For investors looking for companies with good expansion potential that are not trading at very high prices, the "Growth at a Reasonable Price" (GARP) or "Affordable Growth" strategy offers a balanced method. This approach looks for stocks showing good growth paths, firm underlying profitability, and sound financials, all while trading at prices that do not seem too high. The aim is to gain from future earnings growth without paying too much for it now, reducing some of the risk found in pure growth investing. One stock that recently appeared from such a search is Mueller Industries Inc (NYSE:MLI).

A Snapshot of Fundamental Strength

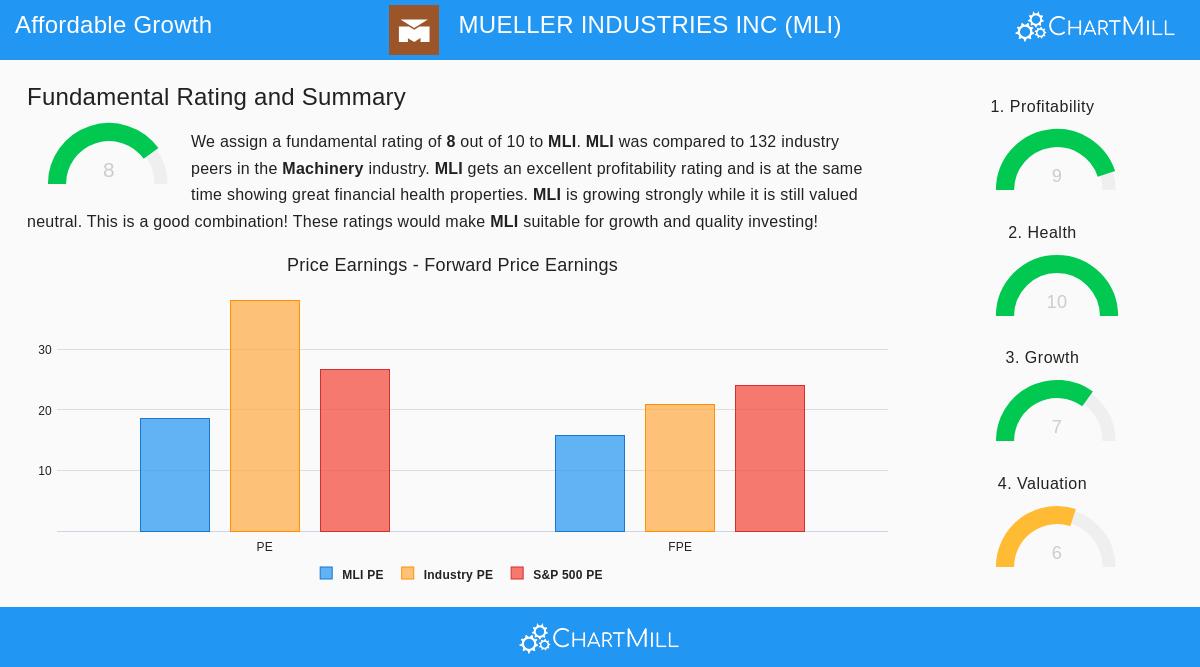

A close fundamental analysis report for Mueller Industries shows an overall score of 8 out of 10, pointing to a firm foundational profile. The company, a maker of copper, brass, aluminum, and plastic products used in plumbing, HVAC, and industrial uses, gets especially high marks in two key areas for cautious growth investors: financial health and profitability. These high scores offer a margin of safety, indicating the company has the operational soundness and balance sheet durability to handle economic changes while supporting its expansion.

Valuation: The "Reasonable Price" Argument

The central idea of an affordable growth strategy is finding companies where the price does not completely account for the growth possibility. Mueller Industries' Valuation Score of 6/10 puts it in a range that is not very low nor very high, providing a sensible entry point.

- Earnings Multiples: The stock trades at a Price-to-Earnings (P/E) ratio of 18.57. While this shows a higher price on a basic level, the situation is important. This P/E is lower than over 76% of similar companies in the Machinery industry and is under the current S&P 500 average.

- Forward-Looking and Cash Flow Measures: Also key, its Price-to-Forward Earnings ratio of 15.79 and its Enterprise Value-to-EBITDA ratio are also better compared to industry averages. The analysis points out that its low PEG ratio, which includes earnings growth, "indicates a rather cheap valuation of the company."

- Justified Premium: The report clearly says that the company's "outstanding profitability rating, which may justify a higher PE ratio." This is a key point for GARP investors: paying a fair price for very good quality and growth is often a reasonable exchange.

Growth: The Engine for Future Returns

A stock cannot be a growth candidate without a good expansion story. Mueller Industries gets a Growth Score of 7/10, backed by strong past performance and positive future estimates.

- Historical Momentum: The company has shown strong earnings expansion, with EPS growing by 24.9% over the last year and at an average yearly rate of 42.6% over recent years. Revenue growth has also been good, at 15.7% for the last year.

- Future Expectations: This movement is expected to continue, though at a more measured, maintainable speed. Analysts forecast future EPS growth of about 12.7% each year, along with revenue growth averaging 8.1%. For a company already of Mueller's size and profitability, this represents a steady growth path.

The Supporting Pillars: Profitability and Financial Health

The affordable growth search needs more than just growth and value; it requires quality. This is where Mueller Industries really performs well, giving the stability that makes the growth story more believable.

- Very Good Profitability (Score: 9/10): The company is very efficient at turning sales into profits. Its Return on Invested Capital (ROIC) of 20.7% and Profit Margin of 18.1% are in the top group of its industry, showing a lasting competitive edge and very good management performance.

- Very Strong Financial Health (Score: 10/10): Maybe the most notable metric is the company's balance sheet strength. Mueller Industries has no debt, has a very high Altman-Z score of 16.5, and has strong liquidity with a Current Ratio of 4.82. This clean financial situation gives great freedom to invest in growth, manage downturns, or return capital to shareholders without the weight of interest costs.

Conclusion

Mueller Industries Inc presents a good case for investors using an Affordable Growth strategy. It joins a clear growth path, shown by strong past performance and positive future estimates, with a price that stays sensible compared to both the market and its high-quality basics. The very good scores in profitability and financial health greatly lower the risk of the investment idea, suggesting the growth is built on a stable and efficient operational base. While the dividend yield is small, the company's perfect balance sheet and high returns on capital are main attractions.

This review of MLI came from a specific search for affordable growth stocks. If you are interested in looking at other companies that fit similar standards of good growth, reasonable price, and sound basics, you can see the full search results here.

Disclaimer: This article is for information only and does not make up financial advice, a suggestion, or an offer to buy or sell any security. The review is based on data and scores from ChartMill.com. Investors should do their own research and think about their personal money situation and risk comfort before making any investment choices. Past results do not show future outcomes.