For investors looking for chances where the market price may not completely show a company's true value, a disciplined screening method can be a helpful first step. One such technique looks for equities that join an attractive valuation with good basic business condition. This strategy selects for stocks with high valuation ratings, meaning they are priced low compared to important financial measures, while also needing acceptable scores in profitability, financial condition, and growth. The aim is to find companies that are not just low-priced on paper, but are fundamentally good businesses selling for less than they might be worth, possibly providing a buffer for investors focused on value.

A recent filter using this approach has pointed to Kinross Gold Corp (NYSE:KGC) as a candidate for more detailed review. As a large gold mining company with a worldwide collection of mines and development projects, Kinross works in a field often affected by commodity price swings and market feeling. The filter outcomes indicate its present share price may not completely represent its operational and financial qualities.

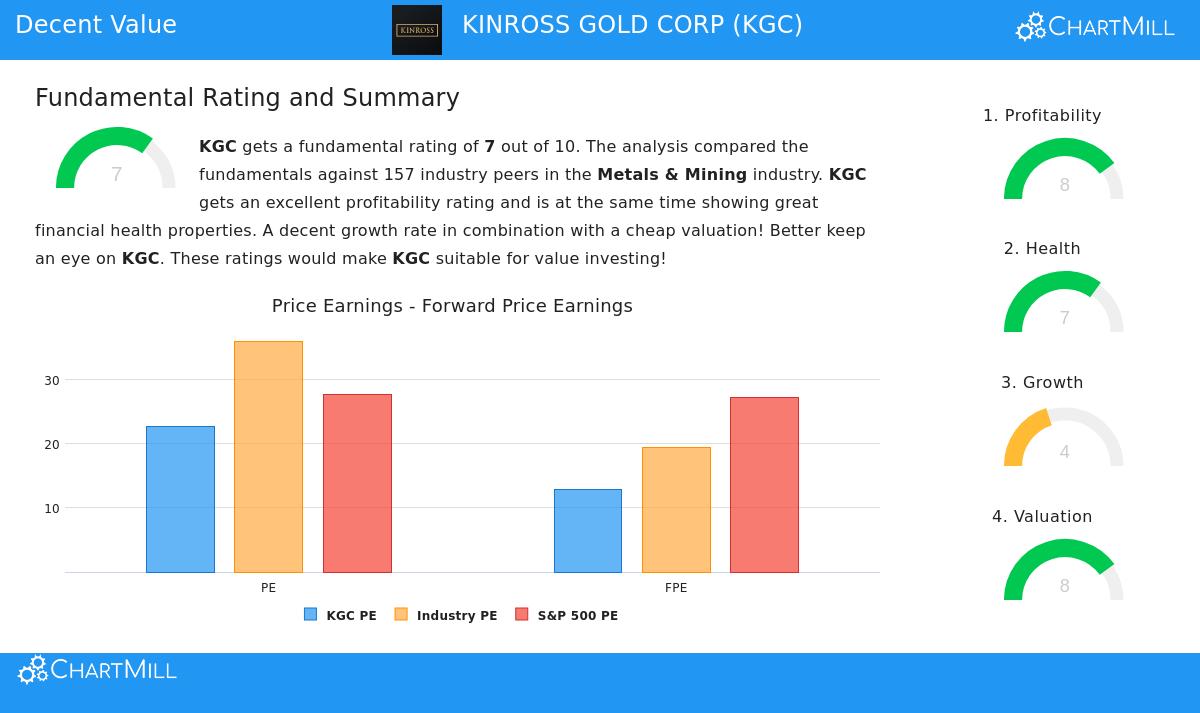

Valuation: An Attractive Entry Point

The central idea of value investing is buying an asset for less than its calculated worth. Kinross’s basic report gives it a high Valuation score of 8 out of 10, showing it seems low-priced compared to its industry and its own financial results.

- Good Multiples: While its standard P/E ratio of 22.64 matches the wider S&P 500, it is clearly lower-priced than 83% of similar companies in the Metals & Mining industry. More future-oriented measures are even more interesting. Its Price/Forward Earnings ratio of 12.83 is lower than 77% of industry rivals and rests under the S&P 500 average.

