The investment philosophy of legendary fund manager Peter Lynch, as detailed in his book One Up on Wall Street, focuses on finding companies with strong, lasting growth that are trading at sensible prices. Often called a "Growth at a Reasonable Price" (GARP) method, Lynch's strategy does not pursue the fastest-growing, most speculative names. Instead, it looks for profitable, financially sound businesses whose earnings growth is both notable and can be maintained over many years. This approach uses a group of specific fundamental filters to find such opportunities, concentrating on earnings growth, valuation, profitability, and balance sheet condition.

A Lynch-Style Candidate in the Tanker Trade

One company that recently appeared using a filter based on Lynch's standards is DHT Holdings Inc (NYSE:DHT), an owner and operator of a fleet of Very Large Crude Carriers (VLCCs). Initially, a crude oil shipping company may appear an improbable candidate for a growth-focused method. However, Lynch supported investing in comprehensible businesses, even those in more cyclical or "ordinary" fields, if they show the correct financial traits. The fundamental data for DHT indicates it deserves more examination from investors looking for long-term, sensibly-priced growth.

Meeting the Lynch Criteria

The central filters of a Peter Lynch screen are made to identify companies with a particular financial profile. DHT's current measurements align closely with these needs:

- Lasting Earnings Growth: Lynch preferred a 5-year earnings per share (EPS) growth rate between 15% and 30%, thinking growth outside this band was either too low or could not last. DHT's 5-year average EPS growth of 16.14% sits within this target area, showing a record of firm, consistent profit increase.

- Sensible Valuation (PEG Ratio): Possibly the most important Lynch measurement is the Price/Earnings to Growth (PEG) ratio, which tries to price a stock in relation to its growth rate. Lynch wanted a PEG of 1.0 or lower. DHT's PEG ratio, based on its past five-year growth, is 0.90, suggesting the market might be pricing its historical growth path too low.

- Firm Profitability (ROE): A high Return on Equity (ROE) shows management's skill in creating profits from shareholder money. Lynch's screen usually asks for an ROE above 15%. DHT's ROE of 18.25% clearly passes this level, indicating firm profitability in its industry.

- Financial Condition (Debt & Liquidity): Lynch was cautious about high debt. His method often uses a Debt/Equity ratio below 0.6, with a liking for even smaller amounts. DHT's Debt/Equity ratio of 0.22 shows a careful capital structure funded mainly by equity. Also, its Current Ratio of 2.41 displays sufficient liquidity to meet near-term debts, passing another key Lynch condition check.

Fundamental Condition and Valuation Summary

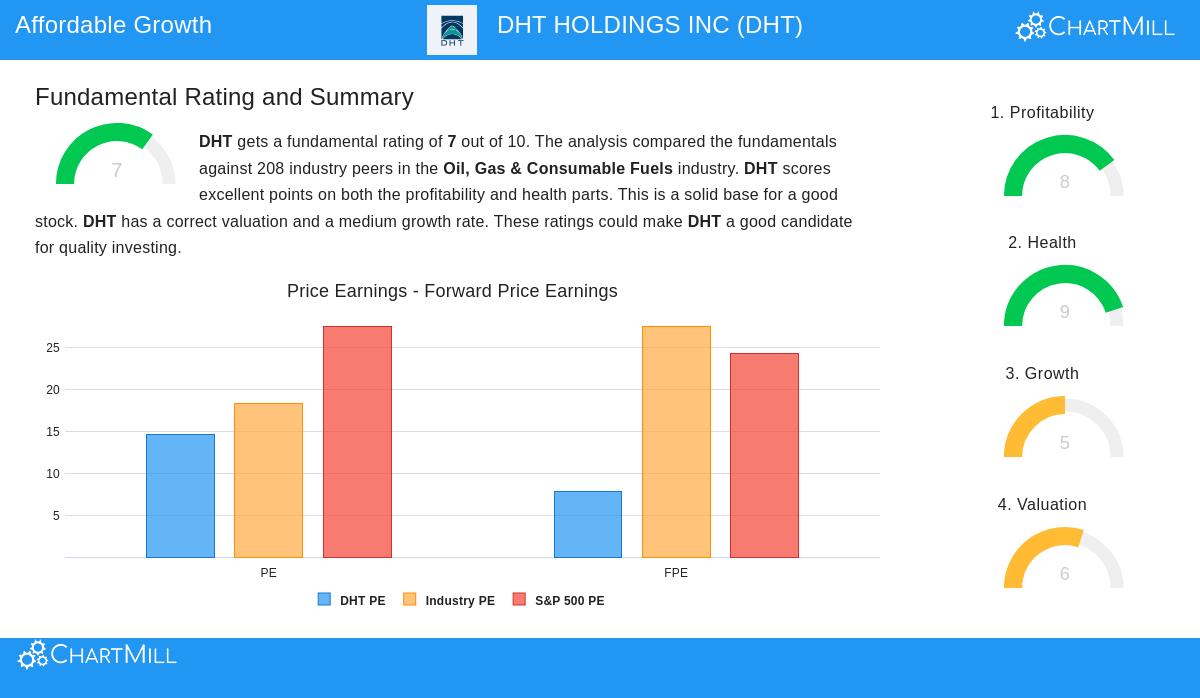

A wider view of DHT's fundamental analysis report on Chartmill supports the image shown by the Lynch screen. The company gets a firm overall fundamental score of 7 out of 10. Its notable features are very high scores in both Condition (9/10) and Profitability (8/10), verifying the strong balance sheet and firm margins shown by the Lynch filters. The company's profit margin of over 41% is one of the highest in its field.

On the valuation side, the report states DHT trades at a P/E ratio of 14.59, which is similar to its industry peers but clearly lower than the wider S&P 500. More interesting is its forward P/E ratio of 7.84, which is seen as "very low" compared to both industry and market norms. While past revenue and EPS have had some recent variation, typical in the cyclical shipping field, analyst predictions point to a new increase, with expected EPS growth of almost 15% each year. You can see the complete, thorough fundamental analysis for DHT Holdings Inc. here.

Points for the Long-Term Investor

For an investor using Peter Lynch's ideas, DHT offers an interesting case. It works in a physical, comprehensible business, global seaborne crude oil transport. Its financial numbers pass the quantitative checks for lasting growth, sensible price, and financial strength. The high dividend yield, while appealing, needs careful thought about its long-term durability next to the company's growth goals.

Lynch stressed that a screen is only the beginning for more investigation. The cyclical pattern of shipping rates, worldwide oil demand directions, and fleet update plans are all important factors a long-term investor must know before making a decision. The method's achievement depends on holding during market cycles, if the company's fundamental story stays unchanged.

Finding More GARP Possibilities

DHT Holdings is one of a number of companies that presently fit the disciplined standards of the Peter Lynch investment method. Investors curious about finding other possible "growth at a reasonable price" candidates can view the live screen and its outcomes here.

Disclaimer: This article is for informational purposes only and does not constitute financial advice, a recommendation, or an offer or solicitation to buy or sell any securities. The investment strategy discussed does not guarantee results. All investing involves risk, including the potential loss of principal. Investors should conduct their own independent research and consider their individual financial circumstances before making any investment decisions.