For investors looking to balance the search for growth with a degree of caution, the "Growth at a Reasonable Price" (GARP) method presents a thoughtful middle path. This method tries to find companies that are increasing their earnings and revenue at a good pace while also trading at prices that do not require flawless future results. It is a way to steer clear of the speculation of high-growth stocks and the potential stagnation of very low-priced stocks. One method for finding these opportunities is the "Affordable Growth" stock screen, which looks for companies with good growth scores, firm profitability and financial soundness, and a valuation that is not extreme. A recent name from this screen is manufacturing solutions provider Jabil Inc (NYSE:JBL).

Examining Growth and Valuation

The center of the GARP case for Jabil depends on its mix of good growth measures and a sensible price. According to ChartMill's fundamental analysis, Jabil receives a Growth Rating of 7 out of 10 and a Valuation Rating of 7 out of 10. This combination is important; it shows the company is achieving firm expansion without being valued for extreme, unlikely future success.

- Good Historical and Expected Growth: The company's Earnings Per Share (EPS) increased by a notable 35.07% over the last year, with a five-year annual growth rate of 27.52%. For the future, analysts believe this pace will persist, with EPS predicted to grow at an average yearly rate of 17.64%. Revenue growth is also positive, with an 8.65% yearly rise anticipated in the next years.

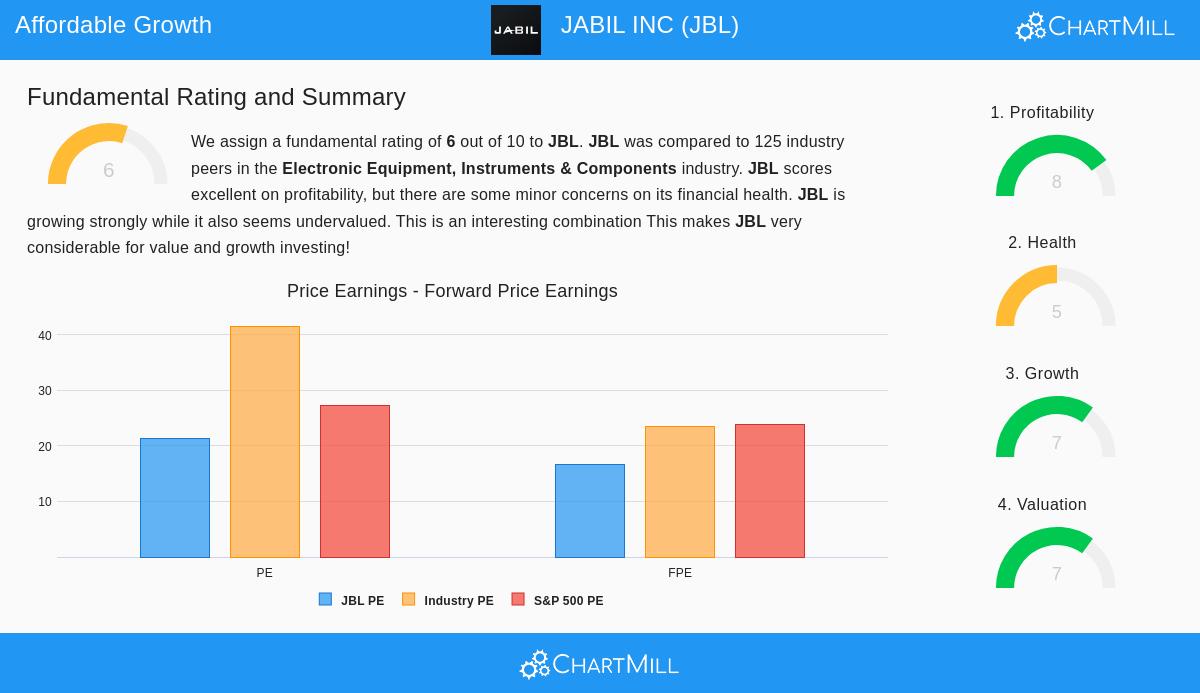

- Sensible Valuation Multiples: Even with this growth picture, Jabil's stock seems fairly priced. Its Price-to-Earnings (P/E) ratio of 21.27 is lower than 77.6% of similar companies in the Electronic Equipment, Instruments & Components industry and is under the current S&P 500 average. More forward-looking measures are even more interesting: its Price-to-Forward Earnings ratio of 16.68 is lower than 81.6% of industry peers. The company also performs well on enterprise value and free cash flow multiples, supporting the idea that investors are not paying too much for its growth path.

You can see the complete details of these scores in the detailed fundamental analysis report for JBL.

Supporting Fundamentals: Profitability and Financial Soundness

For a GARP investment to last, good growth at a sensible price must be supported by a stable base. This is where profitability and financial soundness are key, confirming the company can finance its expansion and handle economic shifts. Jabil's scores in these areas give important support for the investment case.

- High Scores for Profitability: Jabil gets a firm Profitability Rating of 8 out of 10. The company has been reliably profitable with positive cash flow over the past five years. More significantly, it produces very good returns on capital. Its Return on Invested Capital (ROIC) of 24.71% and Return on Equity (ROE) of 52.31% are some of the top in its industry, showing very efficient use of shareholder capital. While its gross margins are somewhat narrow, a trait of the manufacturing sector, they have been getting better, and its operating margin of 4.91% is above the industry median.

- A Varied but Acceptable Soundness Picture: The company's Financial Health Rating of 5 out of 10 shows a more detailed picture, pointing out an area for investor review. On the good side, Jabil generates substantial value, as its ROIC is well above its cost of capital. It has also been lowering its share count and holds an acceptable amount of debt compared to its free cash flow. The main focus is on liquidity: its Current and Quick ratios are below 1.0, which indicates possible difficulty in meeting near-term debts without using operating cash flow or new financing. This is typical in asset-light, working capital-intensive operations but needs attention.

Conclusion: A Name for the Affordable Growth Investor

Jabil Inc shows a profile that matches well with the aims of an affordable growth method. The company displays a strong source of growth, in both its recent results and its forecasted future earnings, supported by its role in fields like AI infrastructure, healthcare, and automotive. Importantly, this growth is offered at a valuation that seems moderate compared to both its industry and the wider market. This mix meets the main GARP aim of not overpaying for growth.

The firm profitability, shown by exceptional returns on capital, suggests this growth is high-quality and efficient. The financial soundness measures, while indicating some liquidity pressure, are offset by firm cash generation and an acceptable overall debt situation. For investors searching for companies that offer an interesting growth narrative without a speculative price, Jabil deserves further examination.

This review of Jabil was prompted by an "Affordable Growth" screen. If you want to find other stocks that fit similar standards of good growth, sensible valuation, and acceptable fundamentals, you can use this screen yourself with the ChartMill stock screener.

Disclaimer: This article is for informational purposes only and does not constitute financial advice, an endorsement, or a recommendation to buy, sell, or hold any security. The information presented is based on data provided and should not be the sole basis for an investment decision. Investors should conduct their own thorough research and consider their individual financial circumstances and risk tolerance before making any investment.