The investment philosophy of Peter Lynch, famous manager of the Fidelity Magellan Fund, focuses on finding good companies with lasting growth that are available at fair prices. His method, often called Growth at a Reasonable Price (GARP), stays away from speculative manias by concentrating on firms with solid foundations, low debt, and high profitability. A main idea is putting money into businesses that are easy to grasp, frequently those seen in daily life, before they gain widespread attention on Wall Street. By using a methodical filter built on Lynch's rules, investors can create a list of possible choices for more detailed study. One firm that recently met this filter is Lululemon Athletica Inc (NASDAQ:LULU).

Meeting the Lynch Criteria

Lululemon's profile matches many of Peter Lynch's numerical filters, which are made to locate sound, expanding companies without extreme prices.

- Lasting Earnings Growth: Lynch preferred companies with steady, high growth, which is easier to keep up. Lululemon's earnings per share (EPS) have increased at an average yearly rate of 24.37% over the last five years. This easily passes the filter's lowest limit of 15% while staying under the 30% maximum Lynch used to steer clear of growth paths that cannot last.

- Fair Valuation via PEG Ratio: Maybe the most important Lynch measure is the Price/Earnings to Growth (PEG) ratio, which tries to price a company next to its growth rate. A PEG ratio at or under 1.0 is seen as good. Lululemon's PEG ratio, using its past five-year growth, is about 0.60, suggesting the market might be pricing its growth story too low compared to its earnings.

- Outstanding Financial Health: Lynch required companies with firm balance sheets.

- Debt/Equity Ratio: Lululemon shows a Debt/Equity ratio of 0.0, meaning it has no debt that charges interest. This is much better than Lynch's chosen standard of under 0.6 (and his more exacting choice for under 0.25), putting the company in a very safe financial state.

- Current Ratio: The company's Current Ratio of 2.13 indicates it has more than sufficient near-term assets to pay its near-term obligations, easily meeting the filter's need to be at least 1.

- High Profitability: A minimum Return on Equity (ROE) of 15% was a Lynch standard for good use of shareholder money. Lululemon's ROE of 38.67% is exceptional, meaning the company is very good at creating profits from its equity.

Fundamental Strength in Detail

A wider fundamental review of Lululemon supports the image shown by the Lynch filter. The company gets a high total fundamental score, led by top marks in health and profitability.

The company's profitability measures are strong in all areas. It keeps high margins, with a Gross Margin around 58% and a Profit Margin above 15%, both placing in the best of its industry. The high returns on assets, invested capital, and equity further prove efficient management and a strong brand position.

Financially, Lululemon is in excellent health. The lack of debt removes default risk and gives major room to maneuver. Its Altman-Z score points to a minimal chance of failure, and the consistent decrease in shares outstanding in recent years matches another Lynch liking for companies that repurchase stock, increasing value per share.

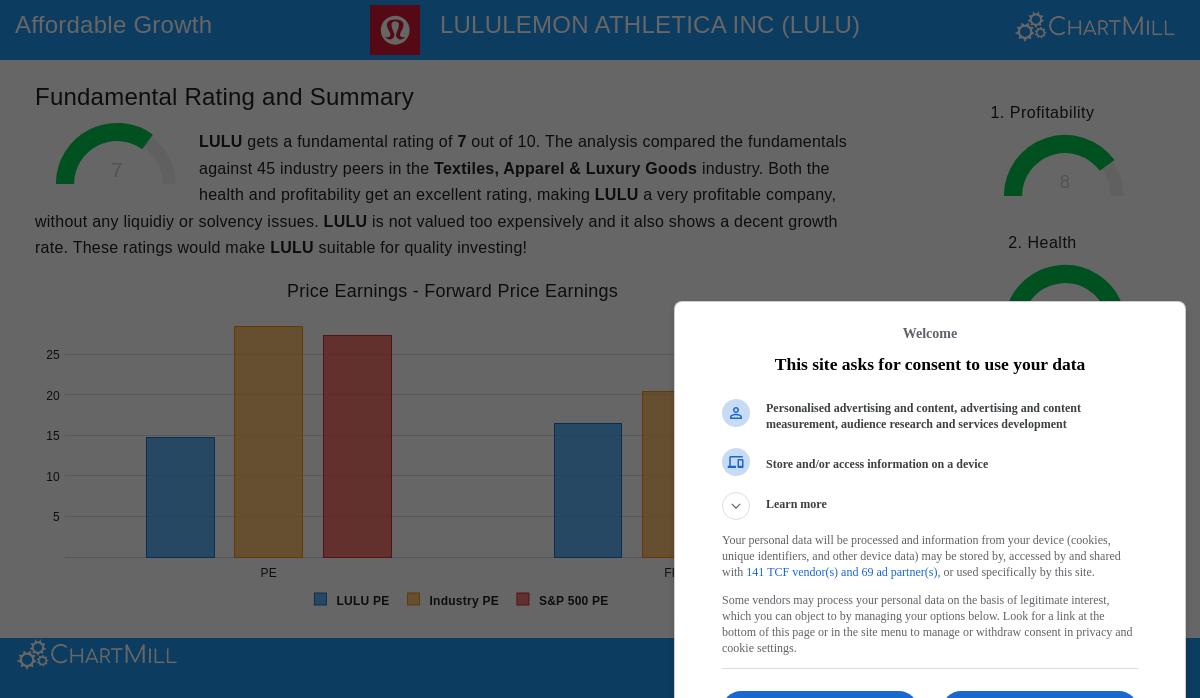

On price, Lululemon seems fairly valued next to both its own past and the wider market. Its P/E ratio is lower than the present S&P 500 average, and many of its price multiples are less expensive than those of its industry competitors in the textiles, apparel, and luxury goods sector. This mix of fair price with high growth and profitability is the heart of the GARP method.

You can see the full fundamental review for Lululemon Athletica Inc here.

The Lynch Philosophy in Practice

Lululemon acts as a real-world case of Lynch's rule of "investing in what you know." The brand has expanded from a yoga company to a leading worldwide name in technical athletic wear, a product group millions of customers use themselves. This exposure lets investors learn the business plan and judge brand quality directly before checking the numbers. The company’s attention on a particular, growing area, premium athletic leisurewear, fits Lynch's liking for understandable companies working in fields with lasting need.

Considerations for Investors

While the Lynch filter points out notable strengths, it is a first step for study, not a direct instruction to buy. Investors should see that analysts expect Lululemon's future sales and earnings growth to slow from its impressive past speed. This is a normal change for an established company but needs careful look to decide if the present price correctly accounts for this reduced growth path. Also, the company does not offer a dividend, which could be a factor for portfolios seeking income.

Exploring Further Opportunities

Lululemon Athletica Inc stands for one present choice found through the Peter Lynch investment model. For investors wanting to find other companies that meet these rules for lasting growth at fair prices, the complete Peter Lynch strategy filter is ready to review here.

Disclaimer: This article is for information only and is not financial guidance, a suggestion, or an offer to buy or sell any security. The review uses data and a particular investment strategy model; each investor should do their own complete research and think about their personal money situation and risk comfort before making any investment choices.