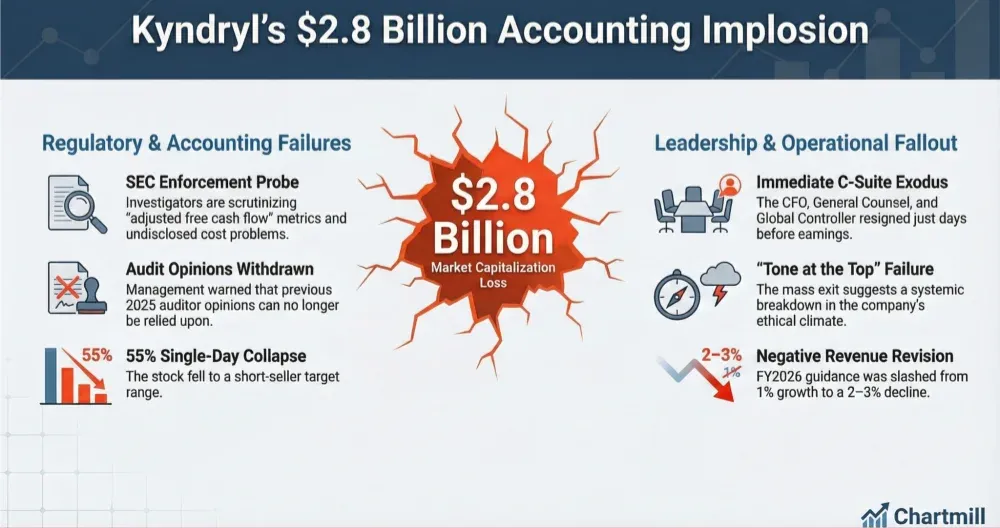

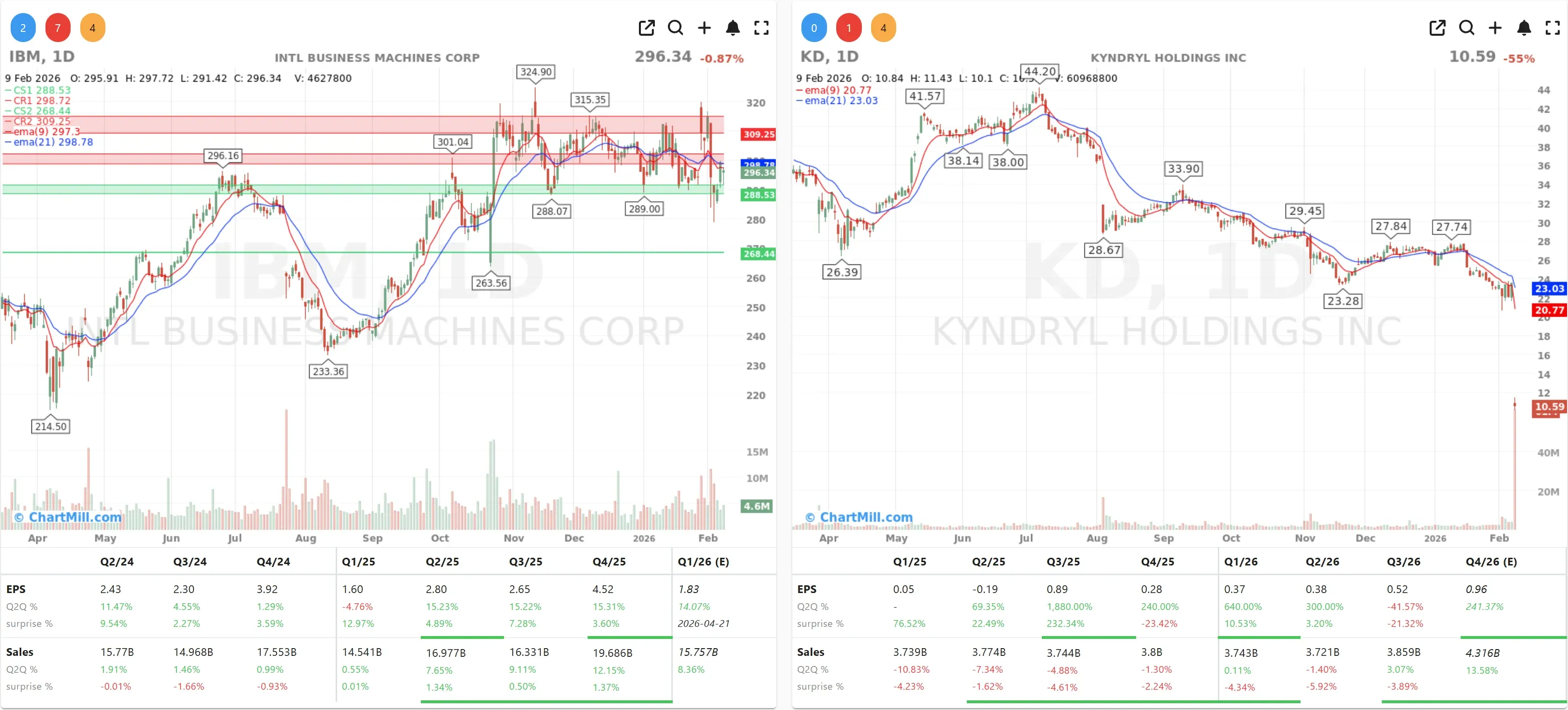

I’ve rarely seen a "told you so" moment as devastating as the one that just hit Kyndryl (KD | -54.92%).

For nearly a year, the company dismissed short-seller allegations as mere "falsehoods," but today those chickens came home to roost with a $2.8 billion loss in market cap.

The Gotham Ghost and the SEC Hammer

The catalyst for this carnage was the disclosure that the SEC’s Division of Enforcement has issued voluntary document requests focused on Kyndryl’s cash management practices. Specifically, investigators are digging into the drivers of the company’s "adjusted free cash flow" metric.

This move directly vindicates the March 2025 report from Gotham City Research, which accused the company of manipulating these very figures to project a false image of profitability. I find it particularly damning that the SEC is now looking at the exact "undisclosed cost problem" that Kyndryl (KD | -54.92%) so aggressively denied just months ago.

A C-Suite in Full Retreat

The scale of the executive departure is, frankly, alarming.

CFO David Wyshner and General Counsel Edward Sebold departed "effective immediately" a mere four days before the scheduled earnings call. When you add the departure of the Global Controller and the company’s warning that previous auditor opinions from 2025 can "no longer be relied upon," you are looking at a fundamental breakdown of what auditors call "tone at the top", the ethical climate set by management.

To make matters worse for the long-term outlook, Kyndryl slashed its revenue guidance for fiscal year 2026. What was once expected to be a modest 1% growth has been revised to a 2–3% decline. For many investors who received these shares during the IBM spin-off in 2021, the "operational progress" management touted just last quarter now looks like a house of cards.

The Legal and Financial Fallout

The blood in the water has already attracted the sharks.

Multiple law firms, including Johnson Fistel, have launched investigations into potential violations of federal securities laws. Investors are left grappling with systemic problems that the company admits will likely impact financial reporting through most of 2026.

Conclusion

In my opinion, the disclosure of "material weaknesses" regarding corporate governance and the SEC's interest in cash flow manipulation suggests that a restatement of past earnings may be a "when," not an "if." Until a permanent CFO is found and the SEC probe concludes, this stock is a toxic asset for any portfolio. The IBM legacy has never felt heavier.

Kristoff - ChartMill