The investment philosophy of Peter Lynch, the legendary manager of Fidelity's Magellan Fund, focuses on finding well-run, growing companies trading at reasonable prices, a concept often called Growth at a Reasonable Price (GARP). His strategy, detailed in One Up on Wall Street, stresses sustainable earnings growth, strong financial health, and a valuation that does not overpay for that growth. It is a disciplined, long-term method that avoids speculative bubbles by concentrating on companies with understandable business models and solid foundations. A stock screener following Lynch's ideas can help find candidates that meet these strict criteria, one of which is ExlService Holdings Inc (NASDAQ:EXLS).

A Business Built for Sustainable Growth

ExlService Holdings operates in the IT services sector, providing data analytics, digital operations, and business process management. Its services span insurance, healthcare, banking, and capital markets, industries with persistent demand for efficiency and data-driven insights. This places the company in what Lynch might call a "dull" but essential area, where a company can grow steadily by performing well in a necessary field. The business model is understandable: it helps clients reduce costs and improve decision-making through technology and analytics, creating a recurring revenue stream that can support measured, long-term expansion.

Meeting the Lynch Criteria

A Peter Lynch-style screen looks for companies showing a specific mix of growth, profitability, and financial care. ExlService Holdings matches these core filters:

- Sustainable Earnings Growth: Lynch preferred companies growing earnings per share (EPS) between 15% and 30% each year, fast enough to be interesting, but slow enough to be maintainable. EXLS's five-year EPS growth rate of 21.9% sits comfortably within this target range, indicating a history of strong yet controlled expansion.

- Reasonable Valuation via PEG Ratio: The Price/Earnings to Growth (PEG) ratio is a key part of the Lynch method, as it frames a stock's valuation next to its growth. A PEG ratio at or below 1.0 suggests the market may not be overpaying for future growth. EXLS's PEG ratio, based on its past five-year growth, is 0.99, pointing to a good valuation when growth is considered.

- Strong Profitability (ROE): Return on Equity (ROE) measures how well a company creates profits from shareholder equity. Lynch looked for high ROE as a sign of a lasting competitive edge. EXLS's ROE of 25.4% is very good, far above the 15% minimum often used in screens and pointing to very effective management.

- Solid Financial Health: Lynch required companies with strong balance sheets to endure economic downturns.

- The Debt-to-Equity ratio of 0.37 is well under the screen's limit of 0.6 (and even Lynch's stricter preference for below 0.25), showing little use of debt financing.

- The Current Ratio of 2.91 shows good liquidity, meaning the company can easily meet its short-term obligations, a key sign of financial strength.

Fundamental Analysis Overview

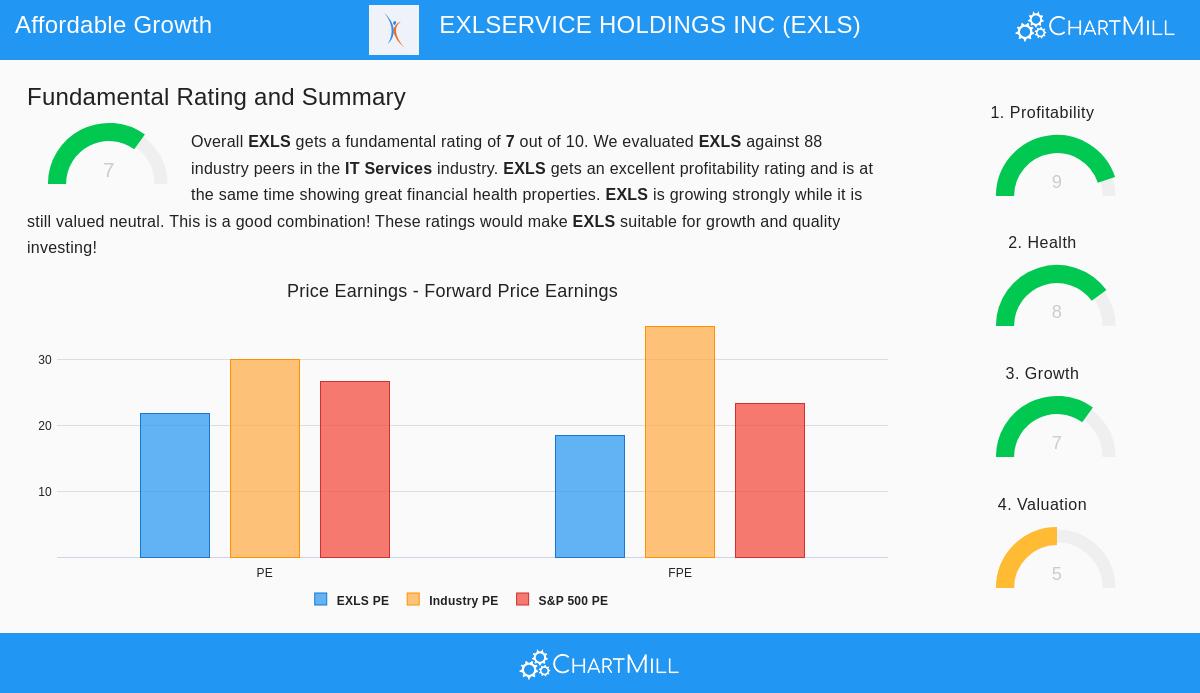

A detailed fundamental analysis of EXLS gives it a strong rating of 7 out of 10, noting its quality within the IT Services industry. The report emphasizes two main strengths:

- Exceptional Profitability and Health: The company scores a 9 for profitability, with excellent margins and returns on assets and invested capital. Its health score of 8 mirrors a strong balance sheet, high solvency, and good liquidity, all matching Lynch's focus on financial strength.

- Growth at a Reasonable Price: The analysis confirms the good historical growth in both revenue and EPS. While the valuation score is a moderate 5, noting the P/E ratio appears "rather expensive" alone, it states that the excellent profitability and expected future growth (approximately 15-16% each year) can support the valuation. This is the core of the GARP method: paying a fair price for superior, well-managed growth.

A Candidate for the Long-Term Investor

For an investor following Peter Lynch's ideas, ExlService Holdings makes a strong case. It is not a speculative story stock, but a financially sound company performing in a growing, necessary field. It has shown it can grow earnings at a maintainable double-digit rate, keeps a very strong balance sheet with little debt, and is priced at a level that accounts for its historical growth. While the basic P/E multiple may cause some concern, the complete view through the PEG ratio and the fundamental analysis implies the market is pricing its growth fairly.

The Lynch method needs patience; the idea is not about short-term market timing but about keeping quality companies through market cycles. With its steady performance and strong foundations, EXLS seems to be the kind of company that could build value for shareholders over many years.

Interested in finding other companies that fit this disciplined growth strategy? You can explore the full Peter Lynch Strategy stock screen here.

Disclaimer: This article is for informational purposes only and does not constitute financial advice, a recommendation, or an offer to buy or sell any security. Investing involves risk, including the potential loss of principal. You should conduct your own research and consult with a qualified financial advisor before making any investment decisions.