In the search for investment opportunities, many market participants turn to the principles of value investing, a strategy created by Benjamin Graham and famously used by Warren Buffett. This method works to find companies trading for less than their intrinsic value, often by using quantitative measures to find stocks that are fundamentally healthy but priced low. A typical technique involves looking for companies that rate well on basic financial health and profitability while also having good valuation measures. This pairing works to find businesses that are not only low-priced, but low-priced without a clear cause, possibly offering a safety buffer for long-term investors.

Neurocrine Biosciences Inc (NASDAQ:NBIX) recently appeared through such a strict screening process. The biopharmaceutical company, focused on neurological and endocrine disorders, shows a profile that fits several important value-investing points. A detailed fundamental analysis report shows a mixed but interesting picture, where healthy basic business measures contrast with what seems to be a fairly low market valuation.

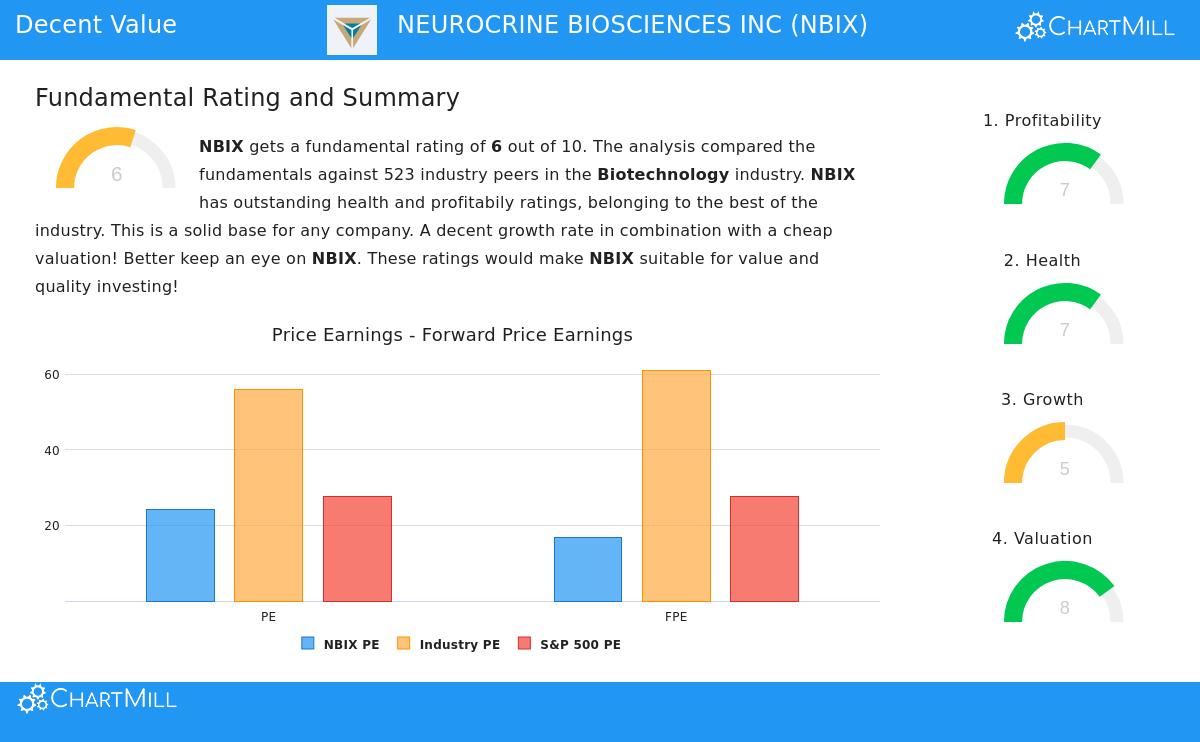

Valuation: A Relative Discount in a High-Cost Sector

For a value investor, the valuation is the beginning. The aim is to pay a price well below a company's estimated worth. Neurocrine's valuation measures indicate it may be trading at such a discount, especially within its own field.

- Price-to-Earnings (P/E): At 24.33, NBIX's P/E ratio is seen as high on an absolute basis. However, context is key. Compared to the biotechnology industry's average P/E of over 55, NBIX costs less than about 94% of similar companies. It also trades similarly to the wider S&P 500 average.

