A rollercoaster session on Wall Street ended largely flat as oil markets whipsawed on conflicting signals from the US–Iran conflict. After the close, Oracle delivered a convincing earnings beat that sent shares sharply higher, while Kohl's and NIO served up their own dramatic storylines during the regular session.

Oil at Center Stage (again)

If there's one thing that's been dominating market sentiment these past couple of weeks, it's crude oil and Tuesday was no exception.

At one point during the session, WTI dipped below $80/barrel after Energy Secretary Chris Wright posted on social media suggesting a US Navy vessel had successfully navigated the Strait of Hormuz. The post was subsequently removed, and the White House clarified that no tanker had actually passed through the strait, sending oil right back up toward $87/barrel.

Oil prices, which had nearly touched $120 on Monday, had already pulled back sharply after President Trump hinted the conflict with Iran was nearing its end. Saudi Aramco indicated production could be restored within days once the strait fully reopens but Iran's Revolutionary Guard pushed back firmly, signaling that they, not Trump, would determine when hostilities end.

For portfolio managers with energy exposure, that tension is something to watch carefully heading into Wednesday's session.

A sustained reopening of the Strait of Hormuz would be a meaningful headwind for oil prices; any further escalation, however, could send crude back toward triple digits in a hurry. The risk premium in oil remains very much alive.

Broad Market: Flat Finish After a Volatile Ride

The Dow Jones closed 0.1% lower, and the Nasdaq finished essentially flat after a session that briefly showed gains of around 1% before those evaporated by the close. It wasn't a pretty day for the bulls but it wasn't a disaster either. Just the kind of choppy, directionless action you tend to get when traders are simultaneously trying to price in geopolitical risk, mixed earnings, and macro data that doesn't quite fit a clean narrative.

On the macro front, small business optimism continued to erode in February, with NFIB economist Bill Dunkelberg noting that competitive pressure from large companies was squeezing smaller operators, despite solid revenues and profits for many. On the other hand, existing home sales in February came in above expectations, a modest bright spot in an otherwise uncertain environment.

Kohl's: A Profit Beat That Couldn't Buy a Rally

Few stocks put on a more entertaining - and ultimately frustrating - show than department store chain Kohl's KSS | -1.49%. The session started ugly: comparable-store sales declined 2.8% year-over-year, a shortfall roughly twice what analysts had anticipated, while total net sales fell 3.9%. That's not a great report for a retailer already fighting a long battle on relevance.

And yet, for a few glorious hours, the bulls had their moment. Kohl's reported Q4 earnings per share of $1.07, beating the consensus estimate of $0.86 by a healthy margin, and management's candid acknowledgment of the company's shortcomings on the analyst call appeared to resonate.

CEO Michael Bender made it clear that costs are being managed, and that the company knows it has fallen behind on what retailers call "value", a measure of whether shoppers feel they're getting their money's worth. As he put it directly on the call: the company has not consistently brought the right products to market at the right time and in the right place.

The proposed fix is sharper focus, doubling down on fast-growing brands, improving the in-store experience, and helping customers make better style choices. It's a sensible strategy, but I'll be direct: we've heard variations of this turnaround narrative from Kohl's before.

Full-year FY2026 EPS guidance of $1.00–$1.60 came in well below the Street's $1.82 expectation, and the stock ultimately erased its intraday gains to close lower. That tells you everything you need to know about prevailing sentiment on this name.

NIO: A Historic Milestone... and Then Some

If you were looking for good news on Tuesday, NIO NIO | +15.38% delivered it loud and clear. The Chinese electric vehicle maker reported its first-ever quarterly net profit - $40.4 million - along with $178.9 million in adjusted operating profit, which actually exceeded the high end of management's own guidance range. NIO also issued above-consensus guidance for Q1 2026 revenue and deliveries, a sign that momentum is building rather than stalling.

CEO William Bin Li highlighted strong performance across three brands, with the NIO ES8 setting monthly delivery records above the RMB 400,000 price threshold, and the ONVO L90 becoming the top-selling large battery-electric SUV in China for 2025. The company is targeting full-year profitability in 2026, a goal that seemed distant not long ago. The market priced it accordingly with a double-digit surge during the session.

This is a genuine inflection point for NIO, and I think it warrants serious attention — even if near-term volatility is par for the course at these levels. The first-ever profit milestone is a structural catalyst that tends to attract renewed institutional interest in the quarters that follow.

