In the search for long-term investment opportunities, many investors turn to the principles of legendary fund manager Peter Lynch. His strategy, famously outlined in One Up on Wall Street, focuses on finding growing companies with sound financials that are trading at reasonable prices, a philosophy often described as Growth at a Reasonable Price (GARP). Lynch supported a disciplined, fundamental method, preferring businesses with sustainable earnings growth, strong profitability, manageable debt, and healthy liquidity. By using a systematic filter based on these core ideas, investors can create a shortlist of companies for more study. One company that recently appeared through this view is EXLService Holdings Inc (NASDAQ:EXLS).

A Profile in Operations and Analytics

EXLService Holdings Inc is a global operations management and analytics company, providing data-led, AI-driven, and digital solutions across key industries. Headquartered in New York, the company's services are divided into Insurance; Healthcare and Life Sciences; Banking, Capital Markets and Diversified Industries; and International Growth Markets. In short, EXLS helps its clients, which include major insurers, healthcare payers, and financial institutions, improve efficiency, reduce costs, and enhance decision-making through advanced analytics and business process management. This puts the firm in the competitive but necessary IT Services sector, where consistent performance and technological adjustment are important.

Meeting the Lynch Criteria

A Peter Lynch-inspired filter looks for companies that show a specific mix of growth, value, and financial soundness. EXLService Holdings seems to meet these numerical tests, which are made to find sustainable compounders.

- Sustainable Earnings Growth: Lynch looked for companies growing steadily, not suddenly, thinking overly high growth is hard to keep. The filter requires a 5-year earnings per share (EPS) growth rate between 15% and 30%. EXLS reports a 5-year EPS growth rate of 21.93%, well inside this target range, showing a good and consistent history of profit increase.

- Reasonable Valuation Relative to Growth: Maybe the central part of the GARP method is the Price/Earnings to Growth (PEG) ratio. Lynch preferred companies with a PEG ratio of 1 or less, indicating the stock price is fair relative to its earnings growth. EXLS has a PEG ratio (based on past 5-year growth) of 0.98, meaning the market may be pricing its shares in line with its established growth path.

- Strong Profitability: To confirm quality, the filter requires a high Return on Equity (ROE). ROE shows how well a company creates profits from shareholders' equity. EXLS has an ROE of 25.35%, much higher than the 15% minimum, which indicates efficient management and a strong market position.

- Solid Financial Health: Lynch stressed investing in companies with strong balance sheets to handle economic slowdowns. Two key filters deal with this:

- Debt/Equity Ratio: A ratio below 0.6 is required, with Lynch himself favoring levels under 0.25. EXLS reports a Debt/Equity ratio of 0.37, showing a careful capital structure with little use of debt financing.

- Current Ratio: This measures short-term liquidity, with a score above 1 being necessary. EXLS has a strong Current Ratio of 2.91, showing clear ability to meet its near-term responsibilities.

Fundamental Health Check

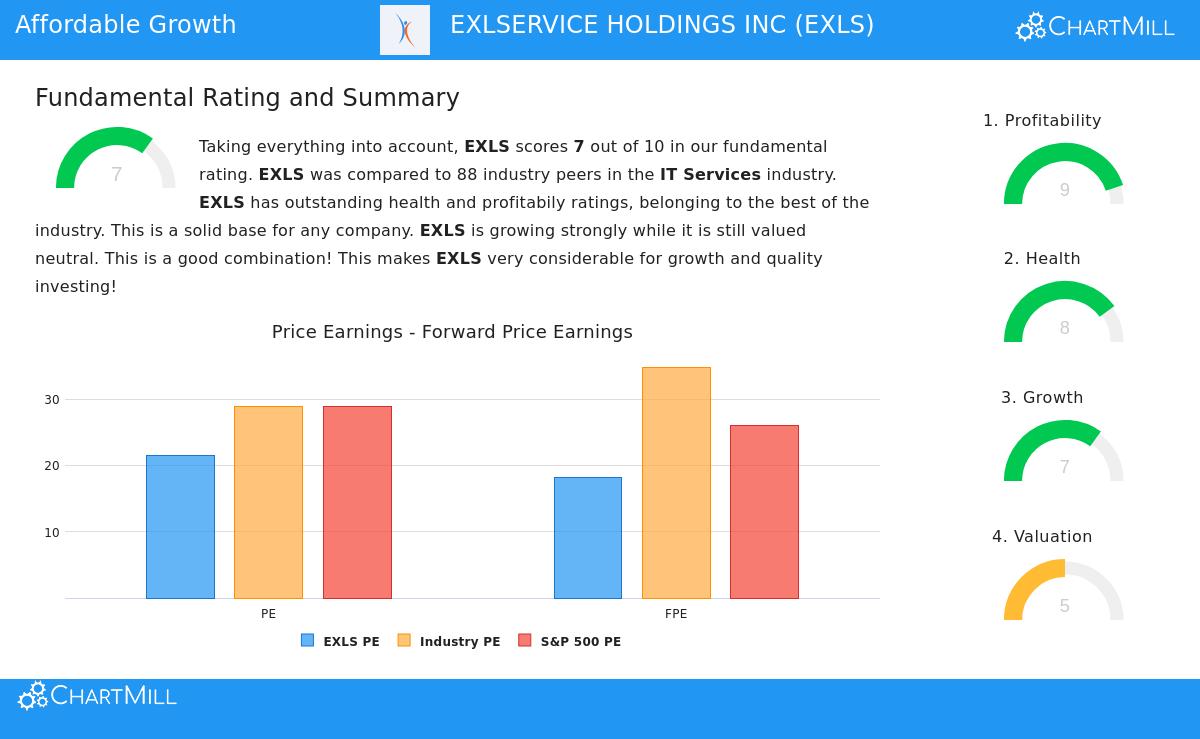

Beyond the specific filter settings, a wider look at EXLS's fundamental picture supports its position. According to ChartMill's detailed fundamental analysis report, EXLS gets an overall rating of 7 out of 10, comparing well within its industry.

The company's advantages are especially clear in two areas:

- Profitability & Health: EXLS gets very good scores for both profitability and financial health. Its margins are increasing, and it does better than most peers on important measures like Return on Assets (13.93%) and Return on Invested Capital (16.51%). The health score is supported by high liquidity and a very strong Altman-Z score of 8.28, which points to a very small chance of financial trouble.

- Growth & Valuation: The company is classified as "growing strongly" while keeping a "valued neutral" position. Its revenue growth has been steady, and future estimates point to continued, though slightly slower, increase. The valuation score is mixed; while its P/E ratio of 21.42 may seem high alone, it is actually lower than the industry average and the wider S&P 500. When growth is considered via the PEG ratio, the valuation seems more fair.

Is EXLS a Lynch-Style Opportunity?

For investors following the GARP philosophy, EXLService Holdings offers a strong example. It passes a strict, rules-based filter modeled on Peter Lynch's strategy by showing a history of sustainable earnings growth, trading at a price that accounts for that growth, and keeping a very firm balance sheet with high profitability. The company's main business, helping traditional industries change with digital tools, is likely a "simple" but necessary service, another detail Lynch might like.

It is important to note that a filter is only a first step. Lynch's strategy strongly focused on knowing the business you invest in. Potential investors should study EXLS's competitive environment, management performance, and the long-term need for its analytics and operations services.

Interested in seeing other companies that fit this disciplined growth-at-a-price method? You can see the current results of the Peter Lynch strategy filter here.

Disclaimer: This article is for informational purposes only and does not constitute financial advice, a recommendation, or an offer to buy or sell any securities. Investors should conduct their own due diligence and consult with a qualified financial advisor before making any investment decisions.