For investors aiming to construct a durable, long-term portfolio, the ideas of quality investing present a useful structure. This method concentrates on finding companies with lasting competitive strengths, sound financial condition, and the capacity to produce steady, high returns on capital. The "Caviar Cruise" stock screen puts this thinking into practice by selecting for firms with good past revenue and profit increases, high returns on invested capital, reasonable debt amounts, and trustworthy earnings. It is a plan created not for fast transactions, but for discovering businesses deserving of long-term holding.

A leading instance found by this strict screen is MASTERCARD INC - A (NYSE:MA). The global payments network operator seems to represent many of the traits quality investors carefully look for.

Meeting the Caviar Cruise Screen

The Caviar Cruise screen uses a number of numerical filters to find high-standard businesses. Mastercard's financial information shows a good match with these central requirements:

- Continued Increase: The screen asks for at least 5% yearly increase in both revenue and EBIT (earnings before interest and taxes) over five years. Mastercard goes beyond this, with a 5-year revenue CAGR of 11.67% and an EBIT CAGR of 11.15%. This steady double-digit increase in its main activities points to a successful business model.

- Profitability Improvement: A central idea of the screen is that EBIT increase should be faster than revenue increase, showing better operational effectiveness and pricing ability. Mastercard satisfies this condition, as its EBIT increase has closely followed its good revenue growth, keeping high profitability.

- Excellent Capital Use: Maybe the most important filter is a Return on Invested Capital (leaving out cash and goodwill) over 15%. Mastercard's number here is very high at 228.49%. This shows the company needs very little extra capital to produce large profits, a sign of an outstanding business with a strong asset-light network.

- Sound Financial Condition: The screen looks at debt sustainability by comparing total debt to free cash flow, favoring a ratio below 5. Mastercard's ratio of 1.16 is very good, meaning it could clear all its debt with just more than one year's free cash flow. This points to little financial danger.

- Trustworthy Earnings: The filter requires that, on average over five years, at least 75% of net income becomes free cash flow. Mastercard's "Profit Quality" score of 101.14% means its accounting profits become cash completely, giving real financial room for dividends, share repurchases, or strategic investments.

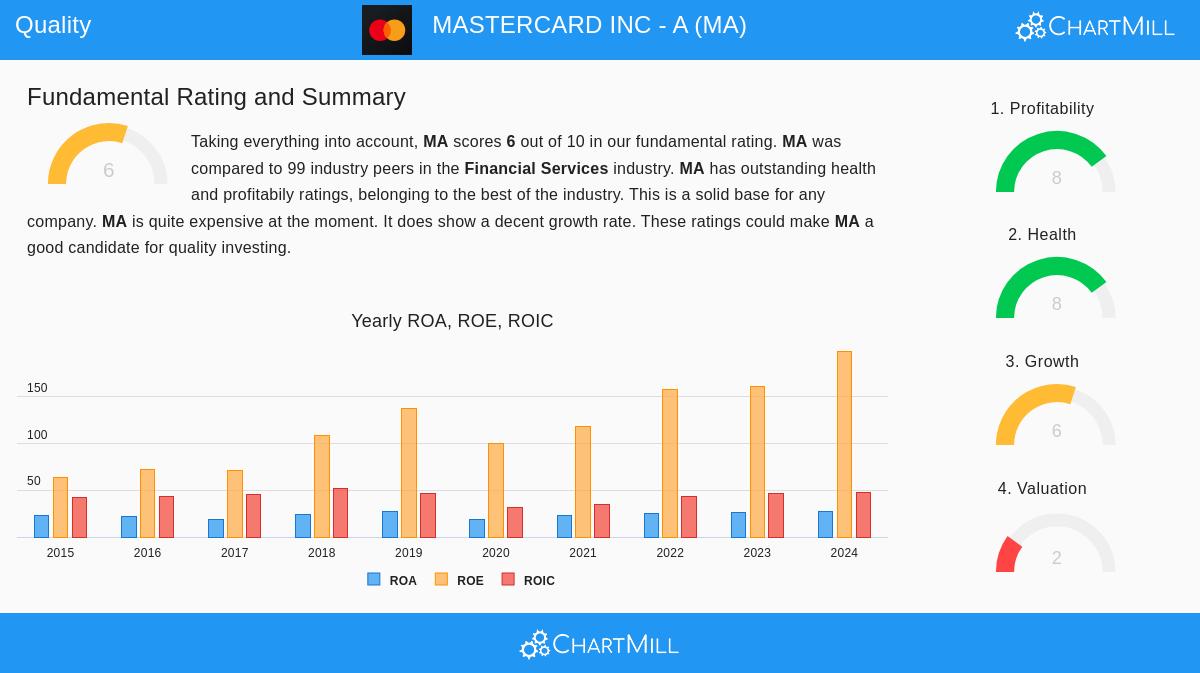

A Top-Level Fundamental Look

A look at Mastercard's detailed fundamental analysis report supports the results from the screen. The company gets a good total rating, with special force in two areas key for quality investors.

Its profitability is very high. Mastercard has industry-best margins, with an operating margin near 60% and a profit margin above 45%. Its returns on assets, equity, and invested capital are all in the highest group of its financial services competitors. This better profitability is the driver of its high ROIC.

The company's financial condition is strong. While its debt-to-equity ratio seems high, this is balanced by its large free cash flow generation, as shown by the excellent Debt/FCF ratio. The report mentions a good Altman-Z score, pointing to very low bankruptcy risk, and finds that the company's solvency and profitability lessen worries from more common liquidity ratios.

The main warning in the report focuses on price. Mastercard sells at a high level, with a P/E ratio above both its industry and the wider market. The report indicates this high price may be reasonable given the company's very good profitability and expected earnings increase, but it notes that a quality investor must still think about cost when making an ownership choice.

The Non-Quantitative Argument for Quality

Beyond the figures, Mastercard’s business model fits with the less measurable parts of quality investing. It runs a classic "toll-road" business inside the global electronic payments system, gaining from the long-term, structural shift away from cash. Its competitive strength, or moat, is broad, built on a huge, two-sided network of merchants and financial institutions that is very hard to copy. The business is fairly simple to grasp, has global size, and shows pricing ability, all features that quality investors value for a buy-and-keep holding.

Finding Other Quality Possibilities

Mastercard shows the kind of company the Caviar Cruise screen is made to find. Investors curious about using this method to locate other possible choices can run the screen themselves here.

Disclaimer: This article is for information only and does not make up financial advice, a suggestion, or an offer to buy or sell any security. Investors should do their own study and think about their personal financial situation before making any investment choices.