For investors looking to balance the search for growth with fiscal care, the Growth At a Reasonable Price (GARP) or "affordable growth" method offers a practical middle path. This method tries to find companies with strong and lasting growth paths, but whose shares are not valued at extreme levels that allow little margin for error. It looks for businesses that are not only getting larger but are doing so with good profitability and financial soundness, indicating the growth is of higher quality and less risky. One stock that recently appeared from this type of filter is Globus Medical Inc , A (NYSE:GMED).

The company, a maker of musculoskeletal solutions such as implants and surgical tools for spine and orthopedic care, shows a fundamental picture that fits several main ideas of the affordable growth view.

A Base of Strong Growth

The central attraction of any growth investment is, expectedly, its growth picture. Globus Medical shows solid expansion in important financial measures, receiving a Growth Rating of 7 out of 10 in its fundamental analysis report. This rating comes from notable past results and good future projections.

- Past Performance: In the last year, the company increased its Earnings Per Share (EPS) by 22.76% and its Revenue by 11.75%. More significantly, the longer-term pattern is stronger, with Revenue increasing at an average yearly rate above 26% in recent years.

- Future Projections: Analysts think this progress will carry on, though at a slower speed. EPS is projected to grow at an average of 10.62% per year, while Revenue growth is estimated at 8.32%. This expected slowdown is something for investors to watch, but the forecasted rates still show good, above-average expansion.

For the affordable growth investor, this steady history and positive forecast are necessary. It points to a company that is effectively gaining market position and increasing its operations, which is the main driver for possible future stock gains.

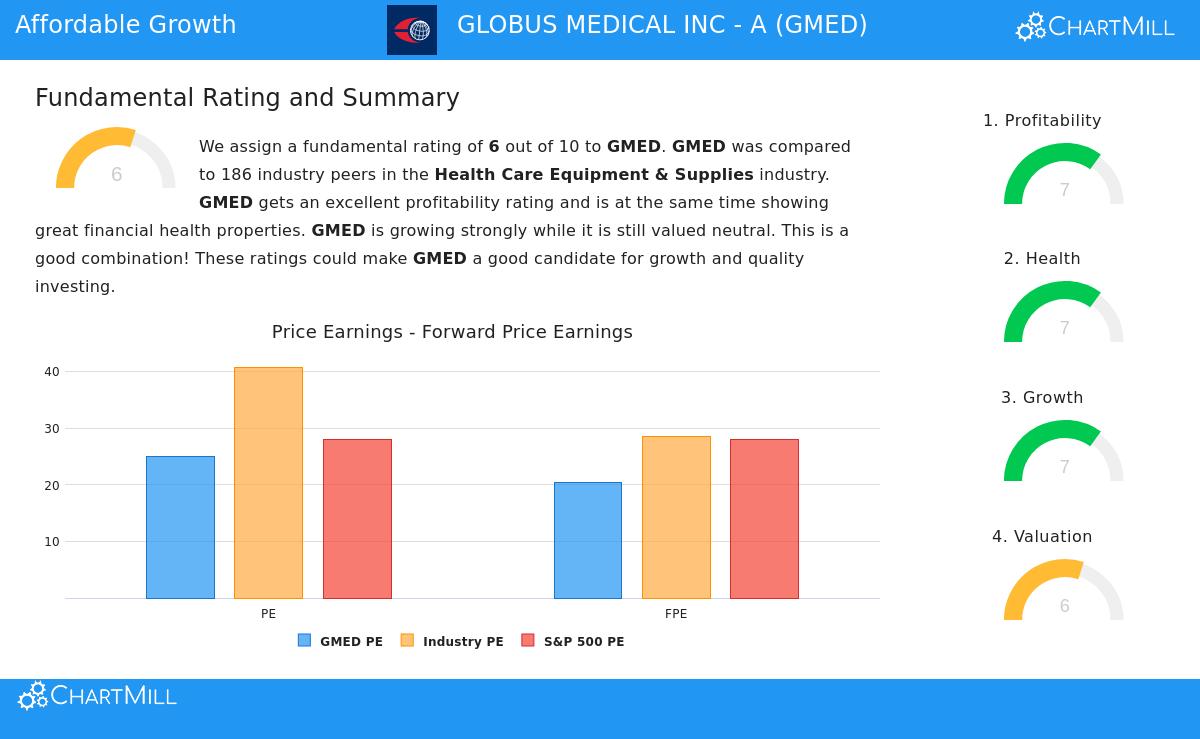

Valuation in Perspective

A stock can show excellent growth but still be a bad investment if bought at a too high price. This is where the "reasonable price" part of the method is vital. Globus Medical gets a Valuation Rating of 6, indicating its current share price is not an obvious discount but also not far from its fundamentals, particularly when compared to its industry.

- Mixed Signs on P/E: The company's standard Price-to-Earnings (P/E) ratio of 24.92 is higher than the industry average. However, its forward P/E ratio of 20.40 is more appealing, trading lower than both the wider S&P 500 average and most of its peers in the Health Care Equipment sector.

- Attractive Cash Flow & EBITDA Valuation: More attractive are other valuation measures. The stock is priced lower than about 90% of its industry based on its Price-to-Free-Cash-Flow ratio and lower than 82% based on its Enterprise Value-to-EBITDA ratio. This suggests the market may be pricing the company's cash-producing capacity too low.

This detailed valuation view is exactly what affordable growth filters aim to find: a company whose growth potential is not completely priced into a very high earnings multiple, especially when using forward-looking or cash-flow-based measures.

Supporting Fundamentals: Profitability and Health

Lasting growth cannot happen alone; it needs a profitable business model and a strong balance sheet. Globus Medical receives a 7 for both Profitability and Financial Health, giving important support for its growth story.

- Profitability Strength: The company has very good margins, with a Profit Margin of 15.30% and an Operating Margin of 17.37%, doing better than most of its rivals. Its Return on Assets and Return on Equity are also near the top in its industry. While these margins have faced some recent reduction—a detail noted in the report—they stay at good levels, showing the company's ability to set prices and run efficiently.

- Outstanding Financial Health: The balance sheet is a specific strength. Globus Medical has no debt, leading to top scores for Debt-to-Equity and Debt-to-Free-Cash-Flow ratios. This lack of debt, along with a strong Current Ratio of 4.13, gives great financial room to pay for future growth projects, handle economic slowdowns, or seek strategic purchases without the weight of interest costs.

For an investor, these high ratings in health and profitability lower the risk linked to the growth narrative. They show that the company's expansion is built on a base of financial control and high-quality earnings, making the growth more stable and less dependent on outside funding.

Conclusion

Globus Medical presents an example of the affordable growth filter reasoning. It is a company showing clear and significant growth in a focused medical market, yet its valuation—particularly on forward-looking and cash-flow bases—does not seem high compared to its peers. This growth is further supported by strong core profitability and a very firm, debt-free balance sheet. While investors should always think about items like the slowing growth rate and industry-specific challenges, the fundamental ratings indicate GMED has the main traits sought by methods looking for growth at a reasonable price.

This review of Globus Medical came from a specific filter for affordable growth stocks. Investors wanting to find other companies that fit similar standards of strong growth, fair valuation, and good fundamentals can examine the filter more via this link: View More Affordable Growth Stock Ideas.

Disclaimer: This article is for informational purposes only and does not constitute financial advice, a recommendation, or an offer to buy or sell any security. Investors should conduct their own research and consider their individual financial circumstances and risk tolerance before making any investment decisions.