The investment philosophy of Peter Lynch, the legendary manager of the Fidelity Magellan Fund, has long been a cornerstone for investors seeking to build wealth over the long term. His approach, often categorized as Growth at a Reasonable Price (GARP), focuses on identifying companies with strong, sustainable growth potential that are not overvalued by the market. It’s a strategy that prioritizes fundamental health and understandable business models over speculative trends. A screen based on Lynch’s key criteria, such as strong earnings growth, high profitability, sound financial health, and an attractive valuation, can find companies that align with this disciplined framework. One such company that recently emerged from this screen is INMODE LTD (NASDAQ:INMD).

Alignment with Peter Lynch's Core Criteria

Peter Lynch advocated for investing in companies with a clear, sustainable growth trajectory that an individual investor can understand. The filters applied in a Lynch-inspired screen are designed to isolate businesses that meet this pragmatic standard. InMode’s profile shows a strong alignment with several of these rules:

- Sustainable Earnings Growth: Lynch favored companies growing earnings per share (EPS) between 15% and 30% annually, as growth beyond that rate is often unsustainable. InMode’s five-year average EPS growth of approximately 23% falls squarely within this target range, indicating a history of strong, but not hyper-aggressive, expansion.

- Attractive Valuation via PEG Ratio: A central part of the GARP approach is the Price/Earnings to Growth (PEG) ratio, which Lynch insisted should be at or below 1. This metric adjusts the standard P/E ratio for a company’s growth rate, helping to identify stocks that may be undervalued relative to their growth potential. InMode’s PEG ratio, based on its past five-year growth, stands at an exceptionally low 0.40, suggesting the market may be significantly undervaluing its historical growth profile.

- Exceptional Profitability (ROE): Lynch looked for companies that efficiently generate profits from shareholder equity, with a Return on Equity (ROE) above 15% being a key benchmark. InMode’s ROE of nearly 23% not only comfortably exceeds this threshold but also ranks within the top tier of its industry peers, signaling highly effective management and a strong business model.

- Strong Financial Health: A prudent balance sheet was non-negotiable for Lynch. He preferred companies with little to no debt and strong short-term liquidity. InMode performs well here, having a Debt/Equity ratio of 0.0, meaning it operates with no interest-bearing debt. Furthermore, its Current Ratio of 9.75 indicates a large capacity to cover short-term obligations, providing a significant margin of safety.

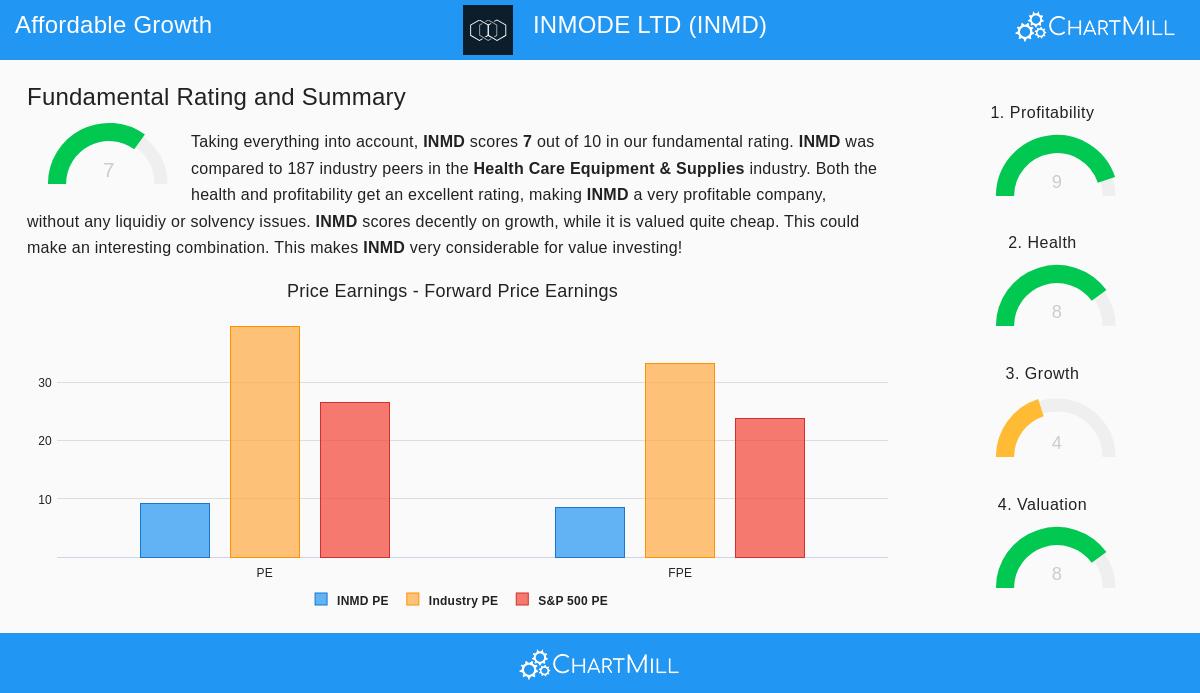

Fundamental Health and Valuation Summary

A deeper look at InMode’s fundamental report reinforces the picture painted by the screen. The company earns a high overall fundamental rating, driven by standout scores in profitability and financial health. Its profit margins are among the best in the Health Care Equipment & Supplies industry, and its complete lack of debt is a rare and notable strength. From a valuation perspective, InMode appears notably cheap. Its P/E ratio of 9.1 and forward P/E of 8.5 are a fraction of both the industry average and the broader S&P 500, presenting a clear value proposition.

However, a Lynch-style investor would also note areas for further research. The most recent year showed a contraction in both revenue and earnings, and analyst expectations for near-term growth are currently muted. This highlights Lynch’s principle that a screen is only a starting point for deeper due diligence. The investor’s task would be to understand the reasons behind the recent slowdown, whether it’s a temporary setback, a cyclical downturn, or a more fundamental challenge, and assess the company’s ability to return to its historical growth path. The strong balance sheet provides ample resources to manage any turbulence.

A Candidate for the Long-Term Portfolio

For an investor adhering to the Peter Lynch methodology, InMode presents a notable case study. It operates in the understandable, albeit competitive, field of minimally-invasive aesthetic medical technology. The company demonstrates the characteristics Lynch valued: a history of strong profitability, a very strong balance sheet with no debt, and a valuation that appears to offer a substantial margin of safety relative to its past performance. While recent results introduce a note of caution that warrants investigation, the foundational financial strengths align closely with the criteria for a long-term, growth-at-a-reasonable-price holding.

The screen that identified InMode is based on a timeless strategy focused on fundamental quality and sensible valuation. You can explore the current results of this Peter Lynch-inspired screen and discover other potential candidates here.

Disclaimer: This article is for informational purposes only and does not constitute financial advice, a recommendation, or an offer to buy or sell any securities. The mention of specific securities is for illustrative and educational purposes related to the discussed investment strategy. Investors should conduct their own thorough research and consider their individual financial circumstances and risk tolerance before making any investment decisions. Past performance is not indicative of future results.