Investors looking for long-term growth opportunities at reasonable prices often use established methods like the Peter Lynch investment strategy. This method, described in Lynch's book One Up on Wall Street, centers on finding companies with lasting earnings growth, good financial condition, and fair valuations. The strategy prioritizes fundamental analysis instead of market timing, looking for businesses that show steady profitability without high debt. Lynch famously delivered outstanding returns by investing in companies he understood that had predictable growth, making his framework especially useful for investors aiming for growth at a reasonable price (GARP).

Company Overview

DRDGOLD LTD-SPONSORED ADR (NYSE:DRD) functions in the gold mining industry via surface retreatment activities in South Africa. The company focuses on obtaining gold from old tailings deposits, mainly through its Ergo and Far West Gold Recoveries sites. This operational model includes processing former slime dams and sand dumps from past mining work, representing a specific part of the wider mining field that merges resource recovery with environmental cleanup.

Growth Metrics

The company shows notable growth features that fit with Lynch's focus on lasting expansion:

- 5-year EPS growth rate of 26.15%, well inside Lynch's favored 15-30% span

- Most recent year EPS growth of 141.66%, showing increasing profitability

- Revenue growth of 13.49% per year over recent years, with projections rising to 16.38% future growth

Lynch specifically looked for companies expanding between 15-30% each year, thinking this span indicates manageable growth without the instability of very high-growth firms. DRDGOLD's steady results within this range point to controlled, expected growth that can be continued over long periods.

Valuation Assessment

DRDGOLD shows interesting valuation measures that satisfy Lynch's strict standards:

- PEG ratio of 0.53, much lower than Lynch's highest limit of 1.0

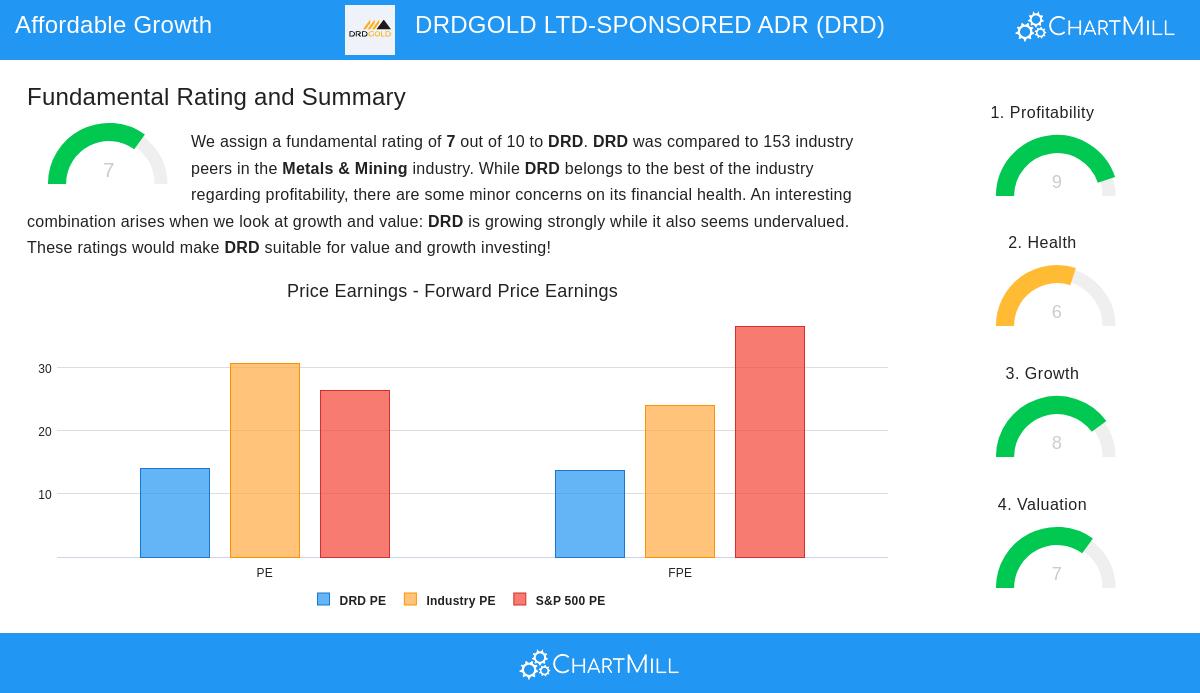

- P/E ratio of 13.97, showing a lower price compared to both industry and S&P 500 averages

- Price/Forward Earnings of 13.75, showing continued fair valuation outlooks

The PEG ratio was especially significant to Lynch because it adjusts the P/E ratio for growth, giving a fuller view of valuation. A ratio under 1.0 indicates the market might be pricing the company's growth potential too low, creating a possible opening for long-term investors.

Financial Health and Profitability

The company displays good financial traits that Lynch thought necessary for long-term investments:

- Debt/Equity ratio of 0.001, much lower than Lynch's preferred maximum of 0.6

- Current Ratio of 2.28, showing good short-term cash availability

- Return on Equity of 36.17%, greatly surpassing the 15% minimum Lynch wanted

- Operating Margin of 35.35% and Profit Margin of 27.51%, both placed in the top group of industry competitors

Lynch stressed careful financial management, favoring companies with very little debt and good cash situations. The almost non-existent debt combined with good profitability measures forms a financial condition that matches his cautious method for growth investing.

Fundamental Analysis Summary

According to the detailed fundamental analysis, DRDGOLD gets an overall score of 7 out of 10, with especially high marks in profitability (9/10) and growth (8/10). The analysis points out the company's excellent return measures, including ROE of 36.17% and ROIC of 26.85%, both placed in the top levels of industry competitors. While the dividend part scores average at 4/10 because of reducing but maintainable payments, the valuation score of 7/10 shows the company's appealing price relative to its growth outlook and profitability.

Investment Considerations

For investors using the GARP method through Lynch's strategy, DRDGOLD offers an interesting example of a company working in a conventional field while showing current efficiency and profitability. The surface retreatment operational model provides possible benefits in cost predictability and environmental adherence compared to standard mining. However, investors should think about the company's connection to gold price changes and geographic focus in South Africa when assessing long-term possibilities.

The company's mix of good growth, high profitability, careful financial setup, and fair valuation creates a profile that deserves notice from investors looking for Lynch-style openings. The match across several Lynch criteria indicates the possibility for continued long-term results, though ongoing observation of operational performance and market factors stays important.

Disclaimer: This analysis is for informational purposes only and does not constitute investment advice, recommendation, or endorsement of any security. Investors should conduct their own research and consult with financial advisors before making investment decisions. Past performance does not guarantee future results, and all investments carry risk including potential loss of principal.