For investors looking to balance the search for growth with prudence, the "Growth at a Reasonable Price" or "Affordable Growth" strategy offers a practical middle path. This method tries to find companies that are increasing their earnings and revenue faster than average but are also priced at levels that do not require flawless future results. By filtering for stocks with good growth scores, steady profitability, sound finances, and fair prices, investors can search for chances where a company's prospects may not be completely reflected in its stock price. One stock that recently appeared from this filter is MINISO Group Holding Ltd. (NYSE:MNSO).

A Picture of Growth and Size Increase

MINISO Group Holding Ltd. is a worldwide retailer recognized for its lifestyle and pop toy products under the MINISO and TOP TOY brands. Based in Guangzhou, China, the company runs a large system of stores providing a broad range of items, from home decor and small electronics to toys and cosmetics. Since its initial public offering in late 2020, MINISO has quickly increased its international presence across Asia, the Americas, and Europe. This worldwide retail size increase story forms the central part of its good growth account, which is shown in its fundamental numbers.

Good Growth Numbers

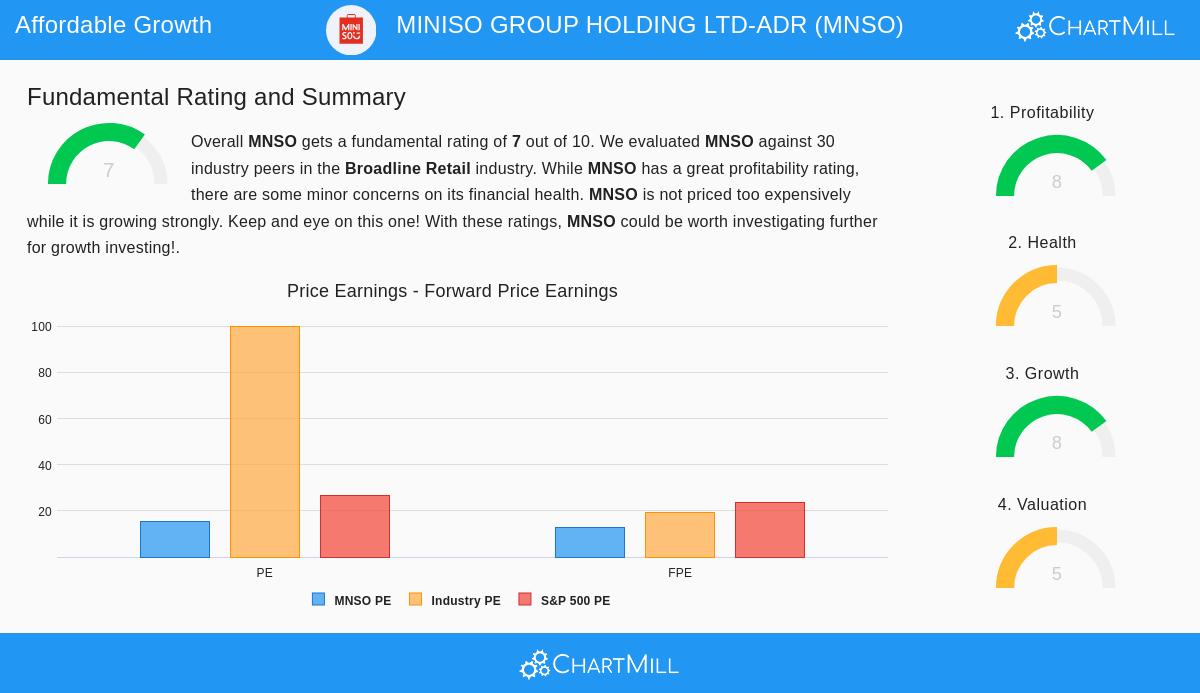

The central idea of an affordable growth strategy is, expectedly, growth. A company must show a clear ability to increase its business and a believable plan to keep doing so. MINISO's fundamental report points out notable strength in this area, giving it a Growth Rating of 8 out of 10.

- Past Results: The company's recent financial reports show solid size increase. Revenue increased by 23.44% over the last year, while Earnings Per Share (EPS) rose by 13.01%. More notably, the average yearly EPS increase over recent years is at a high 73.72%.

- Future Predictions: The growth path is projected to stay good. Analysts forecast an average yearly EPS increase of 14.79% and a revenue increase of 19.77% in the next years. Importantly, the expected revenue increase rate is getting faster compared to its past speed.

- Industry Position: This steady double-digit growth puts MINISO with the better performers in the competitive broadline retail sector, giving a firm base for the investment idea.

Fair Price

A stock with high growth can still be a bad investment if bought at a very high price. The affordable growth strategy clearly tries to prevent this problem by focusing on fair price, and MINISO's Valuation Rating of 5 indicates it is not priced for flawless results.

- Good Ratios: The stock sells at a Price-to-Earnings (P/E) ratio of 15.46 and a forward P/E ratio of 12.98. These numbers are much lower than the current S&P 500 averages (26.55 and 23.78, in that order).

- Sector Comparison: Inside its industry, MINISO seems relatively inexpensive. About 80% of its broadline retail competitors sell at higher P/E and forward P/E ratios.

- Growth Consideration: The price becomes more interesting when seen next to the company's growth and profitability. The report states that its very good profitability could support a higher P/E ratio, and its projected earnings growth aligns with the current price level, hinting investors are not paying too much for future potential. A complete look at these numbers is in the full fundamental analysis report.

Supporting Basics: Profitability and Condition

While growth and price are the main filters, the strategy's need for "acceptable" profitability and financial condition is key for longevity. These parts help confirm the growth is of good quality and the company can manage economic slowdowns.

- High Profitability (Rating: 8): MINISO is strong here. It has leading-in-industry margins, with an Operating Margin of 18.18% and a Profit Margin of 12.63%, doing better than over 93% of its competitors. Its returns on assets (8.83%), equity (21.69%), and invested capital (13.11%) are also high, pointing to very efficient use of money.

- Acceptable Financial Condition (Rating: 5): This is the area with some small points to note, though the total score is seen as suitable for the strategy. The company has a good Altman-Z score (3.39) and solid liquidity ratios, suggesting no immediate bankruptcy danger. However, its Debt-to-Equity ratio (0.72) is above many competitors, and it would take a number of years to clear all debt from its free cash flow. This shows a level of dependence on debt funding that investors should watch.

Summary

MINISO Group presents a profile that fits the affordable growth idea. It shows forceful, speeding revenue growth and good earnings size increase, both in history and in projections. Importantly, this growth is available at a price that is fair compared to both the wider market and its own sector. This pairing meets the main aim of the strategy: locating growth without paying a premium for it. The company's excellent profitability gives trust in the quality of its earnings, while its acceptable, though not top, financial condition score indicates a business that is basically stable but holds a average amount of debt.

For investors curious about examining other companies that fit similar standards of good growth, fair price, and acceptable core basics, more outcomes can be seen by checking the Affordable Growth stock filter.

Disclaimer: This article is for information only and is not financial advice, a suggestion to buy or sell any security, or a support of any investment plan. Investors should do their own study and think about their personal money situation and risk comfort before making any investment choices.