For investors looking for chances in the market, a methodical method often produces the strongest outcomes. One such method is value investing, a plan created by Benjamin Graham and widely used by Warren Buffett. Fundamentally, value investing means finding companies whose present market price is lower than their calculated true worth. The aim is to buy these underrated securities and keep them until the market adjusts its price, hoping to gain from both price increases and, frequently, dividend payments. To steer clear of the dangers of paying too much or encountering a "value trap", a stock that is low-priced for a cause, investors usually search for companies that are not only low-cost on important measures but also show good basic financial condition, reliable earnings, and sensible expansion potential.

A recent filter for "reasonable value" stocks, which selects for companies with good valuation marks while keeping fair grades in earnings, financial condition, and expansion, has identified NICE Ltd. - Spon ADR (NASDAQ:NICE) as an option deserving more review. This Israeli business software supplier, focusing on customer contact and financial crime compliance products, seems to offer an interesting argument when studied with a value-focused view.

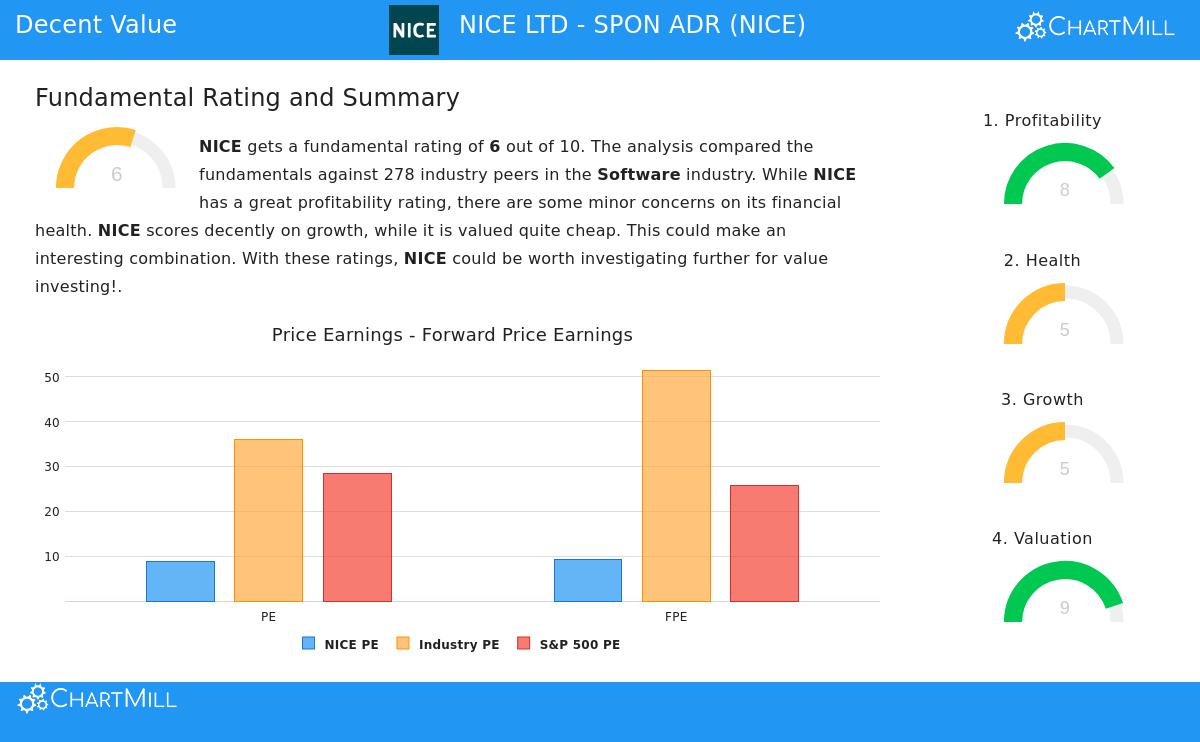

Valuation: A Key Part of Value Investing

The main idea of value investing is locating a notable difference between price and estimated value. NICE’s valuation measures indicate such a difference might be present. According to ChartMill's fundamental analysis report, the company receives a high Valuation Mark of 9 out of 10. This mark comes from several important numbers that are notable, particularly when measured against wider market and sector comparisons.

