For investors looking to balance the search for growth with prudence, the Growth At a Reasonable Price (GARP) method presents a strong middle path. This method looks for companies with good and lasting growth, but importantly, avoids those with very high prices. The aim is to find good businesses where the future earnings possibility is not already completely, or overly, shown in the present share price. One way to find these companies is through a structured search for "affordable growth," which selects for shares with high growth scores, good basic profit and financial strength, and a price that does not seem too high.

Harmony Gold Mining Co. Ltd. (NYSE:HMY) recently appeared from this kind of search. As a large gold and copper producer working mainly in South Africa and Papua New Guinea, HMY works in the changing and capital-heavy metals and mining industry. The company's basic profile, however, shows a notable mix of strength and price that fits the affordable growth idea.

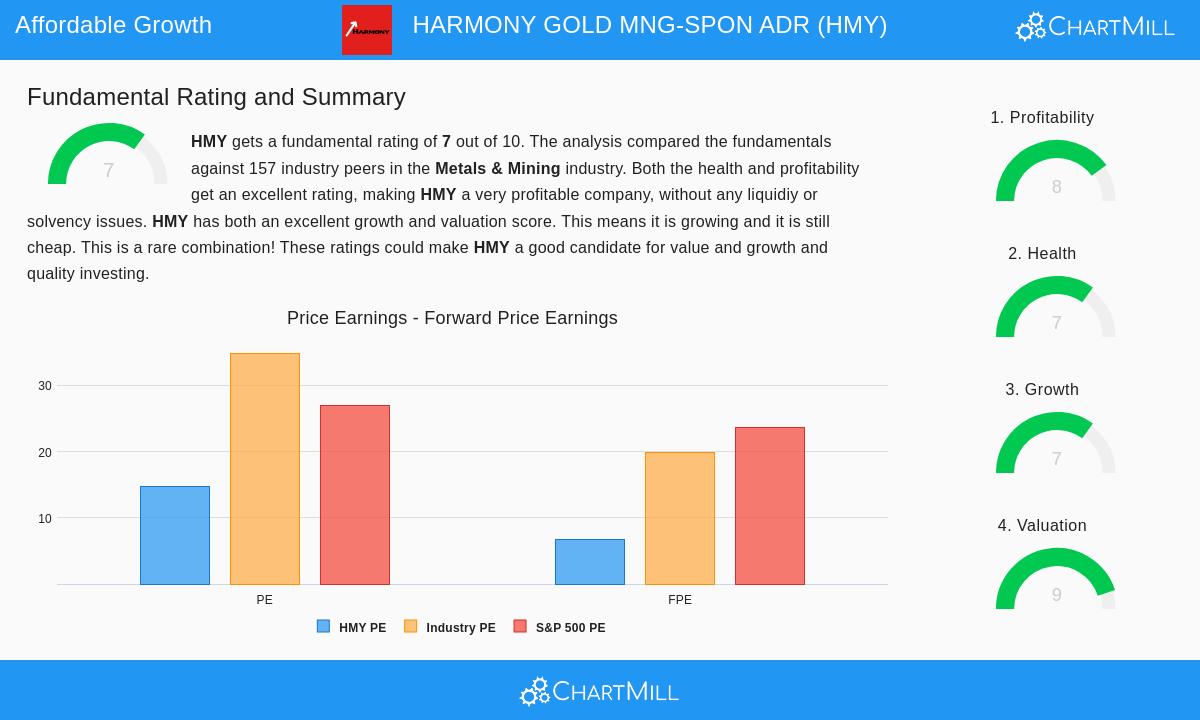

A Strong Price Profile

The central part of the GARP method is finding growth that is fairly priced, and HMY's price measures are a clear strength. According to ChartMill's basic analysis, the share gets a top-level Price Rating of 9 out of 10 when measured against others in its industry.

- Forward-Looking Measures Are Especially Appealing: While the standard Price-to-Earnings (P/E) ratio of 14.72 matches wider market numbers, the forward P/E ratio of 6.65 shows the market is pricing the share at a large discount to its expected near-term earnings. This ratio is lower than about 95% of companies in the metals and mining industry.

- Good Price on Cash Flow and Enterprise Basis: The price appeal goes beyond earnings. HMY also looks low-priced based on its Price-to-Free-Cash-Flow and Enterprise-Value-to-EBITDA ratios, doing better than most of its industry rivals on these measures.

- Growth Consideration: The low PEG ratio, which changes the P/E for expected earnings growth, further shows the share's present price may not fully account for its planned growth path.

For an investor, this price view suggests the market may be using a general industry discount or missing company-specific gains, possibly giving a chance to buy before future growth happens.

Strong and Increasing Growth

A low-priced share is only a good find if the company is expanding, and HMY's growth story is strong. The company gets a Growth Rating of 7, backed by good results in both recent reports and future estimates.

- Notable Past Growth: In the last year, HMY achieved very high growth in Earnings Per Share (EPS) of almost 67%, with a solid 20% rise in Revenue. This is not a single event, as the company has kept an average yearly revenue growth above 20% in recent years.

- Positive Future View: Analyst estimates support the growth story. EPS is expected to grow at an average yearly rate over 25%, with revenue projected to rise by almost 15% per year. This forward-looking strength is key for the GARP method, as it gives a basic reason for the investment idea beyond past performance.

The mix of strong past speed and a positive forward view creates a believable growth profile that warrants investor notice, particularly next to its price.

Supporting Basics: Profit and Financial Strength

An affordable growth share must be more than just low-priced and growing; it needs a solid base. HMY's high Profit Rating of 8 and good Strength Rating of 7 give this important support, lessening some risks natural to its industry.

- Excellent Profit Measures: The company's return figures are standout numbers. Its Return on Invested Capital (ROIC) of 20.6% and Return on Equity (ROE) of nearly 23% are some of the best in the industry, doing better than over 94% of peers. These numbers show management is using capital well and creating large profits from its mining operations. Also, both operating and gross margins have shown good directions in recent years.

- Good Financial Soundness: From a balance sheet view, HMY shows clear strength. Its Altman Z-Score points to very low near-term bankruptcy risk, and its debt amounts are very manageable. The Debt-to-Equity ratio is a small 0.04, and the company could in theory pay all its debt with less than three months of free cash flow. This careful financial setup gives stability against material price changes and operational difficulties.

These factors are important for the method because they show the company's growth is built on a profitable and financially sound base, lowering the chance it will need to take on too much debt or weaken shareholder value to pay for its expansion.

Conclusion

Harmony Gold Mining Co. Ltd. presents an example in the affordable growth search method. The share meets the main needs: it is growing strongly with a clear path to continue, it is basically profitable and financially sound, and it is available at a price that seems to not include much of this positive view. While the mining industry holds specific risks linked to material prices, geopolitical issues, and operational results, HMY's present basic setup, marked by high returns, low debt, and low forward earnings estimates, makes it a clear choice for investors using a GARP view.

A full look at HMY's basic ratings across growth, price, profit, strength, and dividend can be seen in its full basic analysis report.

Investors curious about finding other companies that fit this profile of strong growth next to fair price and good basics can see more results using the Affordable Growth share search tool.

Disclaimer: This article is for information only and does not make financial advice, a suggestion, or an offer to buy or sell any security. Investing has risk, including the possible loss of principal. Readers should do their own study and talk with a qualified financial advisor before making any investment choices.