Investors looking for a disciplined, long-term method for assembling a portfolio frequently consider the ideas of famous fund manager Peter Lynch. His method, outlined in his book One Up on Wall Street, centers on finding expanding companies with sensible prices, highlighting financial strength and lasting earnings. It is a thinking that mixes growth and value investing, often called Growth at a Reasonable Price (GARP). The aim is not to follow the most popular trends but to discover comprehensible companies with sound foundations that can be owned for years. A recent filter using Lynch's main requirements has revealed a well-known name in the technology field: META PLATFORMS INC-CLASS A (NASDAQ:META).

Looking at META Using a Lynch Framework

Peter Lynch’s system uses particular numerical filters to reduce a wide set of stocks to those deserving more study. The filter searches for companies with a past of good, but not extreme, profit expansion, secure financial position, high earnings ability, and a good price when growth is examined. Here is how META Platforms compares against these important Lynch measures.

- Lasting Profit Expansion: Lynch preferred companies with a steady history. The filter needs a 5-year average EPS growth between 15% and 30%, quick enough to be interesting but not so extreme as to be temporary. META’s 5-year EPS growth rate of 24.85% fits well inside this preferred span, showing a solid and regular increase in earnings over a notable time.

- Sensible Price (PEG Ratio): Possibly the main part of the GARP method is the Price/Earnings to Growth (PEG) ratio, which changes the standard P/E ratio for a company’s growth rate. Lynch wanted companies with a PEG ratio of 1 or lower, hinting the market may not be completely valuing the growth path. With a PEG ratio of 0.91, META satisfies this measure, possibly meaning the stock is fairly priced compared to its past profit growth.

- High Earnings Ability (ROE): Return on Equity (ROE) calculates how well a company produces earnings from shareholders' equity. Lynch searched for an ROE above 15% as a mark of a superior business with a lasting edge. META’s ROE of 30.16% greatly passes this standard, putting it in the highest group of its industry for earnings ability.

- Financial Strength (Debt/Equity & Current Ratio): Careful financial management was essential for Lynch. He liked companies financed more by equity than debt, with a Debt/Equity ratio below 0.6 (and preferably below 0.25). META’s ratio of 0.15 shows a very cautious balance sheet with little debt use. Also, a Current Ratio above 1 guarantees a company can pay its near-term bills. META’s ratio of 1.98 signals sufficient cash and financial soundness.

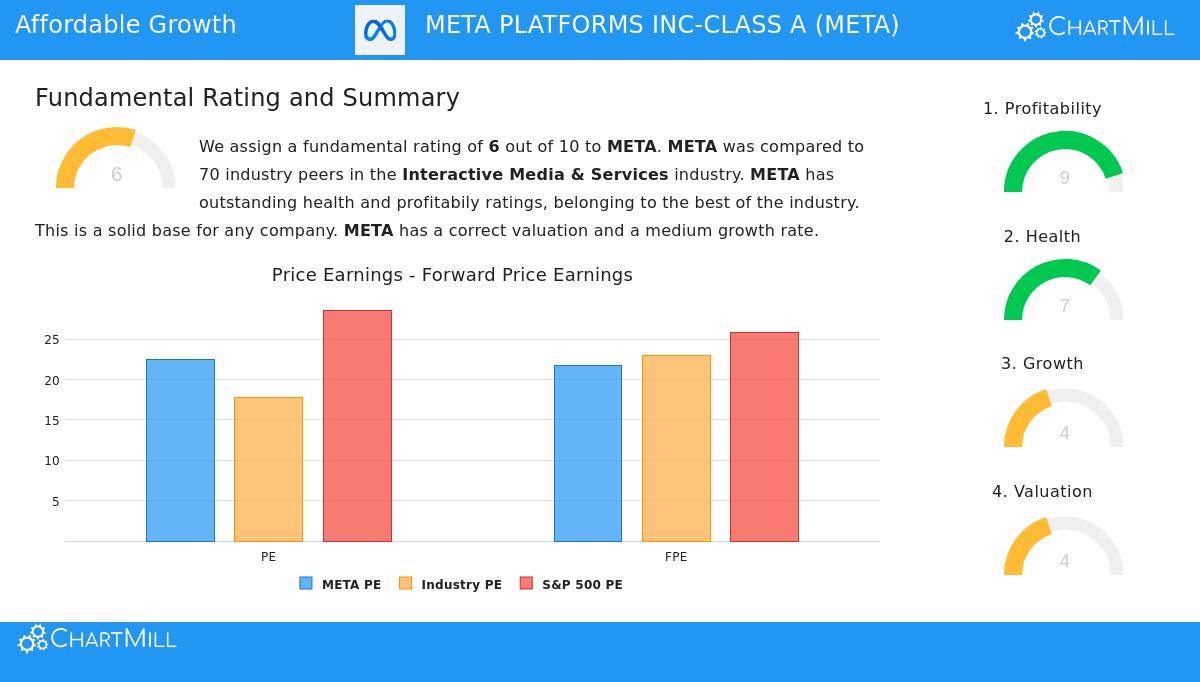

A Broad Fundamental Summary

The full fundamental analysis report for META gives a wider view that backs the Lynch filter findings. The company receives a total fundamental score of 6 out of 10, with specific high points in two areas Lynch stressed.

- Outstanding Earnings Ability: META gets a 9 out of 10 for earnings ability. It has industry-best margins, including an Operating Margin of 43.28% that beats 100% of similar companies, and a Return on Invested Capital (ROIC) of 26.56%. This shows the strong economic machine of its social media and advertising operations.

- Sound Financial Strength: The company scores a 7 for financial strength. Its balance sheet without debt and good solvency numbers, emphasized by a high Altman-Z score of 11.34, highlight its financial durability. This matches well with Lynch’s focus on companies that can survive economic slowdowns.

The report states that while META’s basic P/E ratio may seem high alone, its better earnings ability can support a higher price. The primary points of interest are a small dividend, which is less important for a growth-centered plan, and a price score of 4, which shows a market cost that already includes much of the company’s quality, though the Lynch PEG measure hints growth may still be fairly priced.

Is META a "Know-It" Stock?

Beyond the figures, Lynch suggested investors stay with businesses they grasp. META’s central "Family of Apps", Facebook, Instagram, WhatsApp, and Messenger, are products used by billions worldwide each day. This large, active network is a clear example of the type of leading, common business Lynch thought individual investors could recognize and understand before Wall Street completely values it. While its projects into the metaverse through Reality Labs mean a more uncertain long-term gamble, the company’s main advertising business stays highly profitable and clear.

Finding More Investment Options

The Peter Lynch filter is made to produce a beginning list for more detailed study. META Platforms is one of the companies that presently meets this strict group of filters.

For investors wanting to find other companies that match the Growth at a Reasonable Price description, you can see the full and current outcomes of the Peter Lynch plan filter here.

In short, META Platforms makes a strong argument for investors following the Peter Lynch approach. It displays the qualities he valued: good and lasting historical profit expansion, top-level earnings ability, a very strong balance sheet, and a price that seems sensible when its growth rate is included. As with any investment, this filter-based finding is only the initial stage, requiring complete personal study into the company’s future possibilities, competitive environment, and total place inside a long-term, varied portfolio.

Disclaimer: This article is for information only and does not form financial guidance, a suggestion, or an offer to buy or sell any securities. Investors should do their own study and talk with a qualified financial advisor before making any investment choices.