For investors looking to balance the search for growth with a degree of caution, the Growth at a Reasonable Price (GARP) method provides a solid middle path. This method tries to find companies that are increasing at a rate faster than average but are not valued at the extreme levels common to aggressive growth stocks. By looking for good fundamentals in growth, profit, and financial condition, while also requiring a sensible price, investors can try to reduce risk and prevent paying too much for future prospects. This process selects for stocks that are not only increasing, but are doing so from a foundation of quality and at a cost that is not high.

One stock that recently appeared using this "Affordable Growth" filter is Halozyme Therapeutics Inc (NASDAQ:HALO). The biopharmaceutical technology platform company, recognized for its ENHANZE drug delivery technology, shows a fundamental picture that matches the GARP idea well. A full fundamental analysis report on ChartMill gives HALO a total score of 7 out of 10, but more significantly, shows high scores in the main areas this method targets.

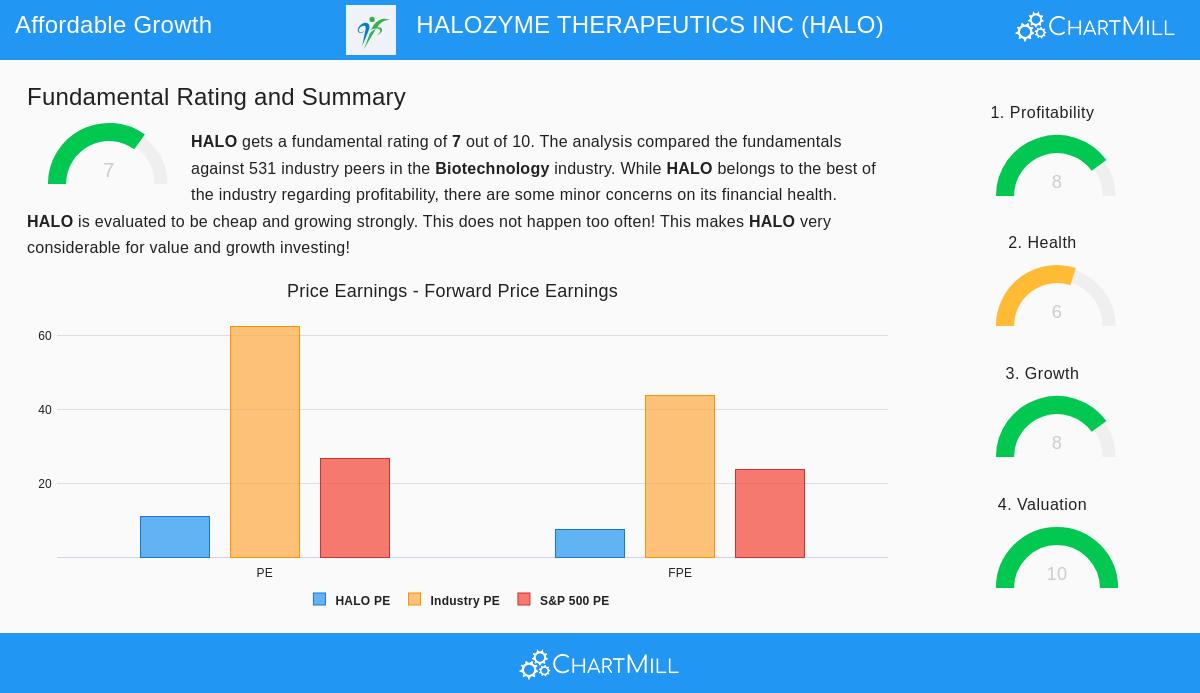

Notable Valuation Measures

The central idea of affordable growth is price, and this is where HALO does very well. The company’s valuation score is a full 10, showing it is priced very well compared to both its own financial results and similar companies. This score is important for the method, as a price that is too high can remove the gains from good growth if future hopes are not realized.

- Price-to-Earnings (P/E): At 11.05, HALO’s P/E ratio is much lower than the biotechnology industry average of about 62.5 and the wider S&P 500 average of 26.54. It costs less than 97% of similar companies in its field.

- Forward P/E: An even stronger number is the forward P/E of 7.50, which uses future earnings projections. This costs less than 99% of industry companies and is below one third of the S&P 500's forward P/E.

- Other Multiples: The good price extends to other measures, with the company also rating well on Enterprise Value to EBITDA and Price to Free Cash Flow ratios, doing better than over 97% of the industry in each case.

Solid and Continued Growth

A low-cost stock is only a poor investment if it does not grow. HALO’s growth score of 8 confirms it is not static, supplying the needed "growth" part of the GARP mix. The company has shown a notable ability to enlarge its business.

- Past Results: Over the last year, Earnings Per Share (EPS) increased by 48.55%, while Revenue went up by 31.19%. The longer-term history is more impressive, with an average yearly EPS increase of 30.12% and revenue increase of nearly 39% over recent years.

- Future Projections: Experts believe this progress will carry on, though at a slower rate. EPS is projected to increase by an average of 17.25% each year moving forward, with revenue growth estimated at 12.82%. While these numbers show a slowdown from the very fast past growth, they still indicate a solid and faster-than-average expansion path.

Supporting Fundamentals: Profit and Condition

For growth to last and the price to be reliable, a company must make a profit and be financially stable. HALO’s scores here give important backing for the idea.

Profit is a definite positive, with a score of 8. The company has very good margins and returns on capital:

- An operating margin of 59.33% and a profit margin of 47.91% put it in the best group of its industry.

- Return on Equity is a very high 118.17%, and Return on Invested Capital is 42.77%, both numbers doing better than most biotech peers.

Financial Condition gets a score of 6, showing a mostly firm position with some points to watch. On the positive side, the company produces notable free cash flow, with a low debt-to-FCF ratio of 2.51, meaning it can easily handle its debts. The Altman-Z score also shows no short-term bankruptcy danger. One point to see is a Debt-to-Equity ratio of 1.59, which is somewhat high and indicates a considerable use of debt financing, a detail for investors to weigh within the whole condition view.

Conclusion

Halozyme Therapeutics makes a strong case as an "affordable growth" option. It joins a notably low price, a key feature of value investing, with a shown and projected faster-than-average growth picture. This pair of traits is the core of the GARP method. Good profit measures suggest the growth is of high quality and produced effectively, while an acceptable condition score provides a base of financial steadiness. The coming together of these points, low price multiples, good past growth, firm future projections, and high profit, makes HALO a stock that deserves more review for investors looking for growth without paying an excessive cost for it.

This review was built on a particular filter for affordable growth stocks. You can locate more investment options that match this description by using the Affordable Growth stock screener.

Disclaimer: This article is for information only and is not financial advice, a suggestion, or an offer or request to buy or sell any securities. The information shown is based on supplied data and should not be the only reason for any investment choice. Investing has risk, including the possible loss of the original amount invested. Always do your own research and talk with a registered financial advisor before making any investment choices.