For investors looking to balance the search for growth with a degree of caution, the "Growth at a Reasonable Price" (GARP) method presents a noteworthy middle path. This method looks for companies with good and lasting growth paths, but whose shares are not valued at the high levels common to popular momentum stocks. By concentrating on firms with sound basic operations, including good balance sheets and steady earnings, the method tries to find chances where the market may not have completely accounted for future prospects, possibly providing an appealing balance of risk and reward. One stock that recently appeared from this type of screening process is CBRE Group Inc - A (NYSE:CBRE), the world's top commercial real estate services firm.

Growth Profile: A Main Feature

The main attraction of CBRE within a GARP structure is its good growth traits, which gave it a ChartMill Growth Rating of 7 out of 10. The company is showing positive movement in both its recent results and its estimated future.

- Good Recent Results: In the last year, CBRE reported notable growth with Revenue rising by 14.61% and Earnings Per Share jumping by 43.41%. This shows not only revenue growth but also effective profit generation.

- Positive Future Expectations: The growth trend is likely to persist. Analysts estimate an average yearly EPS growth of 17.98% and Revenue growth of 9.04% in the next few years. Importantly, the EPS growth rate is forecast to rise compared to its past average, hinting at better operational performance or positive market factors.

- Sector Background: This growth is happening inside the cyclical real estate industry, making CBRE's steady growth and positive estimates especially notable for investors wanting involvement in this market.

Valuation: Moderate Given the Situation

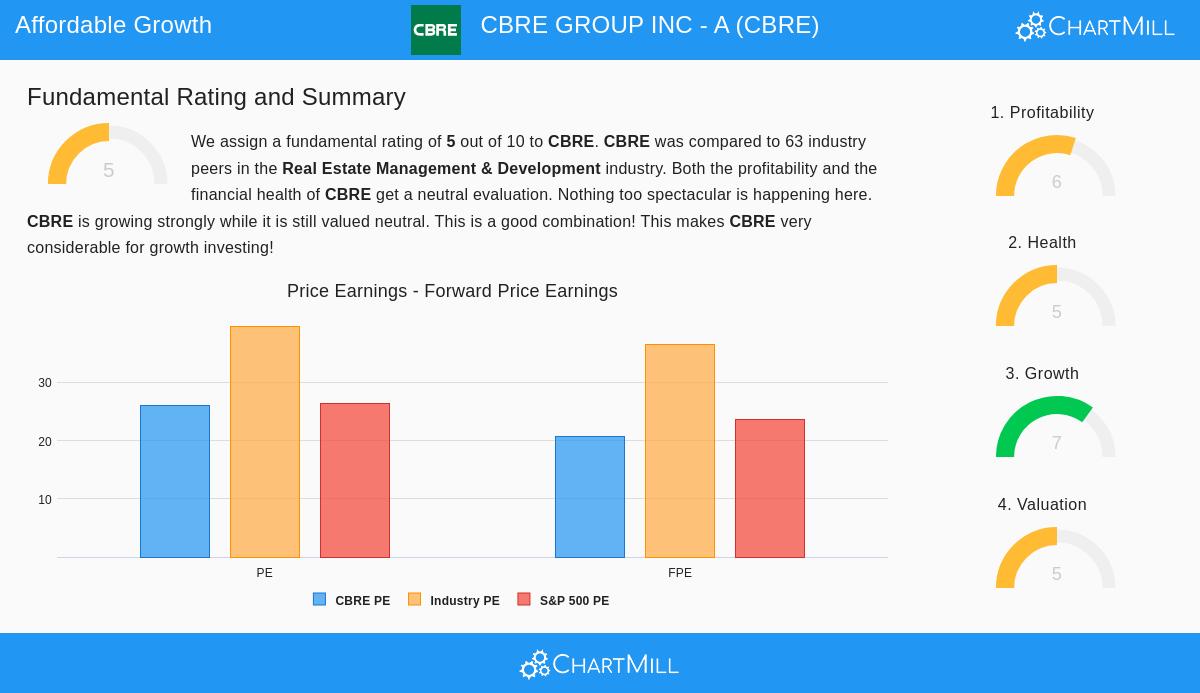

A central idea of affordable growth investing is steering clear of very high prices. CBRE's ChartMill Valuation Rating of 5 points to a varied but finally moderate view when considered next to its growth and industry counterparts.

- Absolute Compared to Relative Measures: On a basic level, CBRE's Price/Earnings (P/E) ratio of 25.98 and Price/Forward Earnings ratio of 20.71 might seem high. However, the valuation picture looks better through a comparison.

- Industry Price Difference: CBRE sells for a notable price below its industry group. Its P/E ratio is lower than about 75% of similar companies in the Real Estate Management & Development industry, where average valuations are much higher.

- Growth Adjustment: The Price/Earnings to Growth (PEG) ratio, which includes estimated earnings growth, shows a fairly low valuation. This measure is important for GARP investors, as it helps decide if the growth price being paid is fair.

Supporting Basics: Stability and Earnings

For growth to be lasting and the valuation to be sound, a company needs a firm financial base. CBRE's scores in financial stability (5) and earnings (6) are considered "acceptable" within the screening rules, giving necessary support for the growth argument.

- Earnings Quality: The company achieves high marks on return measures, with a Return on Equity of 14.39% and Return on Invested Capital of 6.76%, doing better than a big portion of industry rivals. This shows good use of shareholder money.

- Financial Stability Points: CBRE's financial strength is sufficient, with an Altman-Z score showing no short-term bankruptcy danger and a Debt-to-Equity ratio similar to industry averages. Still, investors should be aware that liquidity ratios (Current and Quick Ratio) are somewhat low next to peers, which is typical for service-based firms in this field but needs attention.

- No Income Distribution: It is key to see that CBRE does not provide a dividend, which matches a strict growth focus as the company probably puts earnings back into operations to support more growth.

Conclusion: A Subject for More Study

CBRE Group presents a situation that fits the central ideas of affordable growth investing. The company shows a noteworthy growth profile characterized by good recent outcomes and a rising earnings forecast. Its valuation, while not a bargain, seems moderate, and even interesting, when evaluated next to its own growth speed and the valuations held by its industry counterparts. The acceptable, though not outstanding, scores in financial stability and earnings provide a basic verification, indicating the growth is not being chased without care.

For investors, CBRE represents a possible way to gain involvement in worldwide commercial real estate activity through a top market franchise that is delivering growth while selling at a comparative discount. As with all investments, this review should act as a beginning for more detailed investigation.

You can examine the complete basic analysis report for CBRE Group Inc - A here.

Want to find more stocks that match this "Affordable Growth" description? Our stock screening tool can help you find other possible choices. Click here to see the screen and view more outcomes.

Disclaimer: This article is for information only and is not financial guidance, a suggestion, or a bid to buy or sell any securities. The analysis uses data and ratings from ChartMill, and investors should do their own separate study and talk with a qualified financial consultant before making any investment choices. Past results do not guarantee future outcomes.