For investors looking to balance the search for growth with some caution, the "Growth at a Reasonable Price" (GARP) or "Affordable Growth" strategy offers a practical middle path. This method tries to find companies that are increasing their sales and profits at a good rate while also trading at prices that are not overly high. It avoids the high risk of expensive, unprofitable growth stocks while steering clear of the cheap stocks of companies that are not improving. One way to use this strategy is through a structured filter, searching for stocks with good growth scores, stable profit and financial condition, and a price that is still sensible. Corcept Therapeutics Inc (NASDAQ:CORT) recently appeared from such a filter, making it worth an examination to see if its financial details fit the affordable growth idea.

Growth Path: Past Performance and Future Speed

The central idea of any growth investment is a company's ability to get bigger, and Corcept Therapeutics shows this ability firmly. The company's Growth Rating of 8 out of 10 shows good points in both past results and what is predicted ahead. Revenue growth has been especially notable, rising by 17.92% over the last year and averaging a 17.11% yearly growth rate over recent years. This steady sales increase is a good sign of commercial success for its main product, Korlym, and its research projects.

Maybe more important for the affordable growth investor is the view of the future. Analysts predict a notable quickening in growth:

- Earnings Per Share (EPS) is expected to grow by 44.06% each year.

- Revenue is forecast to rise by 23.55% per year.

This predicted quickening from already-sound past rates indicates the company could be starting a new stage, possibly helped by new drug uses or larger markets. For a GARP strategy, this mix of established growth and a speeding-up forecast is an important beginning, as it supplies the "growth" part without depending only on far-off future hopes.

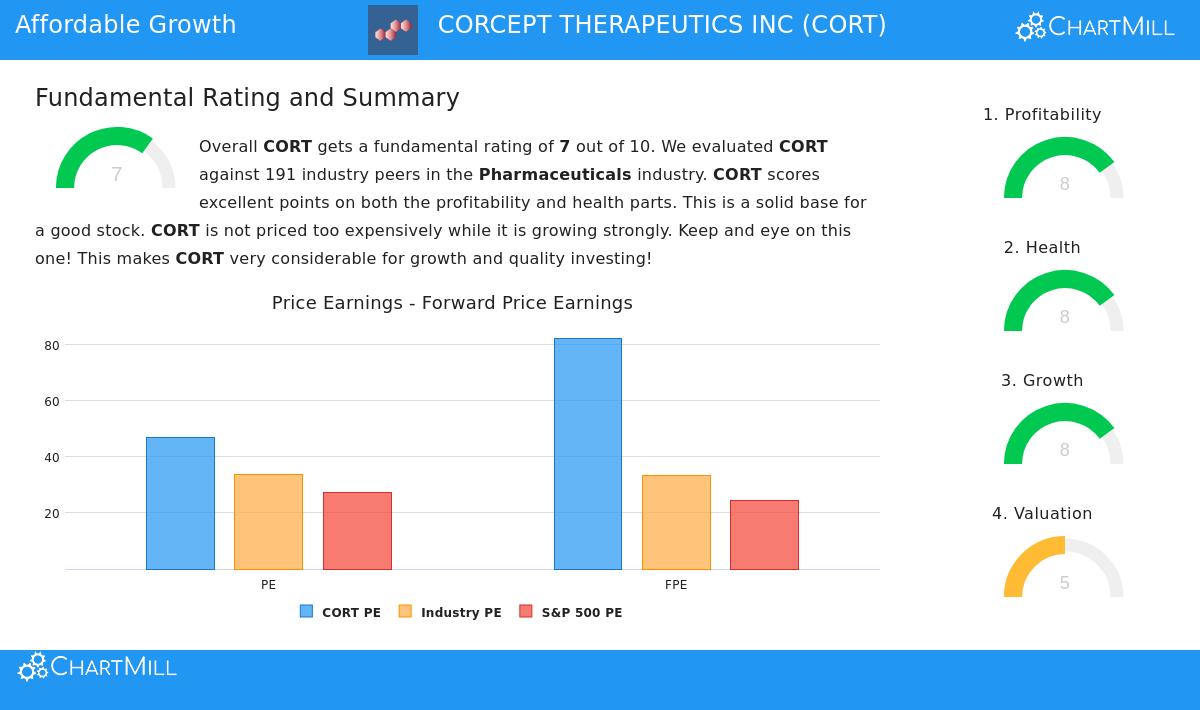

Valuation Setting: A Relative Discount in a Costly Field

Valuation is where the "reasonable price" or "affordable" part of the strategy is checked. Corcept's Valuation Rating of 5 shows a detailed picture. On a simple basis, common measures seem high. The stock trades at a Price/Earnings (P/E) ratio of 46.93 and a forward P/E of 82.30, which are costly next to the wider S&P 500.

However, valuation is frequently relative, particularly for growth stocks in specific fields like drug manufacturing. Here, Corcept's situation becomes more engaging:

- Its P/E ratio is less expensive than nearly 77% of other companies in its drug industry.

- Looking at Enterprise Value to EBITDA, it is priced more cheaply than about 77% of the industry.

- Its Price/Free Cash Flow ratio is below 83% of industry rivals.

This shows that while the stock has a high price in a simple sense, it is placed at a relative markdown within its own high-achieving, research-heavy field. The valuation score recognizes that a higher multiple could be reasonable given the company's excellent profit and its strong predicted earnings growth of over 33% in the next few years. For the affordable growth filter, this relative price within a growth situation is exactly what it aims to find.

Basic Financial Soundness: Condition and Earnings

A filter for affordable growth smartly includes tests for financial condition and earnings. These elements confirm the company has the steadiness to handle difficulties and the business model to turn growth into returns for shareholders. Corcept does very well here, with Condition and Earnings Ratings both at 8.

Financial Condition is very strong. The company has no debt, setting its Debt/Equity ratio at zero—a top-level position that removes interest costs and failure risk. Its Altman-Z score of 16.35 points to very low financial trouble risk, and good cash ratios (Current Ratio of 3.14) confirm it can easily cover near-term needs.

Earnings measures are just as solid, supporting the growth story:

- Return on Equity (ROE): 16.79%

- Return on Assets (ROA): 12.88%

- Profit Margin: 14.32%

- Gross Margin: A very high 98.19%

These numbers are not just acceptable; they are in the top levels of the drug industry, doing better than 80-90% of similar companies in many areas. This high-quality earnings is important for the affordable growth idea, as it means the company's growth is financially worthwhile and is not being pushed by spending that cannot last or bad use of money.

Summary and Next Steps

Corcept Therapeutics Inc shows an interesting example for the affordable growth method. It joins a solid, speeding-up growth picture—especially in future EPS and revenue forecasts—with a valuation that, while high in simple terms, is relatively appealing within its high-profit, high-growth field. This possible "reasonable price" for its growth is supported by a very strong balance sheet with no debt and top-level earnings measures. The company’s financial details indicate it is a sound organization able to pay for its own expansion while providing very good returns on investment.

A complete detailed review of these financial elements is provided in the ChartMill Fundamental Analysis Report for CORT.

For investors wanting to use this structured method to find other possible choices, the exact "Affordable Growth" filter that found Corcept Therapeutics can be viewed and changed here: Discover More Affordable Growth Stocks.

Disclaimer: This article is for information and learning only and is not a suggestion to buy, sell, or keep any security. The review is based on given data and financial ratings, which can change. Investing has risk, including the chance of losing the original investment. Readers should do their own complete research and think about their personal money situation and risk comfort before making any investment choices.