For investors looking for chances in the market, the disciplined method of value investing stays a key strategy. Its foundation is finding companies whose present market price seems to be below their actual worth. This difference, frequently caused by temporary market feeling instead of lasting basics, can offer a possible opening for steady investors. An essential step in this work is a complete basic analysis, reviewing a company's financial condition, earnings, path of expansion, and price assessment to judge its real value. One way to simplify this hunt is by using methodical filters that sort for stocks showing the signs of a value possibility: good basic business measures combined with a low price.

A recent filter using this "Decent Value" method has pointed to ITRON INC (NASDAQ:ITRI) as a stock needing more review. The filter aims to find stocks with a high valuation score, meaning they are low-priced compared to their basics, while also keeping acceptable scores in earnings, financial condition, and expansion. This pairing is key for value investors; a low-priced stock is only a worthwhile find if the company is basically healthy and can have its market price later match its business quality. ITRON, a company offering technology and services for checking and handling energy and water use, seems to match this description based on its newest basic analysis.

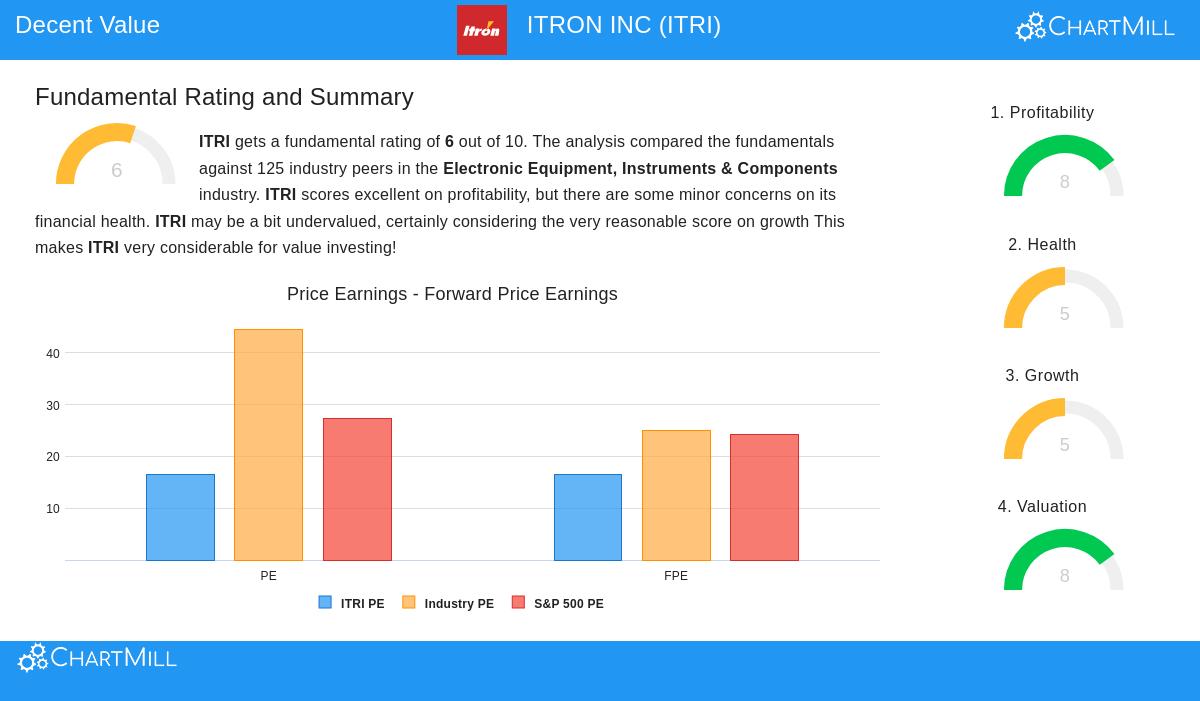

Valuation: The Base of the Idea

The main attraction of ITRON from a value view is in its valuation measures, which indicate the stock is priced low relative to both its field and the wider market. For value investors, a low valuation is the beginning, offering that important "margin of safety" Benjamin Graham stressed.

- Price-to-Earnings (P/E) Ratio: ITRI's P/E ratio of 16.59 is viewed as low within its Electronic Equipment, Instruments & Components field, doing better than 84.68% of similar companies. More widely, it rests under the present S&P 500 average of 27.38.

- Forward P/E Ratio: The view stays the same looking forward, with a forward P/E of 16.42 that is lower than 83.06% of field rivals and under the S&P 500 forward average.

- Cash Flow & EBITDA Multiples: The valuation argument is made stronger by measures like Price/Free Cash Flow and Enterprise Value/EBITDA, where ITRI is priced lower than over 90% and 80% of its field peers, in order.

This group of data shows the market is using a large price reduction to ITRON's earnings and cash flows compared to alike companies, a standard beginning place for value-focused study.

Profitability and Financial Health: Judging the Base

A low valuation by itself can be a "value trap" if the company's business is weakening. So, judging profitability and financial health is required. ITRON's report shows a good earnings profile, which helps lower that risk.

The company gets a high profitability score of 8 out of 10. Main strong points contain:

- Good Margins: A Profit Margin of 10.69% and an Operating Margin of 12.51% are some of the top in its field, doing better than 86% and 80% of peers. These margins have also shown gain in recent years.

- Firm Returns: Returns on Assets (6.94%) and Equity (15.21%) are also above field averages, showing efficient use of money.

Financial health, with a score of 5, shows a more varied but acceptable view. Good points contain a comfortable Current Ratio of 2.17 and an acceptable Debt-to-Free-Cash-Flow ratio of 3.65, suggesting enough cash availability and a workable debt amount relative to cash creation. A main point to watch is that the company's Return on Invested Capital (ROIC) is now under its cost of capital, which is an item for investors to check. However, the report also states that the newest ROIC number is increasing and above its three-year average, a possible signal of good direction.

Growth Path: The Driver for New Valuation

For a value investment idea to succeed, there must be a way for the business to expand or get better, thus leading the market to reconsider its price. ITRON's growth score of 5 shows a change.

- Earnings Growth is Speeding Up: While sales expansion has been flat in the past, the company has reached an 11.11% average yearly growth in Earnings Per Share (EPS) over recent years. Importantly, this speed is expected to continue, with experts predicting EPS growth of over 13% yearly in the next years.

- Sales View Gets Better: After a time of level sales, future expansion is expected to be positive at almost 5% per year. The report clearly says that both EPS and sales growth rates are speeding up.

This expected speed increase is critical. It offers a basic reason that could help reduce the space between ITRON's present market valuation and its actual value, which is a key process value investors look for.

Conclusion

ITRON INC presents a situation that matches several value investing ideas. The stock is priced with a clear markdown to its field and the market based on normal earnings and cash flow measures. This low price exists together with clearly good profitability and gaining return measures. While its financial health has some details to note, its cash availability is good. Most significantly, the company is in a time of speeding earnings growth with a positive sales view, offering a basic ground for possible market re-pricing.

Naturally, this study is a beginning place. Value investing needs full careful research into competitive edges, management skill, and field directions, items of judgment outside a numbers-based report. Investors should think about these parts together with the financial facts before making any choices.

Interested in reviewing other stocks that match this "Decent Value" description? You can use the same filter used to find ITRI and see the present outcomes here.

Disclaimer: This article is for information only and is not financial advice, a suggestion, or a deal or request to buy or sell any securities. The study is based on data and scores from ChartMill, and investors should do their own separate research and talk with a qualified financial advisor before making any investment choices. Past results do not show future outcomes.