Investors looking for expansion possibilities at fair costs frequently use a method called Growth At Reasonable Price, or GARP. This method tries to find companies that show good expansion prospects without the high prices usually linked to fast-growing stocks. By concentrating on businesses with reliable expansion paths, satisfactory earnings, and sound finances that are not too expensive, investors try to mix the search for growth with careful price assessment. This process helps prevent both costly growth narratives and inactive value investments, focusing on companies ready for continued progress.

COTERRA ENERGY INC (NYSE:CTRA) appears as a noteworthy option under this method, especially for investors focused on the energy industry. The company's varied activities in the Permian Basin, Marcellus Shale, and Anadarko Basin offer several paths for expansion while distributing business risk. As an exploration and production company concentrated only on U.S. assets, Coterra gains from local energy rules and infrastructure benefits.

Expansion Path

Coterra displays notable expansion traits that fit well with the low-cost growth method. The company's recent results show considerable growth, with a number of important measures pointing to good momentum:

- Revenue expansion of 25.13% over the last year

- Earnings Per Share rising by 26.74% each year

- Five-year average revenue expansion of 21.44% per year

- Anticipated future EPS expansion of 16.79% annually

- Forecasted revenue expansion of 16.04% in the next years

The quickening between past EPS expansion and future projections indicates the company is starting a period of improved operational performance and market standing. This solid expansion outline builds the base for the GARP method, as investors look for companies with proven growth abilities instead of only theoretical possibility.

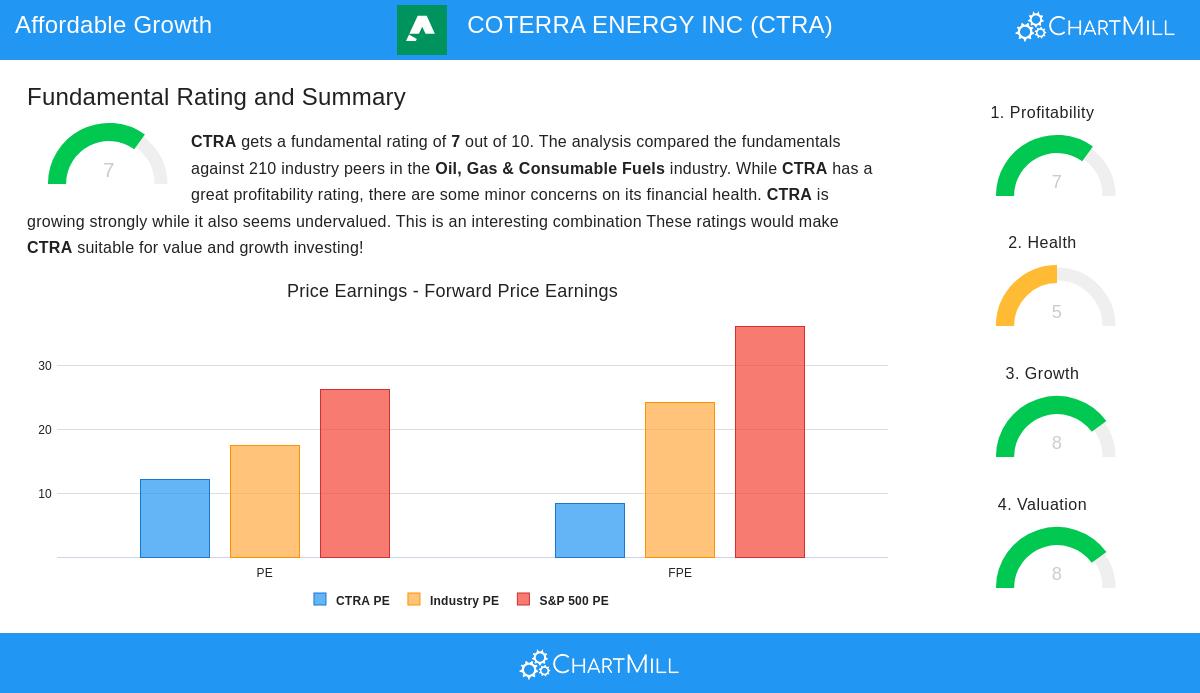

Price Evaluation

The price measures for Coterra create a noteworthy case for investors looking for fairly priced expansion chances. The company's present price multiples indicate the market might not be completely valuing its expansion outlook:

- Price/Earnings ratio of 12.11, under industry normal

- Price/Forward Earnings ratio of 8.39, much lower than S&P 500 normal

- Enterprise Value to EBITDA good compared to 72% of industry counterparts

- Price/Free Cash Flow ratio more appealing than 64% of rivals

These price traits are vital for the low-cost growth method, as they show the market has not overvalued the company's expansion possibility. The moderate P/E ratio relative to good expansion rates forms what value investors often call a "margin of safety" while still capturing expansion forces.

Earnings and Money Strength

Beyond expansion and price, Coterra keeps acceptable earnings and money strength marks that back the total investment idea. The company's earnings score of 7/10 mirrors several positive points:

- Return on Invested Capital of 7.86%, doing better than 71% of industry counterparts

- Profit margin of 23.25%, superior to 80% of rivals

- Operating margin of 31.31% and gross margin of 82.81%, both industry-best

- Steady positive earnings and cash flow over five years

The money strength rating of 5/10 shows some points for watching but general steadiness:

- Debt-to-Equity ratio of 0.25 shows medium borrowing

- Debt-to-FCF ratio of 2.71 indicates workable debt amounts

- Current ratio of 1.02 shows enough short-term cash availability

- Share count decrease in the last year shows capital control

These earnings and strength measures supply the basic steadiness that expansion investors need, making sure that growth is not happening at the cost of money firmness.

Tactical Placement

Coterra's operational variety across several U.S. basins gives natural protection against local price differences and business interruptions. The company's presence in the Permian, Marcellus, and Anadarko areas permits capital distribution to the most promising chances while keeping output steadiness. This geographical variety supports the money traits that make it appropriate for low-cost growth investing.

The company's basic study report shows a balanced outline with special force in expansion and price aspects, just what GARP investors look for. The mix of good expansion measures, fair price, acceptable earnings, and enough money strength forms a noteworthy outline for investors who want expansion contact without paying too much.

For investors focused on finding similar low-cost expansion chances, more screening outcomes can be viewed using our Affordable Growth Stock Screener.

Disclaimer: This article provides factual information and study for learning reasons only and does not form investment guidance, suggestion, or support of any security. Investors should do their own study and talk with money consultants before making investment choices. Past results do not assure future outcomes, and all investments hold risk including possible loss of original money.