A growth investing strategy described in Louis Navellier's "The Little Book That Makes You Rich" uses eight fundamental rules to find companies with high growth potential. This method concentrates on firms showing solid and improving financial numbers across earnings revisions, sales growth, profitability, and cash flow creation. The process aims to find stocks early in their growth phase by focusing on recent performance patterns and operational gains.

Fitting the Little Book Requirements

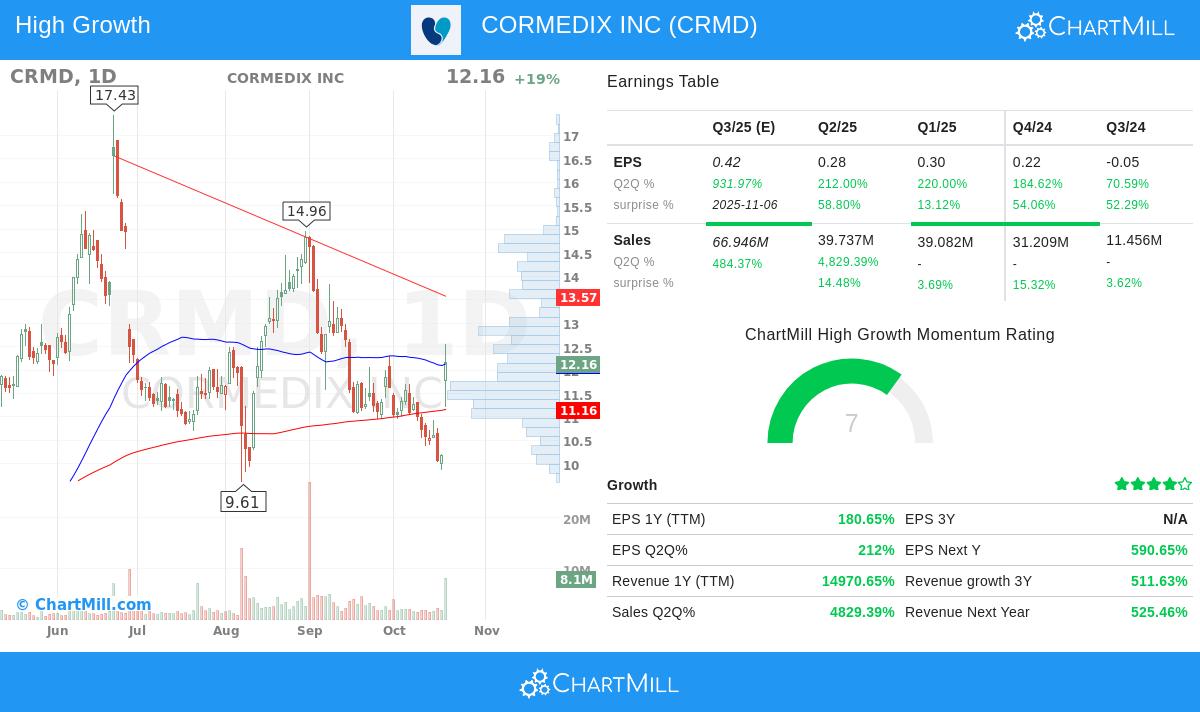

CorMedix Inc (NASDAQ:CRMD) shows very good fit with Navellier's growth model through several quantitative factors:

-

Earnings Revisions and Surprises: The company has an 81.8% upward revision in next-quarter EPS estimates over three months, greatly passing the 4% minimum. This points to high analyst belief in short-term results. CorMedix has reported four straight positive earnings surprises with an average beat of 44.6%, easily passing the strategy's need for three surprises with 10% average beats.

-

Strong Growth Numbers: The pharmaceutical company displays notable revenue increases with:

- 14,970.6% year-over-year revenue growth

- 4,829.4% quarter-over-quarter revenue growth These numbers greatly pass the strategy's 20% minimums for both measures, showing fast sales gains that growth investors look for.

-

Profitability Improvement: Operating margin growth of 100.6% over the last year is much higher than the 2% minimum. This shows the company's skill in turning revenue gains into profits more effectively, a main sign of lasting growth.

-

Cash Flow and Earnings Movement: Free cash flow increased 197% year-over-year, passing the 15% minimum. EPS growth numbers show solid improvement with 180.6% year-over-year growth and 212% quarter-over-quarter growth, both above the 15% needs. The present quarterly EPS growth of 212% is higher than the last quarter's growth, confirming positive earnings movement.

-

Return on Equity: With a 23.2% ROE, CorMedix is more than double the strategy's 10% minimum, pointing to good use of shareholder money to create profits.

Fundamental Analysis Summary

According to ChartMill's detailed fundamental analysis, CorMedix gets an overall score of 7 out of 10, with especially good results in several important areas. The company shows very good financial condition with no remaining debt, high liquidity ratios, and an Altman-Z score pointing to low bankruptcy chance. Valuation numbers seem good with forward P/E ratios below industry averages, indicating possible undervaluation compared to growth outlook.

The analysis mentions outstanding profitability margins, including a 42.1% profit margin and 40.6% operating margin, both placed in the top groups within the pharmaceuticals industry. Growth forecasts stay solid with expected EPS growth of 57.7% and revenue growth of 63.4% each year in future periods, though analysts mention some slowing from recent high growth rates.

Investment Points

While CorMedix shows notable fit with growth requirements, investors should be aware of the company's shift toward commercial sales of its main product DefenCath. The very high growth rates mirror this sales start period, which may become more standard with time. The company's fairly small market size and recent profitability after years of development-stage work are other points for thought.

The mix of good fundamental numbers, attractive valuation compared to growth rates, and fit with systematic growth requirements makes CorMedix worth more study for growth-focused investors. The company's place in the catheter-related bloodstream infection prevention market meets an important healthcare need with little competition.

Find Other Possible Choices

This review of CorMedix shows how the Little Book strategy can find interesting growth chances. Investors wanting to look at other companies meeting these strict requirements can view the full screening results for more research.

Disclaimer: This article provides factual information and analysis for educational purposes only and is not investment advice, a suggestion, or a support of any security. Investors should perform their own research and talk with financial advisors before making investment choices.