For investors looking to balance the search for growth with some caution, the "Growth at a Reasonable Price" (GARP) or "Affordable Growth" strategy offers a practical middle path. This method tries to find companies that are increasing their earnings and sales at a good rate and are also available at prices that are not too high. By looking for stocks with good growth scores, reliable profit and financial condition, and a price that is not too steep, investors can search for chances where the market may not yet see all the future possibility. One stock that recently appeared from this search is CareTrust REIT Inc (NYSE:CTRE).

CareTrust REIT is a real estate investment trust that owns, buys, and rents healthcare properties, mainly skilled nursing and senior housing facilities across the United States. As a net-lease REIT, its operation relies on collecting steady rental income, which creates a base for consistent cash flow and dividend payments.

A Notable Growth Picture

The center of the affordable growth idea for CareTrust depends on its very good growth measures, which are a main part of the search method. According to ChartMill's fundamental analysis report, CTRE gets a high Growth Rating of 9 out of 10. This score comes from strong results in both the recent past and the expected future.

- Past Results: The company has shown marked enlargement, with Revenue increasing 59.24% over the last year and Earnings Per Share (EPS) rising a notable 90.28%. Over a longer several-year time, the growth stays firm, with yearly Revenue growth of 12.64% and EPS growth of 11.30%.

- Future Predictions: Importantly for a growth investor, this pace is forecast to keep going. Analysts predict good forward growth, with EPS expected to go up by 26.18% each year and Revenue by 27.43%. The report states that this shows a quickening from past rates, implying the company's growth path is getting better.

This mix of solid past results and a quickening view is what growth-focused searches aim to find, as it points to a company that is effectively growing its activities.

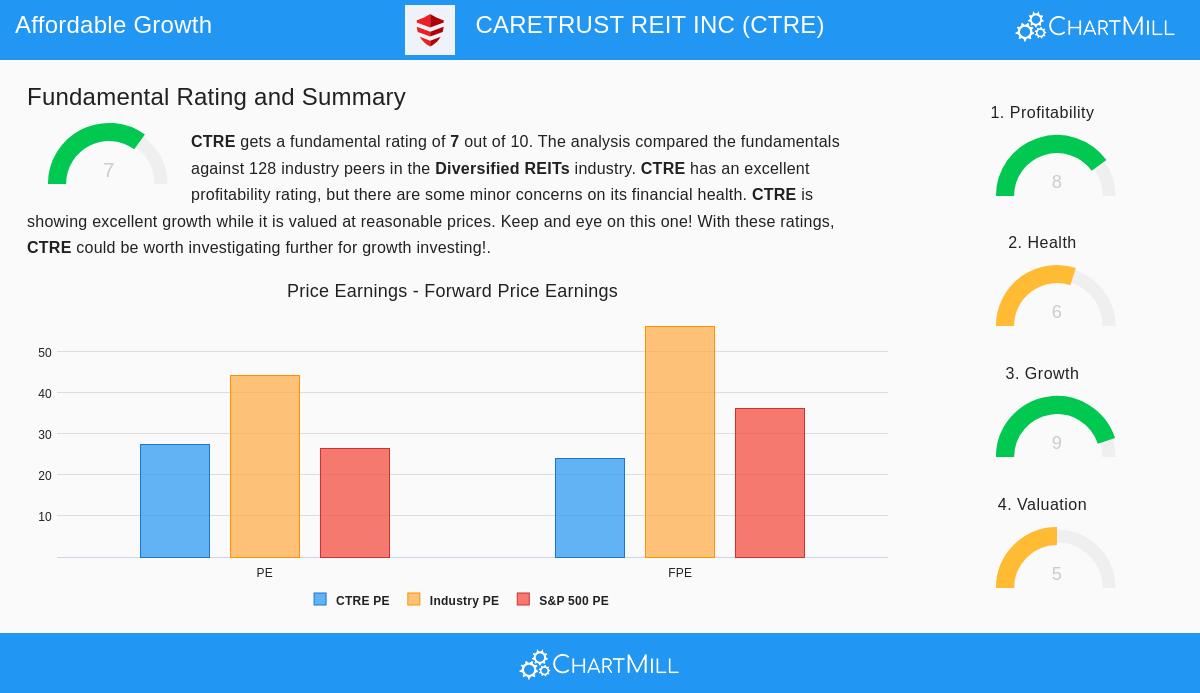

Price Consideration

While growth is needed, the "affordable" or "reasonable price" part is what separates this method from pure trend investing. CareTrust's Valuation Rating of 5 out of 10 shows a varied but finally sensible view when examined completely.

On the face, some absolute price measures seem high. The Price/Earnings (P/E) ratio of 27.52 and Forward P/E of 24.00 can be seen as expensive. However, the search thinking focuses on relative cost and growth payback:

- Sector Contrast: Even with its high absolute P/E, CTRE is priced lower than 71% of similar companies in the Diversified REITs field based on its trailing P/E and lower than 86% based on its forward P/E. This shows the stock is not overly costly within its own industry.

- Growth Payback: The important measure here is the PEG ratio, which changes the P/E for predicted earnings growth. ChartMill's report points out that CTRE's low PEG ratio shows a "rather low price" when its growth rate is included. This is the main point of the GARP case: you are paying for growth, but not an extreme extra amount for it.

- Profit Support: As mentioned in the report, CTRE's "excellent profitability rating may support a higher PE ratio." This relationship between price and other basic strengths is a key section of a full review.

Supporting Basics: Profit and Condition

For growth to last and for a sensible price to be a real chance, a company must have a stable base. The search rules require acceptable scores in Profit and Financial Condition, and CareTrust meets this here.

Profit is a clear positive, with a rating of 8. The company has very good margins, including a Profit Margin of 60.84% and an Operating Margin of 66.50%, which are in the top 1% of its field. Its returns on assets, equity, and invested capital are all above field averages, showing good use of money to create earnings.

Financial Condition gets a rating of 6. The view here is one of strength in cash and debt position, with some small points to note. The company has a very good financial position with a low Debt/Equity ratio of 0.22 (better than 97% of peers) and very good cash ratios (Current and Quick Ratios of 4.05). The Altman-Z score shows no bankruptcy danger. The noted points include a high dividend payout ratio and a past of share increase, which investors should watch, but they are not serious enough to weaken the overall good condition check.

Conclusion

CareTrust REIT Inc shows an example of the affordable growth search reasoning. It displays the high-speed growth in revenue and earnings that growth investors want, together with predictions for that growth to quicken. While its P/E numbers are not small alone, they seem sensible compared to its field and, most significantly, are balanced by its high growth rate and excellent profit. Backed by strong margins and a financially sound position, CTRE fits the method of searching for companies where growth possibility may not yet be completely seen in the present stock price.

This review of CTRE came from a specific Affordable Growth search. Investors wanting to examine other companies that meet similar rules of strong growth, sensible price, and solid basics can find more possible choices through the original search here.

Disclaimer: This article is for information only and is not financial advice, a suggestion, or an offer to buy or sell any security. The review uses data and ratings from ChartMill. Investors should do their own research and think about their personal money situation and risk comfort before making any investment choices.