For investors looking for a disciplined, long-term way to build wealth, few strategies are as respected as Peter Lynch’s method. The famous manager of the Fidelity Magellan Fund supported investing in what you understand, concentrating on companies with clear operations, maintainable growth, and fair prices. His system is not about following the latest fads, but about finding good companies that can be owned for years. It’s a classic growth-at-a-reasonable-price (GARP) strategy, mixing parts of growth and value investing to discover successful investments before Wall Street completely recognizes them.

One company that recently appeared from a filter based on Lynch’s main ideas is Natural Grocers by Vitamin Cottage (NYSE:NGVC). The seller of natural and organic groceries and dietary supplements runs more than 168 stores in 21 states. On initial view, it matches the Lynch model: it is in a simple, clear business, selling healthy food and supplements, that aligns with common consumer patterns. The next phase, as Lynch would suggest, is to examine the figures to see if the basic story holds up the investment idea.

Reviewing the Lynch Standards

The filter uses particular numerical criteria taken from Lynch’s thinking. For a company like Natural Grocers, the given data shows how it compares to these important measures:

- Maintainable Earnings Growth: Lynch preferred companies increasing earnings per share (EPS) between 15% and 30% each year over five years, quick enough to be interesting, but not so fast that it cannot be maintained. Natural Grocers states a five-year EPS growth rate of 17.84%, fittingly inside this goal range. This shows a record of consistent, controlled increase.

- Fair Valuation (PEG Ratio): Maybe the central part of Lynch’s valuation method is the Price/Earnings to Growth (PEG) ratio. A PEG of 1 or less implies the stock price may not entirely account for its growth path. With a PEG ratio (using past 5-year growth) of 0.73, NGVC seems to be valued well compared to its historical earnings growth.

- High Profitability (ROE): Return on Equity (ROE) calculates how well a company produces profits from shareholder equity. Lynch searched for high profitability, frequently setting a demanding standard. NGVC’s ROE of 21.87% is much greater than a common 15% minimum, showing efficient management and a good competitive place in its field.

- Financial Soundness (Debt & Liquidity): A careful balance sheet was crucial for Lynch. He liked companies financed more by equity than debt. NGVC’s Debt-to-Equity ratio of 0.21 is not only much lower than the filter’s maximum of 0.6, it matches Lynch’s stricter liking for ratios below 0.25. The company’s Current Ratio of 1.06 satisfies the basic filter need, showing enough short-term cash availability, though a closer study of its cash cycle would be part of an investor’s additional careful review.

A View of Basic Soundness

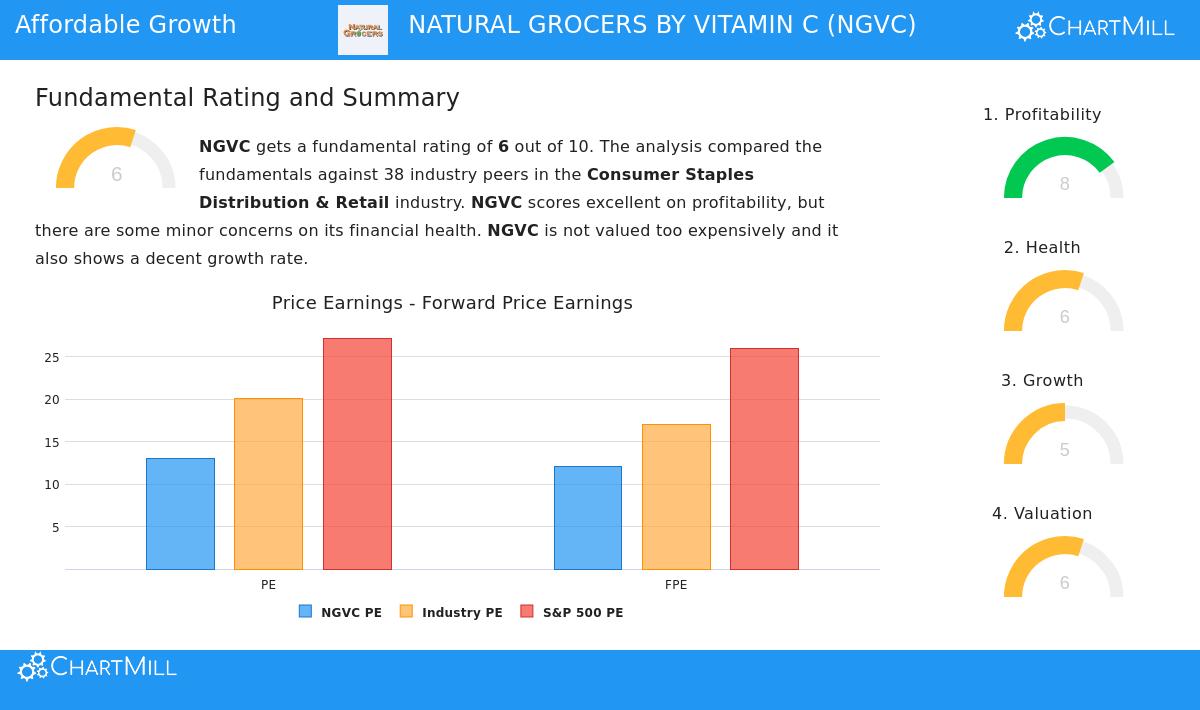

Outside the specific filter criteria, a wider look at Natural Grocers’ basic profile gives setting. Based on a full basic analysis report, the company gets a total rating of 6 out of 10. This score shows a varied but hopeful view:

- Strong Points: The company does very well in profitability, getting an 8 out of 10. Its profit, operating, and gross margins are some of the top in the Consumer Staples Distribution & Retail industry. Its valuation score of 6 suggests the stock is not high-priced, especially when measured against both industry similar companies and the wider S&P 500.

- Points to Note: The financial soundness score of 6 indicates some small issues, mainly linked to short-term cash measures like the Quick Ratio. Still, this is offset by very good solvency signs, including the low debt-to-equity ratio. The growth score of 5 reflects good past EPS growth, though analysts expect a slowing speed in the coming years.

You can see the full basic summary here: NGVC Fundamental Analysis Report.

Why It Matches the GARP Thinking

For the long-term, GARP-centered investor, Natural Grocers offers an interesting example. It works in the steady, essential grocery field, but is placed in the quicker-growing organic and wellness part, a classic "ordinary" industry with a growth element, precisely the kind Lynch valued. The numerical filter supports the story: the company has shown a record of maintainable earnings growth, it is very profitable, it keeps a strong balance sheet with little debt, and the market now values it at a fair price relative to that growth. While it has areas to watch, like the speed of future earnings increase, its profile matches closely with the ideas of searching for quality growth without paying too much.

Locating Other Possible Choices

Filtering is only the initial phase in the Peter Lynch process, used to find a small list for more detailed study. If Natural Grocers by Vitamin Cottage fits your investment thinking, it may be useful to look at other companies that meet similar filters.

You can view the complete Peter Lynch strategy filter and its present outcomes here: Peter Lynch Strategy Stock Screen.

Disclaimer: This article is for information and learning only. It is not meant as investment guidance, a suggestion, or an offer to buy or sell any security. The review of Natural Grocers by Vitamin Cottage Inc. (NGVC) is based on given data and a particular investment strategy filter. Investors should do their own complete research, think about their personal money situation, and talk with a qualified financial advisor before making any investment choices. Past results are not a guide for future results.