For investors looking for a mix of chance and caution, the "Growth at a Reasonable Price" (GARP) or "Affordable Growth" method provides a sensible alternative. This method tries to find companies with good and lasting expansion, but whose stock prices are not at extreme levels. It avoids the speculative excitement near popular growth stocks while staying away from value traps, companies that are low-priced for a cause. The process depends on a complete basic review, judging not only expansion and price, but also the core financial condition and earnings that support that expansion. A stock that performs favorably in these areas can be a steadier investment choice.

McKesson Corp (NYSE:MCK) functions centrally in the healthcare supply system. As a top distributor of drugs, medical items, and healthcare technology services, the company holds a vital, though frequently unseen, place in the worldwide medical environment. Its operations include wholesale distribution, prescription technology services, and medical-surgical answers across North America and Europe.

A Look at Good Expansion Path

The central idea of an affordable growth method is, expectedly, expansion. McKesson’s basic report points to this as a definite positive, giving it a Growth Rating of 7 out of 10. The company is not only keeping its place but is also actively enlarging its financial presence.

- Strong Earnings Growth: McKesson has shown notable bottom-line expansion, with Earnings Per Share (EPS) rising by 25.63% over the previous year. More significantly, this is part of a continuing pattern, with an average yearly EPS expansion rate of 17.17% over recent years.

- Steady Revenue Gains: Top-line expansion is similarly firm. Revenue increased by 17.23% in the last year and has been rising at an average yearly rate of 9.22%, showing the company is effectively enlarging its size and market presence.

- Good Future View: This movement is likely to persist. Experts estimate future EPS expansion of about 13.83% each year, backed by expected revenue expansion of 8.52% per year. This steadiness between past results and future forecasts indicates the expansion is based on a firm business base, not a short-term surge.

For a GARP investor, this steady double-digit earnings expansion is a main draw, supplying the "expansion" part of the method.

