For investors looking for a mix of chance and caution, the "Growth at a Reasonable Price" (GARP) method presents a good middle path. This method looks for companies with good and lasting growth, but importantly, sidesteps those with prices that are too high. The aim is to locate firms where the possible future growth is not already completely, or too much, reflected in the present share price. One way to find these companies is by using a structured filter of basic measures, searching for good growth, firm basic financial condition, and good profit, all while checking the price stays fair.

Harmony Biosciences Holdings (NASDAQ:HRMY) recently appeared from this "Affordable Growth" filter. The filter aims to find shares with a high growth score (above 7 out of 10), along with acceptable scores for profit and financial condition, and a price score above 5 to avoid names that are too costly. HRMY's basic picture indicates it deserves more attention from investors using this careful method.

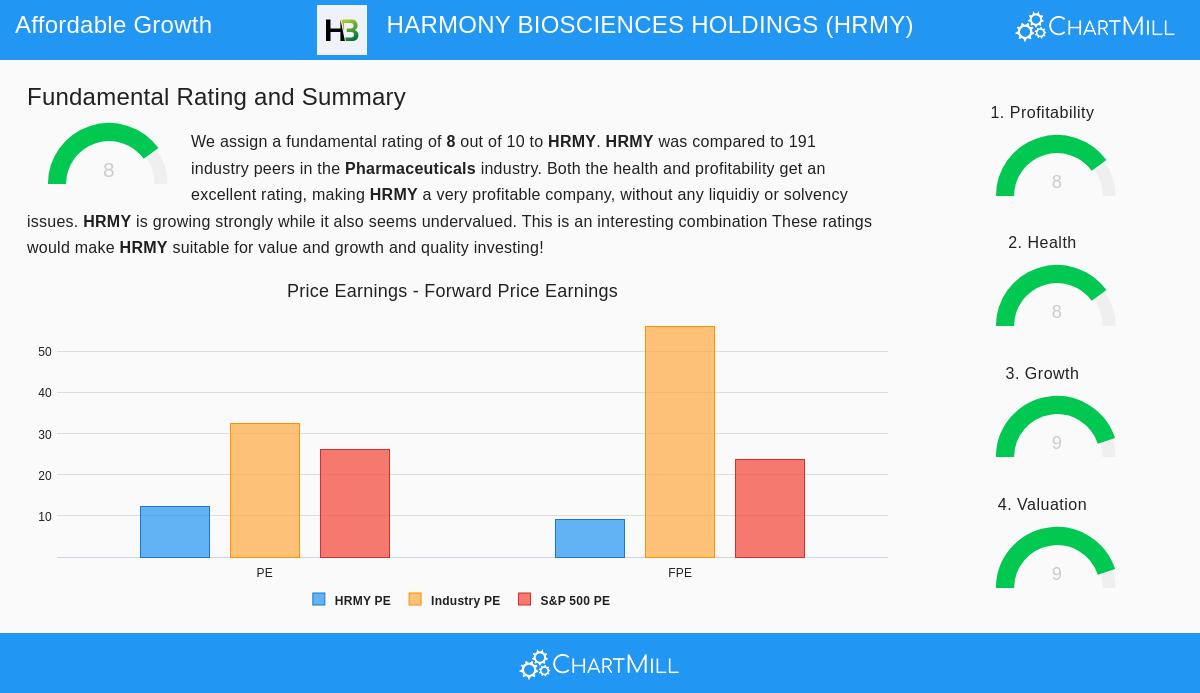

A Good Growth Picture

The central part of the GARP method is, expectedly, growth. Harmony Biosciences performs very well here, getting a top-level Growth Score of 9. The company is not only growing, it is speeding up at a notable rate, pushed by its main product, WAKIX, for narcolepsy.

- Fast Sales Increase: Over the last few years, HRMY has seen an average yearly sales growth near 160%. In the latest year, sales rose by a good 21%.

- Good Profit Growth: This sales strength is reaching the profit. Earnings Per Share (EPS) increased by more than 50% last year and has averaged close to 45% yearly growth in the past.

- Positive Future View: Experts think this pace will keep going, with future EPS growth guesses averaging about 35% each year. While this is a slowdown from the very fast past rates, it is still a very good view that supports the growth idea.

Price: The "Fair Price" Point

Finding good growth is only part of the task, the other key part is making sure you do not pay too much for it. This is where Harmony Biosciences is notable, having a Price Score of 9. The company's present share price seems to give a way to its growth path at a fairly low multiple.

- Good Earnings Multiples: HRMY sells at a Price-to-Earnings (P/E) ratio of 12.2, which is much lower than the present S&P 500 average of about 26.2. Its future P/E ratio, from next year's earnings guesses, is even more interesting at 9.2.

- Less Costly than Industry Companions: This price difference is even clearer inside its own drug industry. HRMY is less costly than about 89% of its industry companions based on its future P/E ratio.

- Good Free Cash Flow Price: The company also seems interesting on a cash flow basis, with a Price-to-Free Cash Flow ratio that is lower than almost 95% of industry rivals.

This mix of high growth and low relative price makes the key "affordable growth" situation. The low PEG ratio, which changes the P/E for growth, further shows the market may not be fully accounting for the company's expected earnings increase.

Supported by Firm Basics

For growth to be lasting and the price to be reliable, a company needs a solid financial base. The GARP method clearly filters for acceptable condition and profit to avoid "price traps" or financially weak growth stories. HRMY scores high here too, with Condition and Profit Scores of 8 each.

- Financial Condition & Stability: The company shows a firm balance sheet. Its Altman-Z score of 5.66 points to a very low short-term bankruptcy danger. Importantly, its Debt-to-Free Cash Flow ratio is a very good 0.57, meaning it could in theory clear all its debt in under seven months using its present cash flow creation, a sign of great financial room.

- High Profit Margins: HRMY is not only growing sales, it is doing so with profit. Its operating margin over 27% and net profit margin of 22.5% place in the top part of its industry. A gross margin close to 78% shows a firm pricing ability for its specific neurology products.

- Effective Capital Use: The company creates notable returns on its used capital (ROIC of 17.2%), which is much higher than its cost of capital, confirming it is building real shareholder value.

Conclusion

Harmony Biosciences shows a standard example for the Growth at a Reasonable Price method. The company is in a strong growth period, driven by its market success in treating rare nerve conditions. Importantly, this growth story is backed by very good profit and a very firm financial state, reducing the dangers often linked to high-growth biopharma shares. Maybe most interesting for investors is that this combination is available at a price that seems low both in simple terms and compared to its industry, suggesting the market may be setting too low a value on its future possibility.

The "Affordable Growth" filter that found HRMY is made to systematically locate such chances. If you want to look at other shares that fit similar needs of strong growth, firm basics, and fair price, you can use the filter yourself here.

Disclaimer: This article is for information only and is not financial advice, a suggestion, or a bid to buy or sell any securities. The study uses data and scores from ChartMill.com, and investors should do their own research and talk with a qualified financial advisor before any investment choices. Past results do not show future outcomes.