For investors looking to balance the search for growth with a degree of caution, the "Growth at a Reasonable Price" or "Affordable Growth" strategy presents a viable middle path. This method seeks to find companies that are increasing their earnings and revenue at a good rate while also trading at prices that are not overly high. It avoids the extreme speculation linked to high-growth stocks and the pitfalls of inexpensive companies with no progress. By looking for stocks with good growth scores, sound profitability and financial strength, and a price that is not too high, investors can create a portfolio ready to gain from business improvement without paying too much for the chance.

A recent search for such "Affordable Growth" possibilities found Doximity Inc., Class A (NYSE:DOCS), a business that runs a digital network for healthcare workers in the United States. The company's basic profile, as shown in its detailed analysis report, seems to match the main ideas of this investment approach.

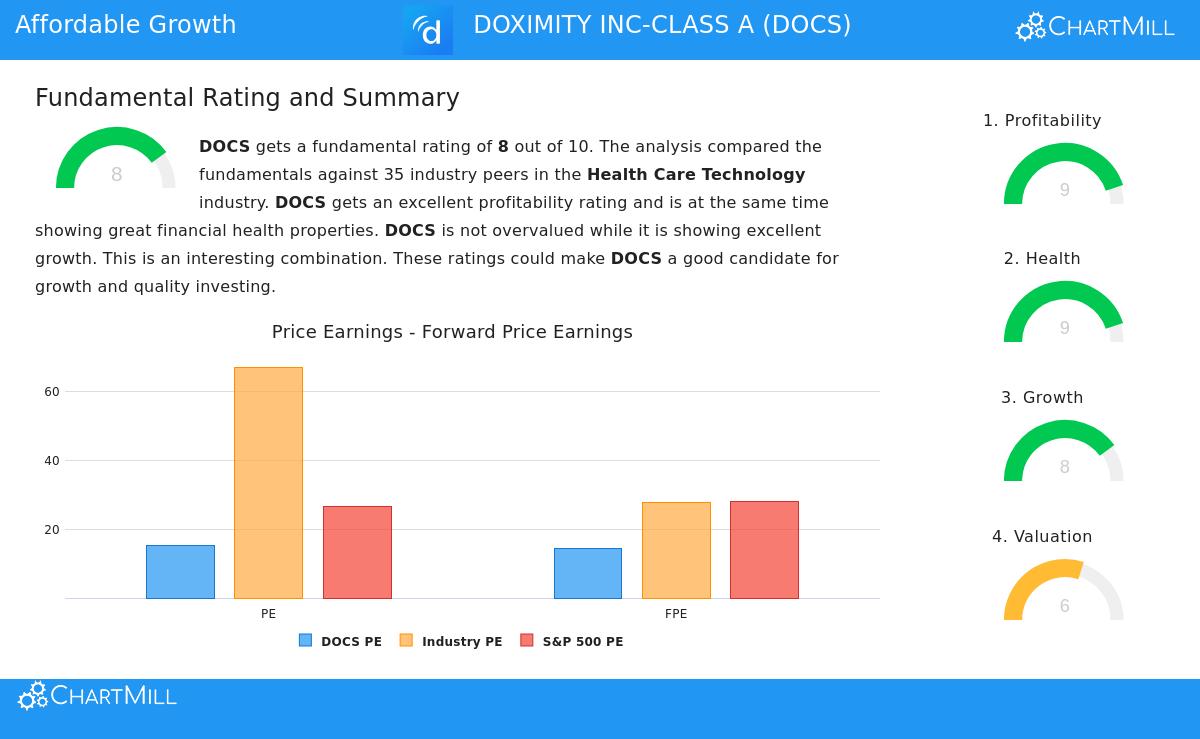

A Base of High Profitability and Strength

Before examining growth and price, it is important to evaluate the company's operational and financial base. Doximity performs very well here, receiving top ChartMill scores of 9 out of 10 for both Profitability and Financial Health. This solid foundation is key for the Affordable Growth strategy, as it implies the company's growth is lasting and supported by a stable operational center, not accounting tricks or high risk.

- Profitability Power: Doximity's profit margins are very high in the Health Care Technology field. It has a Profit Margin of 37.5% and an Operating Margin of 37.4%, doing better than 100% of its industry competitors. Its returns on capital are also notable, with a Return on Invested Capital (ROIC) of 19.5% that is much higher than its cost of capital, showing it is building real value for shareholders.

- Very Strong Financial Health: The company has no debt, giving it great financial options and protection from higher interest rates. This leads to a high Altman-Z score of 17.7 and very good liquidity measures, with a Current Ratio and Quick Ratio both at 6.6. This financial strength means the company can pay for its growth plans from its own resources and handle economic shifts without difficulty.

Strong Growth Path

The "growth" part of the Affordable Growth search is clearly satisfied, with Doximity getting a Growth score of 8. The company has shown it can increase both its revenue and earnings at a good speed.

- Previous Results: Over the last year, Revenue increased by 15.9% while Earnings Per Share rose by 28.9%. The longer-term patterns are more pronounced, with a 5-year average yearly EPS growth rate of 79.2% and Revenue growth of 37.4%.

- Future Outlook: While analyst forecasts naturally expect a slowdown from these very high past rates, the forward view is still positive. Projections suggest average yearly EPS growth of 11.8% and Revenue growth of 11.8% in the next few years, which still counts as quite good and offers a plausible path for further improvement.

Price at a Sensible Level

This is where the "affordable" or "reasonable price" element becomes relevant. Doximity receives a Valuation score of 6, which shows it is not low-priced in a simple way but seems fairly priced, particularly when considered next to its quality and growth picture. The price measures indicate the market is not assuming past very high growth will continue forever, possibly giving a buying point for GARP investors.

- Good Relative Price: Compared to its own industry, Doximity seems lower-priced on several important measures. Its Price/Earnings (P/E) ratio of 15.2 is lower than 83% of its Health Care Technology peers. In the same way, its Price/Forward Earnings ratio of 14.3 and Enterprise Value/EBITDA ratio are more appealing than most of the industry.

- Market and Growth Setting: The stock also trades below the wider S&P 500 index on both past and future P/E bases. Significantly, its PEG ratio, which modifies the P/E for expected growth, is seen as showing a "fair price." When paired with its high profitability, the current price multiple can be viewed as acceptable, if not a good chance, for a company of this quality.

Summary

Doximity offers a strong example for the Affordable Growth investment method. It is not a very low-price stock or a speculative, no-profit growth prospect. Instead, it fits the tactical middle area: a company with a demonstrated, profitable operation, a very strong balance sheet, a record of good growth, and a future supported by positive growth forecasts, all available at a price that seems fair within its industry and the general market. For investors systematically looking for quality growth that is not too expensive, stocks that fit these combined standards deserve more attention.

This review of Doximity came from a particular Affordable Growth search. Investors wanting to find other stocks that currently meet similar filters for good growth, sound basics, and fair price can use this search themselves for more outcomes.

Disclaimer: This article is for information only and is not financial advice, a suggestion to buy or sell any security, or a support of any investment plan. Investors should do their own study and think about their personal financial situation and risk comfort before making any investment choices.