For investors looking for a disciplined, long-term method to build wealth, few strategies have the substance of Peter Lynch's approach. As described in his book One Up on Wall Street, Lynch’s thinking focuses on finding expanding companies that are available at sensible prices, a concept often called Growth at a Reasonable Price (GARP). His method uses fundamental filters to locate businesses with lasting earnings increase, sound financial condition, and good value, preferring those that could be missed by Wall Street. A recent filter using these Lynch ideas has pointed to InMode Ltd (NASDAQ:INMD) as a candidate worth further review for the GARP-oriented investor.

A Sound Match for Central Lynch Measures

The Peter Lynch filter uses particular numerical checks to search for companies that mix increase and value. InMode Ltd seems to satisfy these central needs, which are made to find lasting business models instead of short-lived market movements.

- Lasting Earnings Increase: Lynch preferred companies with solid, but not extreme, increase, thinking overly high rates are not lasting. The filter seeks a 5-year EPS increase rate between 15% and 30%. InMode states a trailing 5-year EPS increase rate of 23.0%, putting it directly within this "ideal range" of sound yet possibly sustainable growth.

- Good Value Compared to Increase: Maybe the central idea of the GARP method is the PEG ratio (Price/Earnings to Growth), which Lynch famously used. A PEG of 1 or less implies a stock may be sensibly priced relative to its increase path. InMode’s PEG ratio, based on its past increase, is 0.39, suggesting the market may be pricing its historical increase performance well below its worth.

- Outstanding Financial Condition: Lynch required companies with firm balance sheets to endure economic periods. Two important filters are a Debt/Equity ratio under 0.6 and a Current Ratio above 1. InMode does very well here, stating no debt (a Debt/Equity of 0.0) and a very strong Current Ratio of 9.75, indicating more than enough cash to cover near-term needs.

- High Profit Generation: A minimum Return on Equity (ROE) of 15% makes sure the company is effectively creating profits from shareholder equity. InMode’s ROE of 22.9% easily passes this mark, showing capable management and a successful business model.

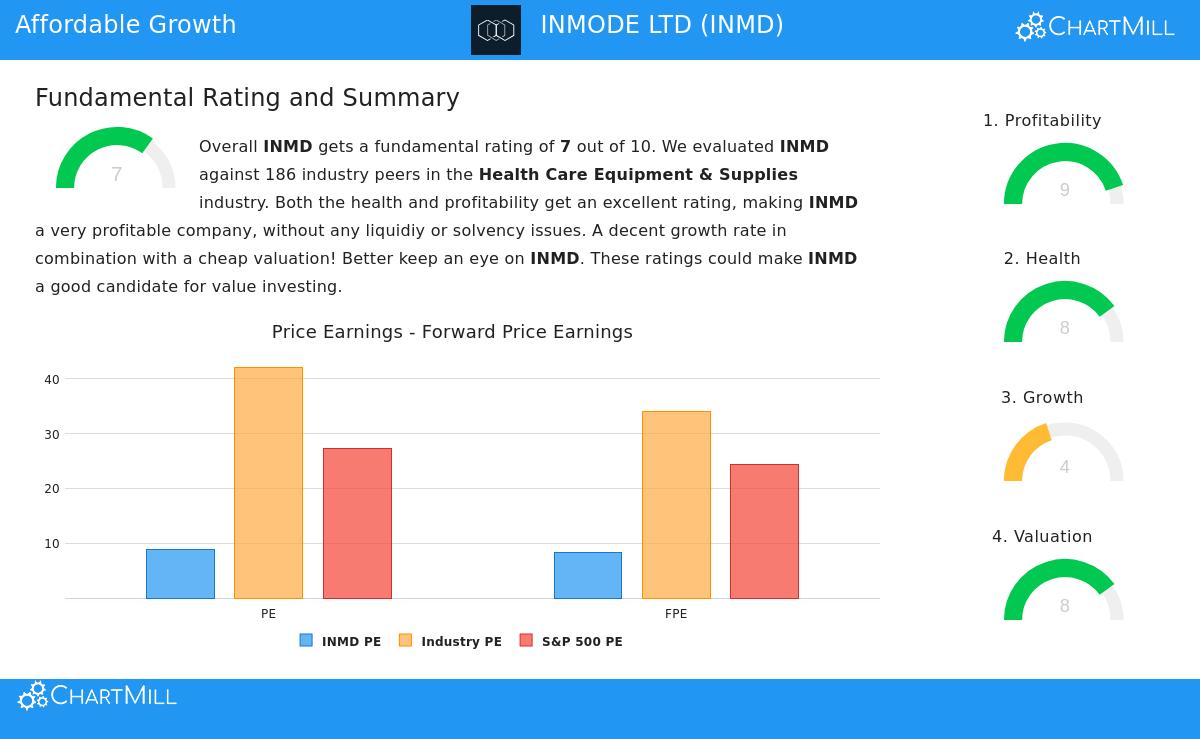

Broad Fundamental Review

A wider fundamental review of InMode supports the image shown by the Lynch filter. The company receives a sound total fundamental score of 7 out of 10, with specific high points in profit generation and financial condition.

Its profit generation numbers are excellent, with profit and operating margins that place in the highest group of its Health Care Equipment & Supplies industry group. The company’s perfect solvency score, supported by its lack of debt, and better liquidity ratios highlight a very strong balance sheet. From a value standpoint, InMode sells at a P/E ratio of 8.91, which is not only low compared to the wider S&P 500 but is also below about 95% of its industry rivals. This mix of high profit generation and low price is a traditional sign looked for by value and GARP investors.

However, the review also points out areas for investor examination, mainly related to increase. While the long-term history is sound, recent results show a drop in both revenue and earnings per share over the last year. Also, future increase projections for revenue and EPS are currently low. This situation shows a key part of the Lynch method: the filter gives a beginning place for study, not a purchase recommendation. Investors must look further to learn the causes for this increase slowdown, whether it is a short-term market change, more rivalry, or a periodic decline, and judge if the company’s long-term increase potential stays valid.

You can review the full, detailed fundamental analysis for INMD here.

Summary and Next Steps

InMode Ltd offers an interesting example for the Peter Lynch investment method. It meets the numerical filters for lasting historical increase, low price based on that increase (PEG), and very firm financial condition. For the GARP investor, these are exactly the basic qualities that can point to a good company selling at a good price, possibly giving a good balance of risk and return over the long term.

The needed next study step, as Lynch stressed, is important. Investors should examine the company’s product development, competitive place in the aesthetic medical device field, and management’s plan for returning to increase. The company’s lack of debt and large cash holdings give important room to handle difficulties or seek chances.

For investors wanting to find other companies that match this disciplined GARP method, you can use the live Peter Lynch filter yourself. Click here to see the current filter results and change the settings for your own study.

Disclaimer: This article is for information only and does not make up financial guidance, a suggestion, or an offer to buy or sell any security. The Peter Lynch method and fundamental review are subjective frameworks. All investment choices include risk, including the possible loss of initial investment. Investors should do their own complete study and think about their personal financial situation and risk comfort before making any investment choices.