In the world of long-term investing, few strategies are as respected as the one made famous by Peter Lynch. The famous manager of the Fidelity Magellan Fund supported a methodical method centered on locating companies with good, lasting growth, sound financial condition, and fair prices. His thinking, often called "Growth at a Reasonable Price" (GARP), avoids speculative high-priced stocks and looks for businesses an investor can comprehend and own with assurance for years. A primary instrument for using this method is a stock screener that sorts for particular, Lynch-influenced measures, like steady earnings growth, a small debt amount, high earnings, and a good price when growth is considered.

One company that recently appeared from such a search is EOG Resources Inc (NYSE:EOG), a top exploration and production company in the oil and natural gas field. At first look, the energy business may appear cyclical and unstable, but a more detailed examination of EOG's basic qualities through Lynch's view shows a profile that matches well with the ideas of methodical, long-term growth investing.

Matching the Lynch Measures

The Peter Lynch search uses several strict filters to find companies with the correct mix of growth and price. EOG Resources seems to satisfy these primary checks, which are made to find businesses constructed for endurance instead of short-term speculation.

- Lasting Earnings Growth: Lynch preferred companies increasing earnings per share (EPS) between 15% and 30% each year over a five-year span, fast enough to be a frontrunner, but not so fast that it is unstable. EOG's five-year EPS growth rate of 18.45% rests securely within this goal range, showing a past of consistent, controlled increase.

- Good Price Compared to Growth: Maybe the central part of the GARP method is the PEG ratio (Price/Earnings to Growth), which Lynch stated should be at or under 1. This measure makes sure an investor is not paying too much for a company's growth path. With a PEG ratio of 0.56, EOG is trading at a notable markdown to its historical growth rate, a clear sign of value.

- Sound Financial Condition: Lynch was cautious of too much debt. The search demands a Debt-to-Equity ratio below 0.6, and Lynch himself liked it under 0.25. EOG's ratio of 0.25 shows a careful balance sheet, funded mainly by equity rather than debt, which offers strength during industry low periods.

- Firm Short-Term Cash Position: A Current Ratio above 1 guarantees a company can meet its immediate responsibilities. EOG's ratio of 1.62 shows more than enough cash availability, a simple but vital check for operational steadiness.

- High Earnings: A minimum Return on Equity (ROE) of 15% was Lynch's standard for effective use of shareholder money. EOG's ROE of 18.26% not only meets but goes beyond this level, showing the company produces firm profits from its equity foundation.

A Broad Basic Quality View

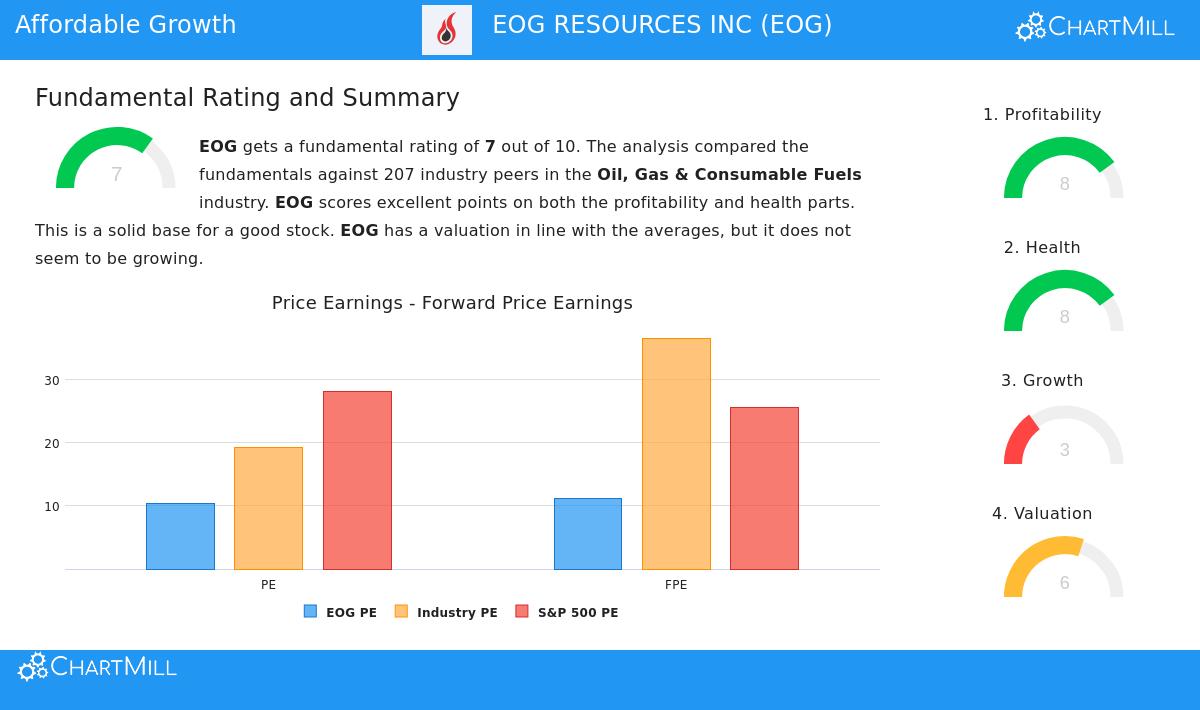

Beyond the particular search measures, a wider basic examination of EOG Resources supports its position as a basically sound company. According to ChartMill's full fundamental report, EOG gets an overall rating of 7 out of 10, with specific strong points in two Lynch-preferred areas: earnings and financial condition.

The company gets a strong earnings score of 8, having industry-best margins and returns. Its Profit Margin of 24.45% and Operating Margin of 33.18% do better than a large number of its competitors in the Oil, Gas & Consumable Fuels industry. This high level of operational effectiveness is precisely what long-term investors look for.

Also, EOG's financial condition score is a firm 8. The report notes its good ability to pay debts, shown by a healthy Altman-Z score and the same Debt-to-Equity ratio that satisfied the Lynch search. The company also has a past of building shareholder value through share repurchases, another detail Lynch saw as good. While the report mentions softer recent growth numbers, a typical difficulty in the commodity field, the company's price is considered fair, especially when matched against both industry averages and the wider S&P 500.

Final Point for the Long-Term Investor

For an investor following the Peter Lynch method, EOG Resources offers a strong case. It is not a speculative concept stock, but a settled participant in a needed industry, showing the "ordinary" but comprehensible business model Lynch frequently commended. The company joins a confirmed history of earnings growth with a price that does not require extreme future success. Its strong balance sheet and high earnings give a safety buffer and the possibility for lasting increase of capital over time.

While the energy field is naturally cyclical and deals with long-term change questions, EOG's controlled capital use, low-cost setup, and financial power place it to handle instability and possibly benefit patient shareholders. It shows the kind of company a GARP investor might study more: one growing at a fair and lasting speed, obtainable at a fair price.

Find Other Possible Investments This study of EOG Resources came from a systematic search based on Peter Lynch's ideas. If you want to study other companies that currently satisfy these methodical growth and price measures, you can see the full and current search results here.

Disclaimer: This article is for information only and does not form financial guidance, a suggestion, or an offer to buy or sell any security. Investing includes risk, including the possible loss of original money. You should do your own complete study and think about talking with a qualified financial advisor before making any investment choices.