For investors looking for a mix of chance and caution, the "Growth at a Reasonable Price" (GARP) method presents a strong middle path. It tries to find companies showing good and lasting growth, but whose stock prices are not at the high levels common to popular technology shares. This method lessens some dangers linked to pure growth investing by requiring financial stability and fair prices. One method for finding these companies is an "Affordable Growth" stock filter, which looks for firms with good growth measures, firm earnings, stable financial condition, and a price that is not in the high-risk area.

MUELLER INDUSTRIES INC (NYSE:MLI) recently appeared from this kind of filtering. The Tennessee-based maker of copper, brass, aluminum, and plastic goods may not work in the most exciting industry, but its basic financial picture shows a history of very good operational performance and money management.

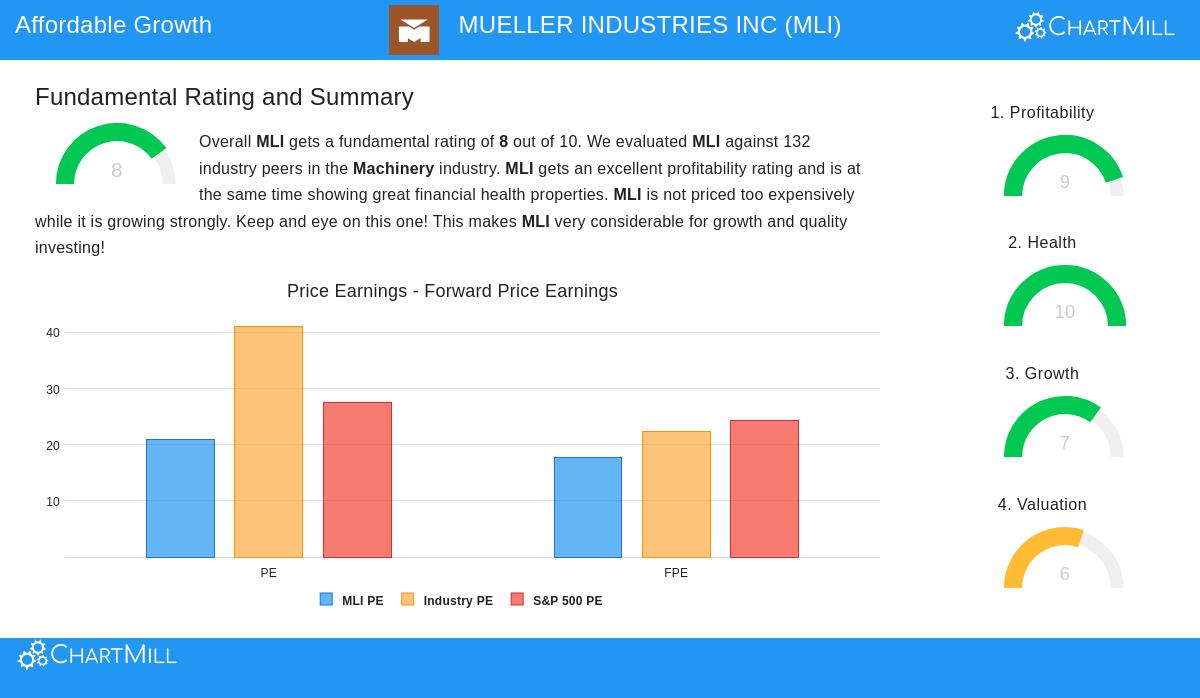

A Base of Very Good Financial Condition and Earnings

Before looking at growth and price, it is important to check the company's base. On these points, Mueller Industries rests on very firm footing. The company's financial condition is excellent, receiving a top mark of 10 out of 10 in the ChartMill basic review. This is supported by a clean record showing no borrowed money and very good cash ratios. Its current ratio of 4.82 and quick ratio of 3.81 are some of the highest in the machinery field, giving great ability to handle economic changes and put money into future expansion.

Adding to this strong record is excellent earnings. Mueller gets a 9 out of 10 here, with profit levels and returns that are better than similar companies.

- Return on Invested Capital (ROIC): At 20.73%, this is a leading result, showing very effective use of money.

- Profit Margin: A margin of 18.10% is much better than most industry rivals.

- Operating Margin: Also good at 21.48%, showing basic operational effectiveness.

This mix of high earnings and no debt is uncommon and forms a key part of the GARP idea, as it shows a low-risk way of operating that can pay for its own growth.

Showing Strong and Continued Growth

The "growth" part of the affordable growth filter is clearly satisfied, with Mueller Industries getting a growth score of 7. The company has produced notable results both lately and over a longer time, moving past regular changes to show a steady rising path.

Past Performance Details:

- Earnings Per Share (EPS) increased by 24.90% in the last year.

- More notably, the average yearly EPS increase over recent years has been a high 42.60%.

- Sales have also grown well, with 15.71% increase last year and a 9.17% average yearly rate.

Future Predictions:

- Experts predict continued firm growth, with EPS expected to rise by 12.67% each year in the next few years.

- Sales are also expected to grow at a steady rate of about 8.13% per year.

While the very high EPS growth rate of the past is predicted to slow, the expected growth stays firm and, importantly, is based on the company's shown operational skill.

Price in View of Quality and Growth

The last part is price, where the filter looks for stocks that are "not overpriced." Mueller Industries scores a 6 here, showing a fair, if not very low, price for its quality. The price view is varied but finally supports the GARP idea when seen as a whole.

- Price-to-Earnings (P/E): At 20.85, MLI's P/E ratio is higher than the market's historical average but is lower than the current S&P 500 average of 27.47. More importantly, it costs less than about 74% of its industry peers, whose average P/E is above 41.

- Price-to-Earnings Growth (PEG): This measure, which includes growth predictions, shows a rather low price. It suggests the market may not be completely counting the company's growth path compared to its earnings multiple.

- Reason for the Multiple: A key point is that high-quality, debt-free companies with excellent earnings and ROIC usually have higher prices. Mueller's P/E ratio, while fair, can be viewed as a suitable price for its very good financial traits and dependable growth.

When judged through the GARP view, Mueller Industries presents a strong case. It is not a high-risk story stock but a basically sound industrial company performing well. Its growth is both shown and expected to keep going, its earnings are top-level, and its record is a source of safety, not danger. The price, while not at the lowest level, seems fair given this full set of quality and growth possibility.

Interested in finding more stocks that match this "Affordable Growth" description? You can use the same filter used to find MLI and find other possible choices here.

For a complete look at all basic measures, you can see the full Fundamental Analysis Report for MLI.

Disclaimer: This article is for information only and is not financial guidance, a suggestion, or an offer to buy or sell any security. The review is based on data and scores from ChartMill, and investors should do their own research and think about their personal money situation and risk comfort before making any investment choices. Past results do not guarantee future outcomes.