- Cash Flow and EBITDA: The company’s valuation seems especially interesting when looking at cash creation. Kinross sells at a Price/Free Cash Flow ratio that is lower than 92% of its industry, and its Enterprise Value to EBITDA multiple is lower than 76% of peers. These measures are important as they are less affected by accounting changes than earnings.

- Growth Adjustment: A low PEG ratio, which changes the P/E for predicted earnings growth, adds more support for a stock that may be priced too low. The report states that Kinross’s “high profitability score may support a higher PE ratio,” and that quicker predicted earnings growth can also support a higher valuation, neither of which seems completely included in the price now.

For a value investor, this mix of low multiples relative to the industry and good cash-based valuations implies the market may be using a reduced price, possibly giving a chance if the company’s basic condition stays strong.

Financial Health: A Good Base

A low-priced stock is only a worthwhile investment if the company is financially secure. Poor investments often come from businesses with weak finances. Kinross gets a 7 for Financial Health, showing a company with acceptable debt and good cash availability.

- Good Solvency: The company’s Altman-Z score of 6.27 shows a very small short-term chance of financial trouble, doing better than 69% of the industry. Its debt amounts are careful, with a very good Debt to Free Cash Flow ratio of 0.62, meaning it could pay off all its debt with under a year’s FCF.

- Acceptable Leverage and Liquidity: A Debt/Equity ratio of 0.16 shows little dependence on debt funding. Also, a Current Ratio of 2.84 means more than enough short-term assets to cover near-term debts, giving operational room and strength.

This good financial condition lowers risk for investors and gives the company the steadiness to handle commodity price changes and put money into its future projects without taking on too much debt.

Profitability: Creating Strong Returns

A high valuation score loses its attraction if the business does not make money. Kinross does very well here, getting a Profitability score of 8. The company is not only profitable; it is very effective compared to its industry.

- Better Returns: The company creates a Return on Equity (ROE) of 20.25% and a Return on Invested Capital (ROIC) of 13.90%, doing better than about 93% and 89% of its industry peers, in that order. This shows management is using capital well to create returns for shareholders.

- High Margins: Kinross keeps notable margins, with a Profit Margin of 25.19% and an Operating Margin of 38.20%, both placed in the top ten percent of its industry. Its Gross Margin has also been getting better in recent years.

For the value plan, this high profitability is key. It gives proof that the company’s low valuation is not a sign of bad operations, but instead a possible market error in pricing a good, cash-creating business.

Growth: A Varied but Clear View

The filter needed acceptable growth, and Kinross’s report shows a detailed view with a Growth score of 4. The score reflects very good recent results against more careful short-term predictions, which is normal in changing industries like mining.

- Very Good Past Growth: Over the last year, Kinross provided very high growth with EPS up 133.9% and Revenue rising 32.9%. Its long-term history is also good, with EPS growing at a yearly rate of nearly 15% over recent years.

- Slowing Future Predictions: Analyst forecasts show a drop in both EPS and Revenue over the next few years. This expected return to a normal level is a main reason likely adding to the stock’s low valuation.

From a value view, this setting is important. The filter finds companies with acceptable growth, not always high-growth stocks. Kinross’s good past performance shows ability, while the predicted slowdown helps explain the valuation chance. The investor’s job is to decide if the market has adjusted too much for this expected change.

Conclusion and Next Steps

Kinross Gold Corp shows a picture that fits the ideas of looking for low-priced stocks with good basics. Its high Valuation score suggests it is priced carefully, especially compared to its high profitability and financial condition. While future growth predictions are lower, its very good recent results and top-level margins point to a well-managed company in a changing field.

This review comes from a methodical search for such chances. Investors wanting to see other companies that meet similar filters for good valuation along with acceptable profitability, condition, and growth can look at the Decent Value Stocks screen on ChartMill.

Disclaimer: This article is for information only and is not financial advice, a suggestion, or an offer to buy or sell any security. The review is based on data and scores from ChartMill, and investors should do their own complete research, including looking at Kinross Gold Corp’s full fundamental analysis report, newest SEC filings, and thinking about their personal risk comfort and investment plans before making any investment choice. Past results do not show future outcomes.