For investors looking to balance the search for growth with a degree of caution, the Growth at a Reasonable Price (GARP) or "affordable growth" method presents a sensible option. This method tries to find companies that are increasing their sales and profits at a good rate and are also priced at levels that do not require flawless future results. It avoids the speculative excitement common around fast-rising growth stocks and also steers clear of value traps—companies that are inexpensive due to fundamental problems. By filtering for stocks with good growth marks, firm profitability and sound finances, and a fair valuation score, investors can create a collection set to gain from business progress without paying too much.

One stock that recently appeared from this type of filtering process is MICRON TECHNOLOGY INC (NASDAQ:MU). The memory and storage solutions company receives a total fundamental score of 7 out of 10 from ChartMill, a number based on a close review of its financial reports across five main areas. This assessment points to a company that fits the affordable growth idea well, joining firm operational results with a price that seems to consider the ups and downs of its business.

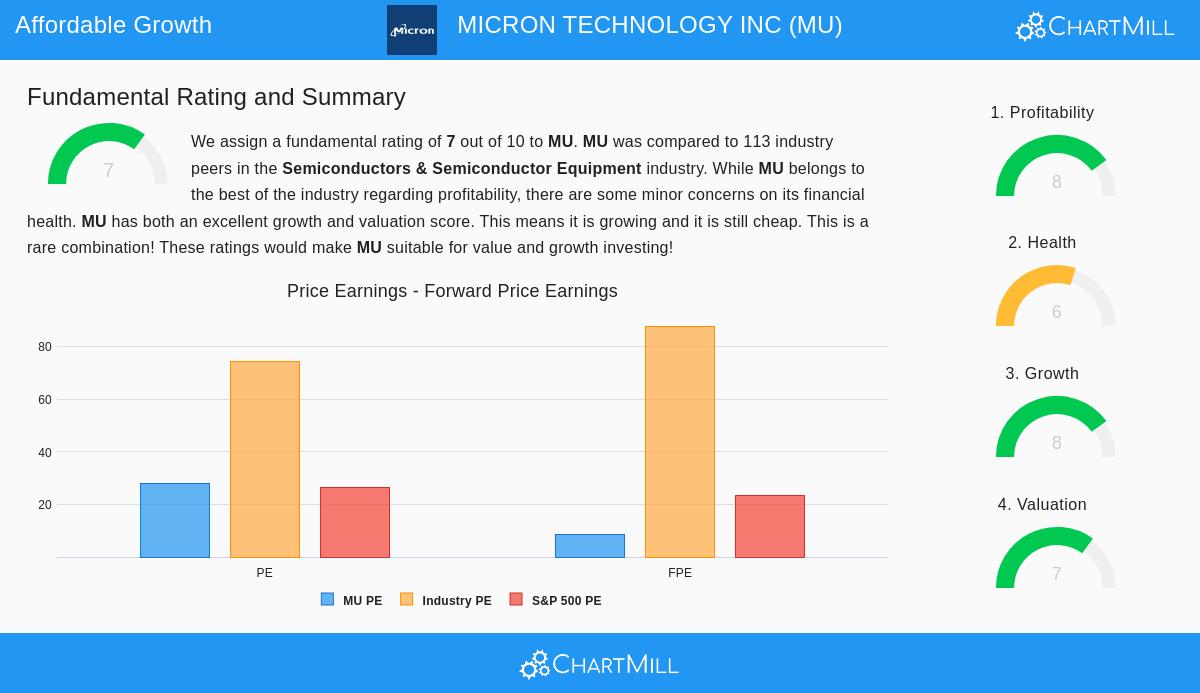

A Close Look at Growth and Valuation

The heart of the affordable growth view for Micron depends on the notable connection between its growth measures and its present price. The company's financial results show a strong growth story, especially in its latest report.

- Strong Recent Growth: In the last year, Micron has posted impressive growth numbers, with Revenue rising by 45.43% and Earnings Per Share (EPS) climbing by 181.30%. This is not an isolated case; the company has shown a good historical pattern with an average yearly EPS growth of almost 24% over recent years.

- Good Future Estimates: For the future, analysts believe this progress will keep going at a steady, though more usual, speed. Revenue is forecast to grow by an average of 12.59% each year, with EPS predicted to rise by 10.58%. This expected growth is key for the GARP method, as it shows the company's expansion can be maintained.

This good growth picture makes the price evaluation even more important. Here, Micron shows a detailed situation that suggests it is fairly priced.

- The P/E Ratio Contrast: Initially, a trailing Price/Earnings (P/E) ratio of 27.96 may appear high. Yet, this needs to be seen with perspective. This number is much lower than over 80% of similar companies in the competitive Semiconductors & Semiconductor Equipment field, where average prices are much higher.

- The Future View is Notable: The more important measure for growth investors is the forward P/E ratio, which uses predicted earnings. Micron's Price/Forward Earnings ratio is 8.70, which is lower than the S&P 500 average and is also lower than each company in its industry. This clear discount to future earnings possibility is a key part of the affordable growth argument.

- Growth Adjustment: The review states that Micron's low PEG ratio—which modifies the P/E ratio for its growth speed—shows a "rather cheap price." This directly relates to the GARP method's aim: obtaining growth without a very high cost.

Supporting Basics: Profitability and Condition

For growth to be "affordable" and lasting, it must rest on a base of operational quality and financial strength. This is where profitability and financial condition scores become important, confirming the company can support its growth and handle slow periods.

Micron's profitability is a clear positive, scoring an 8 out of 10. The company is not only growing; it is turning that growth into high-quality profits.

- Its Return on Equity (20.25%) and Return on Invested Capital (14.22%) are some of the best in the industry, showing efficient use of investor money.

- Strong margins further support this: an Operating Margin of 32.68% and a Profit Margin of 28.15% do better than most industry rivals and have been improving.

The financial condition score of 6 shows a firm, though not perfect, situation. The company keeps a manageable debt level with a low Debt/Equity ratio of 0.19 and a good Altman-Z score, indicating low bankruptcy risk. The report does note some small issues about share dilution over time and liquidity ratios that are only average or a bit below industry norms. However, the overall financial stability remains firm, giving a steady base for continued growth.

Summary and Next Steps

Micron Technology shows the kind of find an affordable growth filter aims to reveal: a company in a strong growth period, supported by high-level profitability and acceptable financial condition, yet priced at a notable discount to both its industry and its own future earnings potential. The cyclical nature of the memory market is probably reflected in this price, offering a buffer for investors who trust the long-term demand from artificial intelligence, data centers, and smart devices.

For investors wanting to review other companies that match this balanced description, more outcomes from the "Affordable Growth" filter can be seen here. A full explanation of Micron's fundamental scores is in its full fundamental analysis report.

Disclaimer: This article is for information only and is not financial advice, a suggestion, or an offer to buy or sell any security. Investors should do their own study and think about their personal money situation before making any investment choices.