For investors looking to balance the search for growth with a degree of caution, the "Growth at a Reasonable Price" (GARP) or "Affordable Growth" strategy offers a sensible middle path. This method tries to find companies that are not only increasing quickly but also have good basic operations, all while trading at prices that do not require extreme optimism. By filtering for stocks with high growth scores, acceptable profit and financial condition, and a price that is not too high, investors can search for chances where the market may not have completely recognized a company's path. One stock that recently appeared from this type of filtering process is DexCom Inc (NASDAQ:DXCM).

A Profile in Growth

Fundamentally, the affordable growth strategy requires solid and clear expansion, and DexCom meets this need. The company's growth measures are a notable characteristic, receiving a high ChartMill Growth Rating of 8 out of 10. This score is supported by strong past results and good future estimates.

- Revenue Growth: Over the last year, revenue rose by 14.21%, and the average yearly growth rate over recent years is a strong 22.27%. Analysts predict this trend to persist, with revenue forecast to grow at an average yearly rate of 13.47% in the next years.

- Earnings Growth: The profit growth is even more notable. Earnings Per Share (EPS) increased by 9.41% last year and has averaged a high 29.25% yearly growth in recent periods. For the future, EPS is estimated to rise by an average of 22.19% each year.

This steady, double-digit growth in both sales and profits is exactly what moves a successful growth investment. It shows a company that is effectively growing its activities and gaining market position in its field.

Valuation in Context

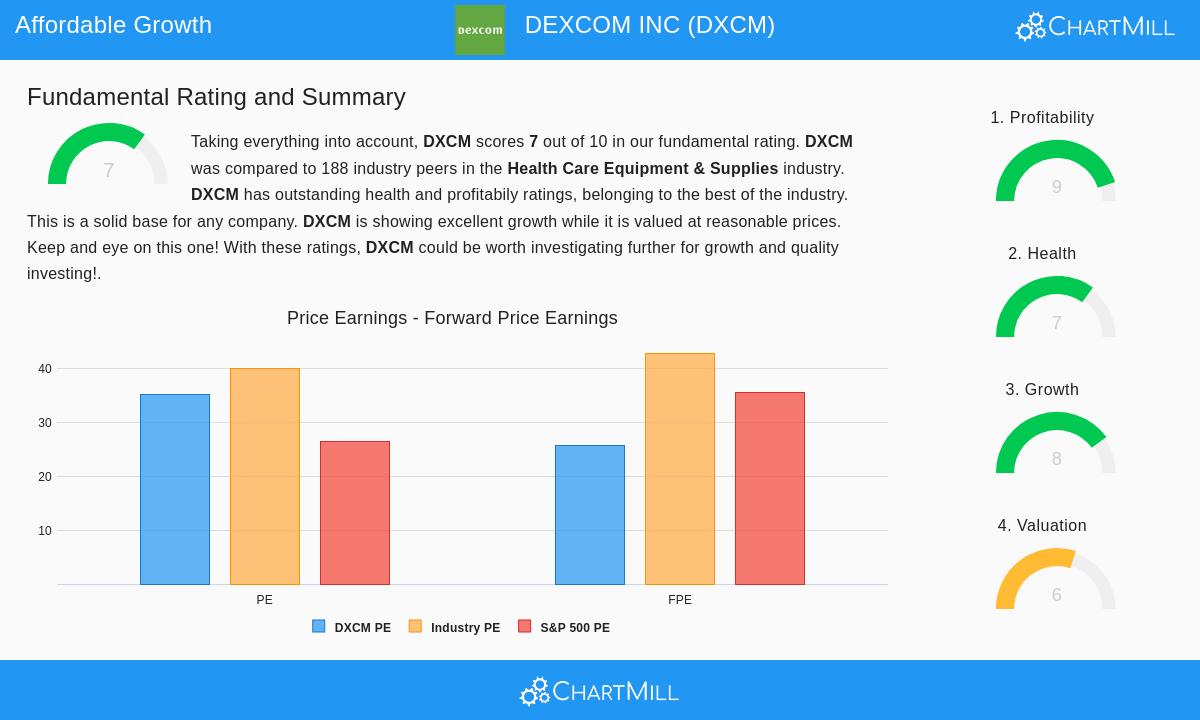

While growth is necessary, paying too high a price for it can reduce future gains. This is where the price evaluation becomes important. DexCom's ChartMill Valuation Rating is a 6 out of 10, which, within the framework of this strategy, implies it is not priced too high. A closer examination shows a detailed situation.

On the surface, common measures like a Price-to-Earnings (P/E) ratio of 35.08 and a Forward P/E of 25.70 might seem high compared to the wider S&P 500. However, price is relative. When compared to its competitors in the Health Care Equipment & Supplies industry, DexCom offers a more interesting situation:

- Its P/E ratio is lower than 71% of its industry competitors.

- Its Forward P/E ratio is lower than 73% of the industry.

- More significantly, its Price-to-Free-Cash-Flow and Enterprise Value-to-EBITDA ratios are lower than 85% and 75% of the industry, in that order.

Also, the company's excellent profit (covered next) and its high estimated earnings growth rate help support its current multiple. The PEG ratio, which includes growth, suggests a fair price. For a GARP investor, this mix, strong growth at a price that is sensible compared to its successful sector, is a main point of interest.

The Foundation: Profitability and Financial Health

Lasting growth cannot occur without a profitable operation and a firm financial position. DexCom performs well here, giving the basic support that makes its growth narrative more reliable. The company has a leading ChartMill Profitability Rating of 9.

- High Returns: The company produces very good returns on its capital, with a Return on Invested Capital (ROIC) of 15.72%, better than almost 96% of its industry. Its Return on Equity of 26.44% is also very high.

- Strong Margins: DexCom keeps solid margins, with a Profit Margin of 15.96% and an Operating Margin of 18.41%, both placed in the top tier of its industry. These margins have gotten better in recent years.

Financial condition, with a rating of 7, is another supporting element. While its immediate cash ratios (Current and Quick Ratio) are only acceptable, its overall stability is firm. The company has a good Debt-to-Equity ratio of 0.47 and an Altman-Z score of 4.87, showing low short-term failure risk. Notably, its Return on Invested Capital is clearly higher than its cost of capital, meaning it is producing real value for shareholders with each dollar used.

Conclusion and Further Research

DexCom Inc shows an example of the kind of profile sought by affordable growth filters. It combines active, double-digit growth in sales and profits with sector-leading profit and a financially stable business. While its total P/E may cause some hesitation, its price is distinctly sensible, and in some instances low, relative to its high-growth industry group. This combination of firm growth, basic strength, and a not-too-high price is the central idea of the GARP strategy.

It is notable that the company does not offer a dividend, which may not appeal to investors seeking income, but this is common for businesses putting money back into operations to support growth. The full basic analysis that supports this perspective can be examined on ChartMill's DexCom Fundamental Analysis Report.

For investors curious about finding other companies that match this careful growth outline, the filtering rules that found DexCom can be a beginning for more investigation. You can examine more possible "Affordable Growth" choices by using the predefined screen on ChartMill.

Disclaimer: This article is for information only and does not form financial guidance, a suggestion to buy or sell any security, or a support of any investment plan. Investors should perform their own study and think about their personal financial situation and risk appetite before making any investment choices.