- Price-to-Earnings (P/E) Ratio: At 8.77, NICE's P/E ratio is much lower than the S&P 500 average of about 28.4. It is also less expensive than almost 90% of similar companies in the software sector.

- Forward P/E Ratio: The valuation stays appealing on a future basis, with a ratio of 9.22, which is also much lower than both the market and sector averages.

- Enterprise Value to EBITDA & Price/Free Cash Flow: The company scores well on these other valuation measures, ranking as less expensive than over 91% of sector rivals.

For a value investor, these measures are the first filter. A low P/E ratio can signal the market is underrating a company's earning ability. However, a low-cost stock is only a sound investment if the basic business is stable—a point key to avoiding value traps. This is where a review of financial condition and earnings becomes essential.

Financial Condition and Earnings: The Base of Security

A company selling at a lower price is of small benefit if it is weighed down by obligations or finding it hard to produce earnings. Value investors look for a "margin of safety," which is strengthened by a good balance sheet and lasting profits. NICE's report displays a varied but mostly good image.

Financial Condition (Mark: 5/10): The company's condition mark is acceptable, backed by one notable aspect: it has no obligations. A balance sheet with no obligations is a major positive, giving great adaptability and removing interest rate danger. This puts its stability ratios with the best in its field. The main issues noted are a small rise in shares available over time and liquidity ratios (Current and Quick Ratio of 1.41) that are only average for sector standards, showing no special benefit or problem in near-term financial handling.

Earnings (Mark: 8/10): This is where NICE does very well. The company shows very good and getting better profit creation, a required quality for a lasting value investment.

- Good Returns: Its Return on Assets (10.83%), Return on Equity (14.45%), and Return on Invested Capital (11.19%) all rank in the top 15-20% of the software sector.

- Strong Margins: Both Operating Margin (22.02%) and Profit Margin (19.37%) are better than most similar companies and have been moving upward.

- Steady Cash Flow: The report confirms positive profits and operating cash flow in each of the last five years.

This high earnings mark is vital. It implies the company's low valuation is not a sign of a failed business plan but could mean a market mistake. A profitable, obligation-free company selling at a single-digit P/E ratio matches well with the traditional value investment outline.

Expansion: The Driver for Future Worth

While strict "deep value" stocks may miss expansion, the "reasonable value" plan looks for companies that are not still. Future expansion is a part of true worth, as described in systems like the Discounted Cash Flow (DCF) study. NICE offers a story of steady, if not fast, expansion.

Expansion (Mark: 5/10): The company's expansion mark is moderate, showing a good past but more controlled future forecasts.

- Past Results: Over the last year and on a multi-year average, both Revenue and Earnings Per Share (EPS) have increased at a double-digit rate (about 9-16%).

- Future View: Experts plan revenue expansion to keep going at a good rate above 8%, though EPS expansion is expected to slow to about 4.8% each year. The report mentions that the expansion rate is slowing from its recent highs.

For a value investor, this outline can be attractive. It shows the company is not shrinking, which supports the idea of an underrating, but its modest forward EPS expansion forecasts may partly clarify the market's quiet valuation—possibly making a chance if the company does better than these forecasts.

Summary and More Study

NICE Ltd. offers a case that meets the needs of a methodical value-seeking plan. It is valued at a major discount to the market and its own sector, has a very good, obligation-free balance sheet, and shows top-level earnings. Its expansion, while slowing, stays positive. This mix of low-cost valuation, good financials, and reasonable expansion tries to give the margin of safety and basic quality that value investors like Graham and Buffett have long supported.

Naturally, no filter replaces complete careful checking. Investors should think about sector rivalry, the lasting nature of NICE's margins, and the specific causes of its expected expansion slowing.

This study of NICE came from a structured search for "reasonable value" stocks. If you want to look at other companies that fit similar needs of fair valuation, earnings, condition, and expansion, you can see the full filter results here.

Notice: This article is for information and learning only. It does not form a suggestion to buy, sell, or keep any security, including NICE Ltd. The study is based on given data and basic reports, which can change. All investment choices include risk, and you should do your own study or talk with a skilled financial guide before making any investment choices.