Price: Sensible Considering the Expansion

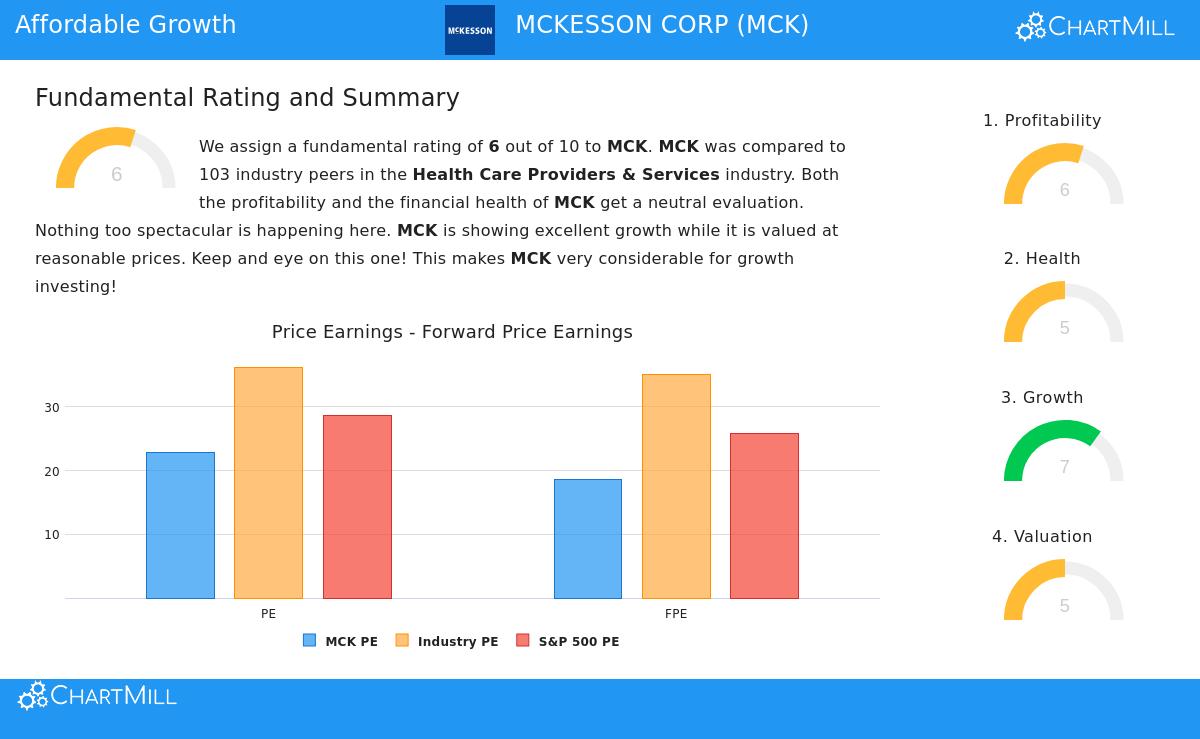

A stock with good expansion can still be a bad investment if the cost is too steep. McKesson’s Valuation Rating of 5 implies it is not in deeply discounted area, but more notably, it is not overly costly relative to its expansion outlook and industry group.

- Varied but Situated Measures: The company’s Price-to-Earnings (P/E) ratio of 22.79 and Forward P/E of 18.68 might seem high initially. However, situation matters. These numbers are lower than the present S&P 500 averages (28.60 and 25.83, in turn). Also, McKesson trades below a large segment of its Health Care Services industry group, where average P/E ratios are much higher.

- Expansion Adjustment: The Price/Earnings-to-Growth (PEG) ratio, which modifies the P/E for anticipated expansion, shows a sensible price. This measure suggests the market is not overvaluing McKesson’s future earnings possibility. The report states that the company’s acceptable earnings and expected expansion rate could support its present price measures.

This equilibrium is key for the affordable growth filter. It removes companies where outstanding expansion is already completely, or overly, accounted for in the stock price, looking for those where the market might not entirely recognize the expansion potential.

Supporting Basics: Condition and Earnings

Lasting expansion cannot stand alone; it needs a profitable business structure and a steady financial setup. McKesson gets average marks here, a Profitability Rating of 6 and a Financial Health Rating of 5, which, within the bounds of this filter, are seen as "acceptable" and adequate for inclusion.

- Earnings Positives and Negatives: The company does very well in returns on capital. Its Return on Invested Capital (ROIC) of 26.27% is outstanding, doing better than almost 98% of its industry group and showing very effective use of capital to produce profits. Yet, this is balanced by very narrow operating and gross margins, which are typical of the low-margin, high-volume distribution business model. The main point is that within its operational structure, McKesson performs with high effectiveness.

- A Financially Sound but Tight Position: McKesson’s financial condition shows a split. First, its ability to pay debts is very good, with a strong Altman-Z score and a very low debt-to-free-cash-flow ratio, indicating little bankruptcy danger and a good ability to handle its debt. Second, its liquidity measures (Current and Quick Ratios under 1) are poor, showing possible issues in meeting immediate bills without incoming cash flow. For a large distributor with predictable cash cycles, this is a recognized concern but often handled through operations.

These "acceptable" marks in condition and earnings are key to the filter's rules. They work as a quality check, making sure the found expansion stocks are not financially weak or unprofitable, thus lowering the chance that the expansion narrative will fail due to balance sheet pressure or poor performance.

Summary

McKesson Corp shows an example of the affordable growth thinking. It displays the necessary element of good, steady earnings expansion backed by increasing revenues. This expansion is offered at a price that, while not low in simple terms, seems sensible next to the wider market and its industry, especially when considering its expansion rate. The company’s outstanding returns on capital show profitable operations, and its firm ability to pay debts gives financial steadiness, even as its cash position needs watching.

For investors filtering for companies that combine expansion possibility with logical price and basic firmness, McKesson justifies more study. Its description matches the aim of finding expansion that the market may not have entirely valued, supported by a business that is financially workable.

You can review McKesson’s complete basic analysis in its detailed analysis report.

To find more stocks that match this "Affordable Growth" description, you can use the same filter with our stock screener tool.