For investors aiming to balance the search for growth with prudence, the "Growth at a Reasonable Price" (GARP) strategy offers a practical middle ground. This method finds companies increasing their earnings and revenue at an above-average pace, but whose shares are not priced too high. The aim is to sidestep the speculation that can surround high performers while still gaining from solid business development. One way to find these chances is to use fundamental ratings that assess a stock on five main points: Growth, Valuation, Health, Profitability, and Dividend. A stock with high growth marks and good scores in profitability and financial condition, while not seen as too expensive, can be a strong fit for this strategy.

Dynatrace Inc. (NYSE:DT), a top firm in software intelligence and observability, recently appeared from such an "Affordable Growth" screen. The company's fundamental report shows a picture that fits the GARP idea well, receiving a total rating of 7 out of 10. This rating comes from clear advantages in several important areas, pointing to a business that is developing effectively and is on stable ground.

Growth: A Strong Engine

The central idea of any growth plan is, expectedly, growth. Dynatrace does very well here, getting a high Growth rating of 8. The company has shown a strong history of development, which is a key sign of market need and operational skill.

- Past Results: Over the last year, revenue rose by 18.5%, while earnings per share (EPS) went up by 18.18%. More notably, the average yearly growth rates are higher, with revenue going up 25.49% and EPS jumping 35.19% over recent years.

- Future Predictions: Analysts expect this pace to keep going, with predicted average yearly growth of 14.93% for revenue and 17.43% for EPS. While this is a slowdown from the very high past rates, it is still a "quite good" view that means continued, above-market development.

This steady and solid growth path is just what GARP investors want to see—a business that is clearly getting bigger and gaining market position.

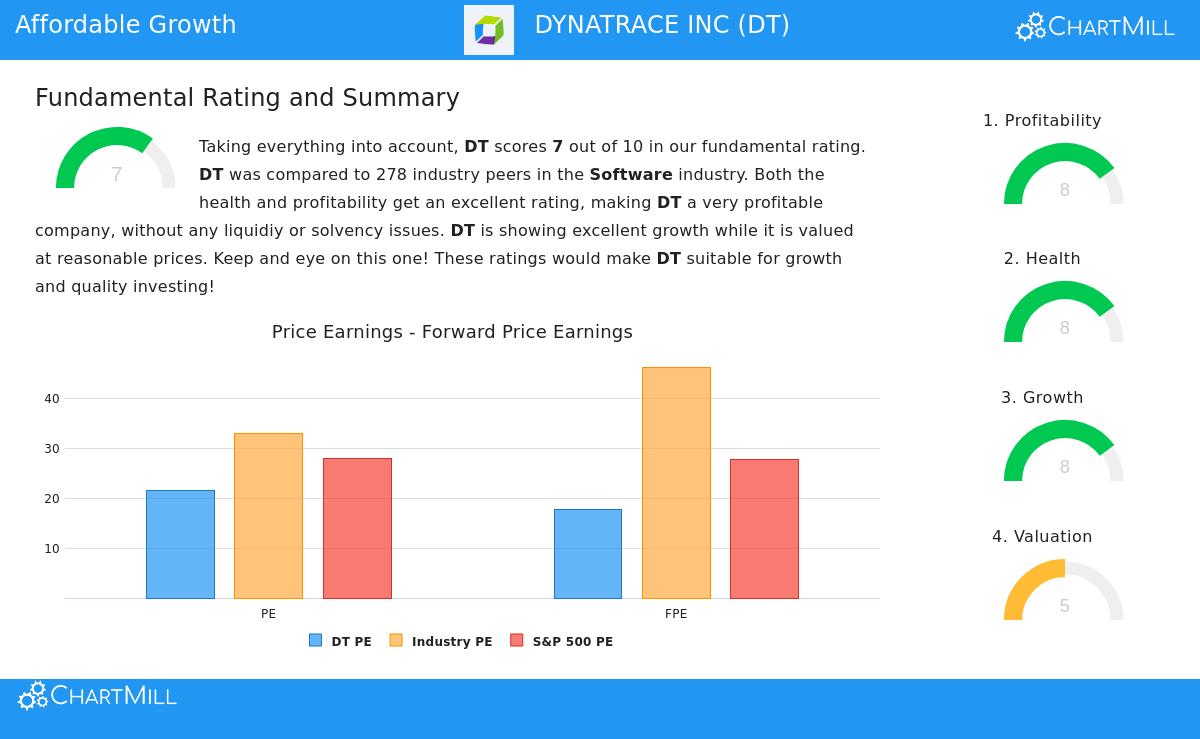

Valuation: Fair Given the Situation

A stock with excellent growth can still be a bad buy if the cost is too steep. The Valuation rating, then, works as an important test. Dynatrace's Valuation score of 5 shows it is not low-cost, but the review suggests it is fairly priced compared to its quality and growth outlook.

- Industry Comparison: With a Price-to-Earnings (P/E) ratio of 21.61 and a Forward P/E of 17.71, Dynatrace is valued lower than most of its software industry competitors. This matters given the industry's frequently high valuations.

- Market Comparison: Both the current and forward P/E ratios are also under the current averages for the S&P 500, giving a good comparison to the wider market.

- Growth Consideration: The PEG ratio, which changes the P/E for predicted earnings growth, shows a "fair valuation." The report states that Dynatrace's exceptional profitability and expected growth could support its current valuation level.

For the GARP strategy, this is the needed balance: paying a fair, not extreme, price for a company with better growth traits.

Profitability & Health: The Supporting Base

Lasting growth needs a profitable business model and a sound balance sheet. Dynatrace gets an 8 on both Profitability and Financial Health, giving trust in the staying power of its growth narrative.

- Profitability Power: The company has very good margins, with a Gross Margin over 81% and a Profit Margin of 27.33%, putting it in the best group of its industry. Its Return on Equity (18.22%) and Return on Assets (12.40%) are also high numbers, showing good use of investor money.

- Financial Strength: Most importantly, Dynatrace has no debt. This clean balance sheet gives great flexibility and lowers risk, particularly in shaky economic times. Its Altman-Z score of 5.62 also shows very small near-term bankruptcy risk.

These high marks in Profitability and Health are not just extra facts; they are central to the "affordable growth" argument. They show that the company's growth is high-quality—coming from a profitable business model and not from high borrowing or financial tactics. This lowers investment risk and backs the view that the company can keep financing its own development.

Conclusion

Dynatrace offers a strong example for the Growth at a Reasonable Price method. It joins a solid, clear growth history with a valuation that seems acceptable—not speculative—when considered next to its industry, the wider market, and its future earnings possibility. Importantly, this growth is supported by first-rate profitability and a very firm, debt-free balance sheet. This mix of elements points to a company that is not only getting bigger but doing so from a place of financial soundness and operational effectiveness.

For investors wanting to look at other stocks that match this description, you can use the same "Affordable Growth" screen with our stock screener tool. A full look at Dynatrace's fundamental numbers is in its complete fundamental analysis report.

Disclaimer: This article is for information only and is not financial advice, a suggestion, or an offer or request to buy or sell any securities. The information given is based on supplied data and should not be the only reason for any investment choice. Investing has risk, including the possible loss of the original amount. Always do your own research and think about talking with a qualified financial advisor before making any investment choices.