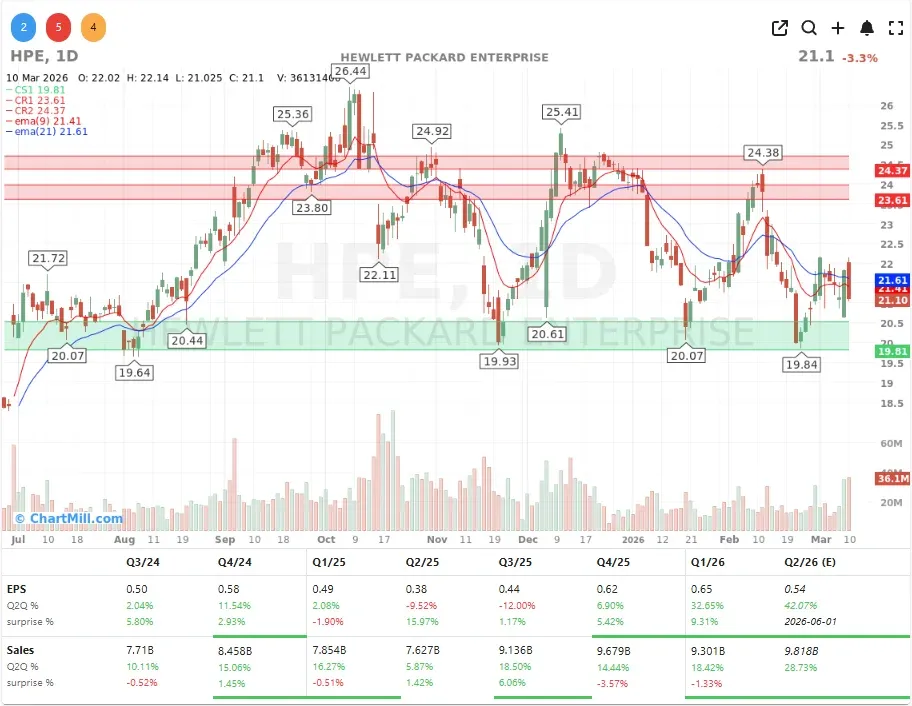

Hewlett Packard Enterprise: Solid Numbers, Cautious Reaction

Hewlett Packard Enterprise HPE | -3.26% reported its Q1 fiscal 2026 results on Monday evening, and on paper the numbers were reasonable. The company posted EPS of $0.65, beating the $0.59 consensus, and raised its full-year FY2026 guidance to $2.30–$2.50 in adjusted EPS. Revenue came in at $9.30 billion - essentially in line with estimates - representing an 18.4% year-over-year increase.

Management pointed to strong demand driven by the AI infrastructure buildout, and the Juniper Networks integration is progressing well. However, the stock still lost ground on Tuesday, reflecting broader skepticism about whether near-term cost pressures - particularly elevated memory pricing - will eat into margins going forward.

HPE noted its intention to pass higher memory costs on to customers, which is a reasonable defensive posture, but the signal to the market remains mixed.

Oracle: The After-Hours Moment Everyone Was Waiting For

This was unquestionably the headline event of the day, and Oracle ORCL | -1.43% (regular session) did not disappoint after the bell (+8.74%).

Q3 fiscal 2026 revenue came in at $17.2 billion - beating the $16.9 billion consensus - while cloud infrastructure revenue surged 84% year-over-year to $4.9 billion, ahead of the 79% growth analysts had modeled and well above the 68% growth from the prior quarter. Earnings per share landed at $1.79 versus the $1.70 consensus.

The company's Remaining Performance Obligations (RPO) - contracted future revenue - climbed to $553 billion, up from $523 billion the prior quarter. That is a number that commands attention. Oracle also issued full-year fiscal 2027 revenue guidance of approximately $90 billion, comfortably ahead of the roughly $87 billion the Street had penciled in.

The critical context: ORCL shares had fallen more than 50% from their September 2025 peak amid investor anxiety over the company's aggressive AI infrastructure spending and rising debt load. Tonight's results - and particularly the RPO expansion - go a long way toward validating the thesis that Oracle's AI buildout is translating into real, contracted demand.

Management also clarified that a meaningful portion of RPO growth is being financed by large AI customers purchasing GPU capacity through Oracle's infrastructure, which materially reduces the self-funding burden. Shares jumped roughly 8% in after-hours trading. For a stock that has been cut in half, that feels like the beginning of a re-rating conversation worth having.

Conclusion

Tuesday was a session defined by noise, geopolitical drama around the Strait of Hormuz, a retail earnings report that couldn't hold its gains, and macro data pointing in two directions at once. But the real story came after the bell, courtesy of Oracle.

For investors who've been watching ORCL languish near multi-year lows, tonight's results offer a meaningful data point: the AI spending cycle is generating real contracted revenue, and the cloud infrastructure business is accelerating. Whether that's enough to sustainably re-rate the stock from here remains to be seen, but it's certainly the most constructive development in the Oracle investment thesis in several months.

Keep NIO's historic profitability milestone on your radar as well; it's the kind of structural shift that tends to attract renewed institutional interest over the coming quarters.

ChartMill Market Desk

This daily update is prepared by ChartMill for informational purposes only and does not constitute investment advice. Always do your own due diligence before making investment decisions.

Next to read: Market Breadth Deteriorates Again as Tuesday’s Rebound Attempt Fades