- Forward P/E and Enterprise Value/EBITDA: More revealing are the forward-looking and cash-flow-based measures. With a forward P/E of 16.81, the stock is valued lower than 95% of its industry and sits below the S&P 500 average. Its Enterprise Value to EBITDA ratio also puts it in the lowest 5% of the biotech sector.

- Growth Compensation: The Price/Earnings to Growth (PEG) ratio is low, showing the stock's price may not completely show its expected earnings growth. This is an important measure for value investors who look for growth at a sensible price, as it indicates the market is not paying too much for future potential.

This valuation view is key to the method. A low valuation compared to both the market and, more significantly, to industry peers and future growth, makes the potential for price increase as the market adjusts its view.

Financial Health: A Strong Balance Sheet

A low-cost stock is only a good investment if the company is financially healthy. A solid balance sheet gives the stability to handle economic declines and put money into future growth, lowering the risk of permanent loss of capital—a central idea of value investing. Neurocrine rates well here.

- Debt-Free Operation: The company has no debt, an uncommon and positive trait. This means it has a Debt/Equity ratio of 0, putting it with the best in its sector. The lack of interest payments gives great financial freedom and removes solvency risk.

- Healthy Liquidity: With a Current Ratio of 3.38 and a Quick Ratio of 3.27, Neurocrine has more than enough resources to cover its short-term obligations. This shows a solid ability to fund operations and research projects without financial stress.

- Bankruptcy Risk: An Altman-Z score of 7.42 shows almost no near-term risk of financial trouble, giving investors a notable safety margin on the balance sheet side.

Profitability: Showing Earnings Ability

Value investing is not about buying troubled companies; it is about buying good companies at a discount. Continued profitability is proof of a lasting business model and able management. Neurocrine's profitability measures are a main positive.

- High Margins: The company has notable margins, with a Gross Margin of 98.37% (better than 97% of peers), an Operating Margin of 20.64% (top 5% of the industry), and a Profit Margin of 15.95% (top 8%). These numbers indicate healthy pricing power and efficient operations.

- Very Good Returns on Capital: The Return on Assets (10.03%), Return on Equity (14.25%), and Return on Invested Capital (11.10%) all rank in the top 6-7% of the biotechnology industry. This shows that management is very good at creating profits from the capital it uses.

Growth: The Driver for Future Worth

While pure value stocks sometimes lack growth, the most interesting opportunities often mix value with a growth path. This allows for possible "double gain": price adjustment toward fair value plus increase from business growth. Neurocrine displays solid growth traits.

- Healthy Historical EPS Growth: Earnings Per Share grew by a notable 53.80% over the past year, with a 3-year annualized growth rate of 31.23%. This past performance shows the company's commercial products are becoming more accepted.

- Good Future Expectations: Analysts think this momentum will continue, with EPS predicted to grow about 25% each year in the coming years. Revenue is also projected to grow at nearly 10% per year. This expected growth helps support the current valuation and gives a way for rising intrinsic value over time.

Conclusion and Additional Study

Neurocrine Biosciences presents a case that fits a modern value-investing structure. It is not a deeply troubled asset but a profitable, debt-free, and growing company whose valuation seems low compared to its industry and its own growth outlook. The pairing of a first-class balance sheet, very good profitability, and healthy expected growth, all available at a valuation that screens as inexpensive, makes it a candidate worth more detailed examination for investors using this method.

It is, however, necessary to think about the wider context. The biotechnology sector is naturally risky, affected by clinical trial results, regulatory choices, and competitive forces. Investors must evaluate whether Neurocrine's pipeline supports the growth expectations and if any sector-wide challenges are creating a temporary value pitfall rather than a real opportunity.

For investors interested in using this organized method to find similar possible opportunities, the Decent Value Stocks screen can act as a beginning point for more study.

Disclaimer: This article is for informational purposes only and does not constitute financial advice, a recommendation, or an offer or solicitation to buy or sell any securities. The information presented is based on data believed to be reliable but is not guaranteed. Investing involves risk, including the potential loss of principal. You should conduct your own research and consult with a qualified financial advisor before making any investment decisions.