The investment philosophy of legendary fund manager Peter Lynch focuses on finding well-run, growing companies available at sensible prices—a strategy often called Growth at a Reasonable Price (GARP). Lynch supported a long-term, buy-and-hold method, concentrating on firms with durable earnings growth, sound financial condition, and clear business models. His process uses particular quantitative filters to locate prospects, highlighting items such as a modest but steady earnings growth rate, a low Price/Earnings to Growth (PEG) ratio, good profitability, and a prudent balance sheet.

A recent filter constructed on these Lynch ideas has identified INTERPARFUMS INC (NASDAQ:IPAR) as a possible prospect. The company, which develops, manufactures, and distributes prestige fragrances under licensed brands like Coach, Jimmy Choo, and Montblanc, seems to match several important parts of the strategy.

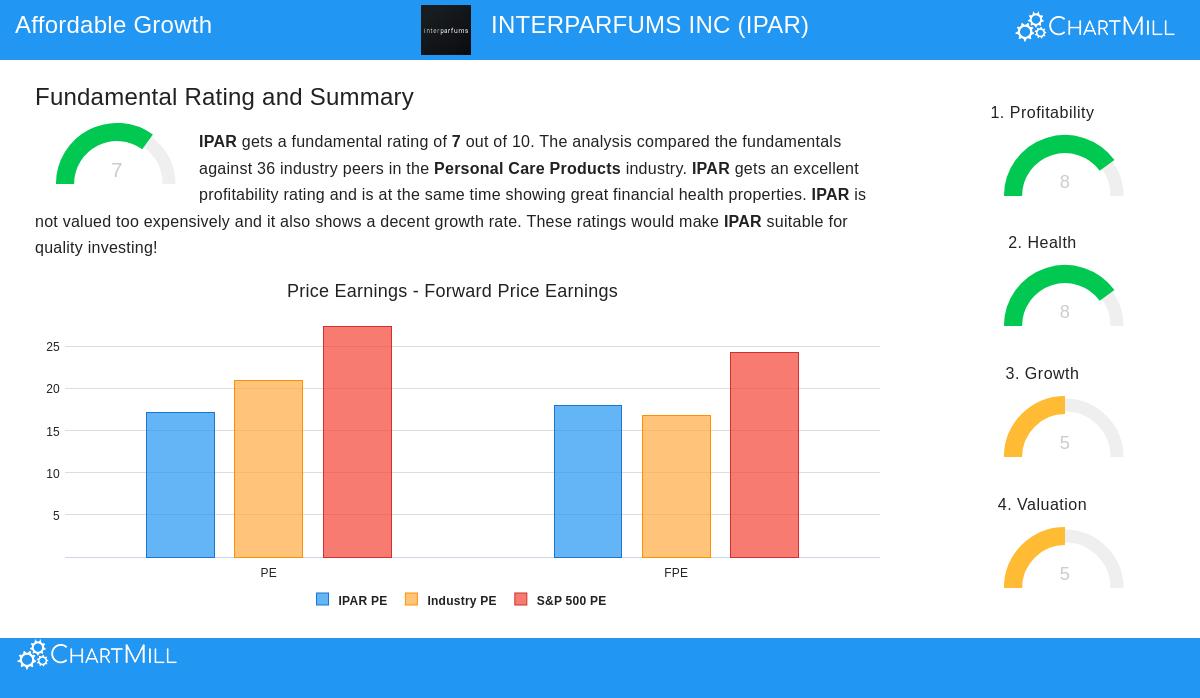

Matching the Lynch Standards

The filter looks for companies showing durable growth, sensible valuation when considering that growth, and financial soundness. Interparfums satisfies these central checks based on the supplied data:

- Durable Earnings Growth: Lynch looked for companies increasing earnings per share (EPS) between 15% and 30% each year over five years, a range seen as durable. Interparfums' five-year EPS growth rate of 22.3% sits directly within this target range, pointing to a firm and consistent historical rise in profitability.

- Sensible Valuation (PEG Ratio): A key part of Lynch's process is the PEG ratio, which measures a stock's Price-to-Earnings (P/E) ratio against its growth rate. A PEG of 1.0 or lower implies the stock may be sensibly priced relative to its growth. Interparfums' PEG ratio of 0.77 indicates its valuation is not excessive when its historical growth is considered, a good signal for value-aware growth investors.

- Good Profitability (Return on Equity): Lynch preferred companies that produce high returns on shareholder equity, a mark of efficient management. The filter demands an ROE above 15%. Interparfums' ROE of 18.9% easily passes this level, showing the company's capacity to profitably reinvest its earnings.

- Financial Condition (Current Ratio & Debt/Equity): A sound balance sheet is essential for enduring economic cycles. The filter requires a Current Ratio above 1.0 and a Debt-to-Equity ratio below 0.6. Interparfums performs well here, with a Current Ratio of 3.27, showing sufficient liquidity, and a very low Debt/Equity ratio of 0.17, indicating little dependence on debt financing—a trait Lynch especially appreciated.

Fundamental Condition Review

A wider fundamental analysis of Interparfums supports the image shown by the Lynch filter. The company receives a good total fundamental rating, with specific strong points in profitability and financial condition.

Its profit margins are solid and have been getting better, while returns on assets and invested capital score well inside the personal care products industry. The condition score is supported by very good solvency measures, including a very low debt-to-free-cash-flow ratio and a high Altman Z-score, which implies low bankruptcy risk. The main areas noted for review are a slowdown in anticipated future growth rates compared to the past and a dividend payout ratio that could be high relative to earnings growth.

Investment Case for the Long Term

For an investor using a Lynch-style GARP framework, Interparfums offers a strong case. The company works in the durable luxury fragrance category, using a collection of established brand licenses with global fame. Its financials display the characteristics Lynch favored: a record of significant but not excessive earnings growth, high profitability, and a very strong balance sheet with almost no net debt. The present valuation, as shown by the below-1.0 PEG ratio, does not seem to completely account for this quality and stability, possibly providing a good entry point for a long-term owner.

The Lynch strategy is naturally patient, concentrating on business results over years instead of months. Interparfums' model—producing consistent cash flow from enduring luxury brands—fits the "clear" business profile Lynch suggested. While future growth is estimated to slow, the company's financial soundness gives a notable margin of safety and the ability to handle market changes or fund new brand partnerships.

Reviewing Other Possibilities

Interparfums is one of multiple companies that currently pass the organized filter based on Peter Lynch's investment ideas. Investors curious about examining other possible prospects that meet these standards for durable growth at a sensible price can review the complete filter results here.

Disclaimer: This article is for informational purposes only and does not constitute financial advice, a recommendation to buy or sell any security, or an endorsement of any investment strategy. Investors should conduct their own thorough research and consider their individual financial circumstances and risk tolerance before making any investment decisions.