For investors aiming to create a portfolio centered on dependable income, a disciplined screening method is necessary. One useful technique includes looking for companies that provide a good dividend now and also have the basic financial soundness to maintain and possibly increase those payments in the future. This approach values quality and long-term viability over seeking the absolute highest yield, which can sometimes indicate company problems. A functional tactic is to employ a screener that finds stocks with good marks for dividend quality, along with good marks for earnings and balance sheet soundness. This pairing helps find companies where the dividend is backed by good earnings and a strong balance sheet.

Amdocs Ltd. (NASDAQ:DOX), a worldwide supplier of software and services to communications and media companies, appears as a notable candidate from this type of screening. The company’s basic profile indicates it fits the main ideas of careful dividend investing, mixing income creation with business steadiness.

Dividend Quality and Long-Term Viability

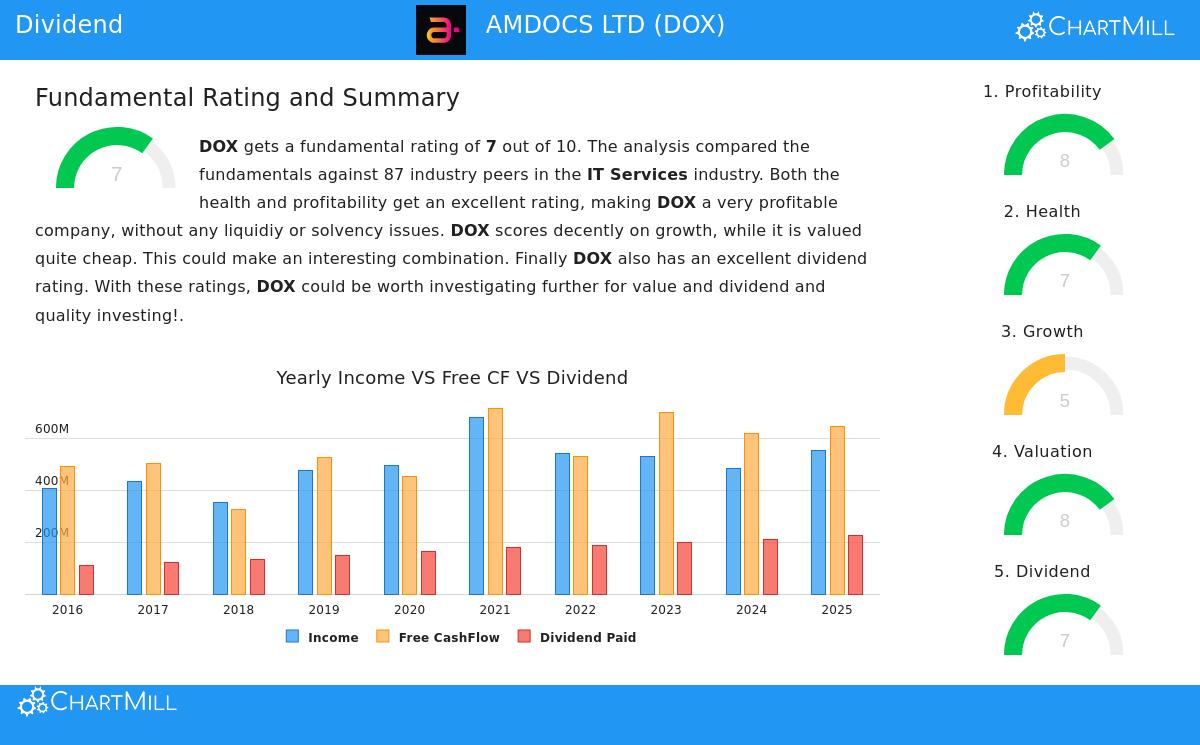

The main attraction for income investors is found in Amdocs’s dividend details, which receive a 7 out of 10 on the ChartMill Dividend Rating. This rating combines important measures into one, summary score.

- Yield and Growth: The company provides a forward dividend yield near 2.87%, which is good compared to both the S&P 500 average (near 1.81%) and the wider IT Services field. Significantly, this income has a past of dependable growth. Amdocs has raised its dividend for at least ten straight years, with a notable average growth rate above 10% during that time. This history of regular increases is a key trait of dividend-centered companies.

- Payout Safety: A vital test for any dividend stock is the payout ratio, which shows the part of earnings given as dividends. Amdocs’s ratio is near 40.5%. While this is above what some cautious investors like, it mostly stays within a workable range, showing the company keeps over half of its earnings to put back into the business. This middle ground is key for the method, as a very high ratio could threaten future payments if earnings fall.

Supporting Basics: Earnings and Balance Sheet Soundness

A good dividend depends on the company behind it. The screening needs of acceptable earnings and soundness are important because they show the company’s ability to maintain its activities and pay shareholders without difficulty. Amdocs does well here, with an Earnings Rating of 8 and a Soundness Rating of 7.

- Earnings Strength: The company is regularly profitable, with good return figures. Its Return on Invested Capital (ROIC) of 13.77% and Profit Margin of 12.22% are some of the top in its field, doing better than most similar companies. This high level of earnings gives a solid base for the dividend, making sure it is paid from real earnings ability, not from borrowing or selling assets.

- Balance Sheet Soundness: From a debt perspective, Amdocs is in good condition. It has a workable amount of debt, with a Debt-to-Equity ratio of 0.19, and its Altman-Z score shows a low short-term chance of financial trouble. While its current and quick cash ratios are seen as lower than some field peers, the complete soundness rating indicates the company’s very good earnings and debt position lessen wider cash concerns. This financial steadiness is what the screening process looks for,a company that can easily meet its duties and pay shareholders through different market periods.

Price and Growth Setting

For investors buying shares, price is important. Amdocs seems fairly valued, with a Price-to-Earnings (P/E) ratio near 10.3 and a forward P/E near 9.0. These numbers show a notable discount compared to the wider market and are less expensive than most companies in its sector. This valuation gives some safety and improves the possible overall return, joining dividend income with the chance for share price growth.

Growth is steady but not high. While recent sales have been flat to a little lower, earnings per share are projected to grow at a near-10% yearly rate in the next few years, which matches its past dividend growth rate. This match between earnings growth and dividend growth is a good signal for the viability of future raises.

A Candidate for More Study

Based on a systematic screen for good dividend payers, Amdocs Ltd. makes a good argument for income-focused investors. It joins an attractive and increasing yield with the basic support of high earnings and firm balance sheet soundness. The stock’s fair price adds to its attraction. As with all investments, this review is a first step. A full study of the company’s business plan, competitive place, and field direction is advised.

You can examine the detailed basic analysis that backs this review in the full ChartMill Fundamental Report for DOX.

For investors wanting to find other companies that fit similar standards of good dividends, earnings, and balance sheet soundness, the screening process that found Amdocs can be repeated and adjusted. You can find more possible candidates by examining the ready-made Best Dividend Stocks screen.

,

Disclaimer: This article is for information only and is not financial advice, a suggestion, or an offer or request to buy or sell any securities. The analysis uses data and ratings from ChartMill, which come from past and projected numbers. Investing has risk, including the chance of losing the original investment. You should do your own complete study and think about talking with a qualified financial advisor before making any investment choices.