For investors looking to balance the search for growth with a degree of caution, the "Growth at a Reasonable Price" (GARP) or "affordable growth" strategy offers a practical middle path. This method tries to find companies that are showing good and lasting expansion, but whose stock prices are not at extreme levels. It tries to sidestep the high chance of paying too much for future prospects while still gaining from the progress of expanding businesses. A useful method to apply this strategy is by using fundamental stock screeners that grade companies on important areas such as growth, valuation, profitability, and financial condition. Stocks that grade well in these areas, especially with good growth combined with a fair valuation, can offer interesting possibilities for more study.

Jabil Inc (NYSE:JBL), a worldwide manufacturing services company, recently appeared from such an "Affordable Growth" screen. The screen looks for stocks with a high growth grade (above 7 out of 10), along with acceptable grades in profitability, financial condition, and a valuation that is not seen as high (grade above 5). Jabil's fundamental picture suggests it deserves more examination from investors using this method.

Strong Growth Path

The central idea of the affordable growth strategy is, expectedly, growth. Jabil's fundamentals show a company in a good expansion period, receiving a Growth Grade of 7. The company's recent results and future view give firm proof.

- Notable Earnings Growth: Over the last year, Jabil's Earnings Per Share (EPS) increased by a notable 35.07%. This is not an isolated event, as the company has shown a good average yearly EPS growth of 27.52% over recent years.

- Firm Revenue Growth: Revenue grew by 13.18% in the past year, a good number for a company of its size. While the multi-year average is more moderate, analysts predict a pickup, with future revenue expected to grow at an average yearly rate of 8.65%.

- Positive Future View: The growth story is expected to persist, with EPS predicted to grow by 17.64% yearly in the coming years. This forward-looking strength is important for a GARP strategy, as it shows the company's growth is still active.

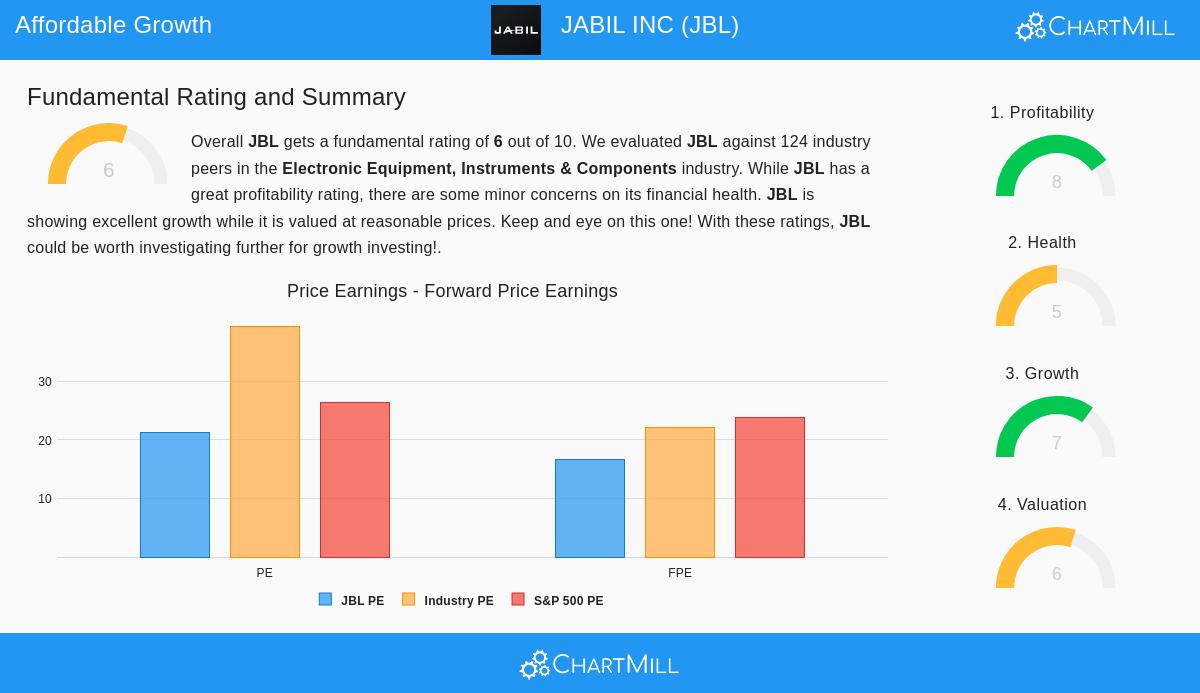

A Fair Valuation

Finding growth is only part of the task, making sure you are not paying too much for it is the other essential part. Jabil receives a Valuation Grade of 6, showing its current price is not a major hurdle. Several measures back this view.

- Appealing Relative Price: While Jabil's Price-to-Earnings (P/E) ratio of 21.32 may appear high alone, it is clearly less expensive than 76% of similar companies in the Electronic Equipment, Instruments & Components industry, where the average P/E is above 39.

- Forward-Looking Measures Are Appealing: The view becomes more positive when looking forward. Jabil's Price/Forward Earnings ratio of 16.72 is less expensive than almost 80% of its industry peers and is below the wider S&P 500 average.

- Cash Flow and EBITDA Backing: The stock also appears inexpensive based on cash creation, with its Price/Free Cash Flow and Enterprise Value/EBITDA ratios grading more positively than over 80% of industry rivals.

Supporting Fundamentals: Profitability and Condition

For growth to be lasting and the valuation to be reasonable, a company must be profitable and financially stable. Jabil's high Profitability Grade of 8 is a notable positive, while its average Condition Grade of 5 presents an area for investor review.

Profitability Positives: Jabil is very good at creating returns on capital. Its Return on Equity (ROE) of 52.31% and Return on Invested Capital (ROIC) of 24.71% are very high, doing better than most of its industry. This shows very efficient use of shareholder and invested capital, a key trait for a growth company.

Financial Condition Points: The company's financial condition shows a varied picture, which is why it receives a neutral 5. On the good side, Jabil creates notable value, as its ROIC is much higher than its cost of capital, and it has been lowering its share count. Its debt, compared to its free cash flow, is workable. However, investors should note its low liquidity ratios (Current and Quick Ratios below 1), which suggest a constrained working capital position and possible weakness in meeting immediate obligations. This is offset by a firm Altman-Z score, showing no short-term bankruptcy concern.

Conclusion

Jabil Inc presents an example in the affordable growth screening process. It shows the effective mix of good, double-digit earnings growth and a forward-looking valuation that is appealing compared to both its industry and the wider market. Its high profitability measures, particularly its very good returns on capital, give fundamental backing for its growth story. While its low liquidity ratios deserve notice, the overall fundamental picture matches the aim of finding companies where growth possibility is not completely shown in a high stock price.

For investors wanting to examine other companies that match this "Affordable Growth" profile, you can see the full screening rules and view more results via this link. A detailed look at Jabil's fundamental grades is available in its full fundamental analysis report.

Disclaimer: This article is for informational purposes only and does not constitute financial advice, a recommendation, or an offer to buy or sell any security. Investors should conduct their own research and consult with a qualified financial advisor before making any investment decisions.