For investors looking to find companies trading below their estimated true value, a systematic filtering process is important. One useful technique is to look for stocks that show a good fundamental valuation score, meaning they might be priced low compared to their financial statements, while also holding firm scores in profitability, financial condition, and expansion. This technique tries to find possible situations where the market could be misjudging a company's lasting earnings ability and sound finances, a central idea of value investing. A recent filter using these measures has pointed to Incyte Corp (NASDAQ:INCY) as a stock needing more examination.

Valuation: An Interesting Entry Point

The main attraction of Incyte from a value view is its valuation measures, which seem appealing compared to both its sector and the wider market. For value investors, a low valuation relative to earnings and cash flow is the first step, hinting at a possible buffer.

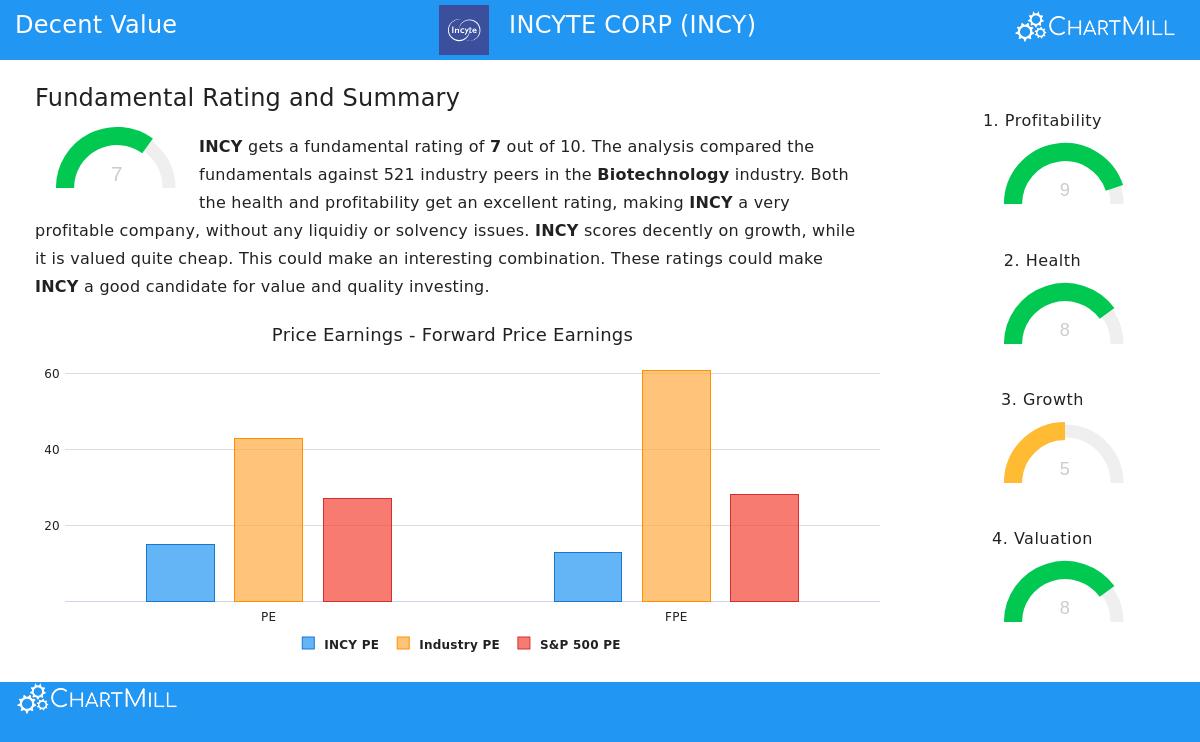

- Price-to-Earnings (P/E): Incyte's P/E ratio of 14.92 is much lower than the biotechnology sector average of 42.71. The company is less expensive than about 96% of its sector competitors on this measure.

- Forward P/E: Looking forward, the situation stays alike with a forward P/E of 12.65, compared to a sector average of 60.80.

- Enterprise Value to EBITDA & Price/Free Cash Flow: Both the EV/EBITDA and Price/FCF ratios also point to a low valuation inside the biotech field, doing better than over 96% of peers.

These ratios imply the market is valuing Incyte cautiously. When paired with good fundamentals in other areas, this can indicate an underpriced condition instead of a company in basic trouble.

Profitability and Financial Condition: A Firm Base

A low valuation by itself can be misleading if the company's core business is poor. However, Incyte scores very well on profitability and condition, giving the stable base value investors look for. Good profitability confirms the earnings ability is genuine, while sound financial condition lowers failure risk and allows for adaptability.

Profitability Quality: Incyte receives a high ChartMill Profitability Rating of 9 out of 10. Important strong points contain:

- High Margins: The company has a profit margin of 25.03% and an operating margin of 26.12%, putting it in the best group of its sector.

- Good Returns: Return on Assets (18.49%), Return on Equity (24.90%), and Return on Invested Capital (19.49%) all notably do better than most biotech peers.

- Steady Cash Creation: The company has been steadily profitable and produced positive operating cash flow in each of the last five years.

Financial Condition Quality: With a Condition Rating of 8, Incyte's balance sheet is sound.

- Low Debt: The company holds very little debt, with a Debt/Equity ratio of 0.01 and a Debt to Free Cash Flow ratio of only 0.03, meaning it could clear all its debts in a short time from its cash flow.

- Good Solvency: An Altman-Z score of 8.72 signals very little near-term failure risk.

- Sufficient Liquidity: A Current Ratio of 3.32 and a Quick Ratio of 3.25 show more than enough means to meet immediate responsibilities.

This pairing of high profitability and a strong balance sheet means the company's low valuation is not due to financial trouble, making it a more interesting stock for more study.

Growth: A Varied but Detailed Image

Growth is the last part of the analysis. While future growth projections are moderate, the past record gives needed background. For a value investor, knowing the growth path helps judge if current earnings are maintainable.

Past Growth Has Been Good:

- Earnings Per Share (EPS) increased by a notable 414% over the previous year and has displayed a good average yearly growth rate of 34.67% over recent years.

- Revenue rose by 21.22% last year and has increased at an average yearly rate of 14.03%.

Future Projections Are Moderate: Analyst estimates point to expected decreases in both EPS (-7.86%) and Revenue (-1.16%) on average over the coming years. This expected slowdown probably adds to the stock's low valuation. The central issue for investors is if this view is already completely factored into the price, or if it offers an excessively negative outlook for a company with Incyte's established profitability and future products.

Conclusion and Next Steps

Incyte Corp shows a standard profile for value-focused review: a stock selling at a markdown to its sector based on common valuation multiples, yet supported by excellent profitability and a clean balance sheet. The principal area of discussion focuses on its growth prospects. The task for investors is to decide if the market has overreacted to a possible growth slowdown, thus making a chance, or if the reduced growth projections are correct.

The "Decent Value" filter that found Incyte is made to find exactly this kind of stock, companies where good fundamentals meet a fair price. For investors wanting to study similar situations, you can view the full fundamental analysis report for INCY here.

Find Other Possible Value Stocks This review of Incyte Corp came from a methodical filter for stocks with firm valuation, profitability, condition, and growth traits. If you want to examine other companies that currently fit like measures, you can study the full filter findings here.

,

Disclaimer: This article is for informational purposes only and does not constitute financial advice, a recommendation, or an offer or solicitation to buy or sell any securities. The analysis is based on data provided and filtering techniques that may have limits. Investors should do their own complete research and think about their personal financial situation and risk willingness before making any investment decisions.