Consider CACI INTERNATIONAL INC -CL A (NYSE:CACI) as an affordable growth stock, identified by our stock screening tool. CACI is showcasing impressive growth figures and is well-positioned in terms of profitability, solvency, and liquidity. Moreover, it seems to be priced reasonably. Let's dive deeper into the analysis.

Evaluating Growth: CACI

ChartMill assigns a proprietary Growth Rating to each stock. The score is computed by evaluating various growth aspects, like EPS and revenue growth. We take into account the history as well as the estimated future numbers. CACI was assigned a score of 7 for growth:

- The Earnings Per Share has grown by an impressive 25.10% over the past year.

- The Earnings Per Share has been growing by 15.03% on average over the past years. This is quite good.

- Looking at the last year, CACI shows a quite strong growth in Revenue. The Revenue has grown by 14.16% in the last year.

- CACI shows quite a strong growth in Revenue. Measured over the last years, the Revenue has been growing by 8.97% yearly.

- CACI is expected to show quite a strong growth in Earnings Per Share. In the coming years, the EPS will grow by 13.18% yearly.

- Based on estimates for the next years, CACI will show a quite strong growth in Revenue. The Revenue will grow by 8.33% on average per year.

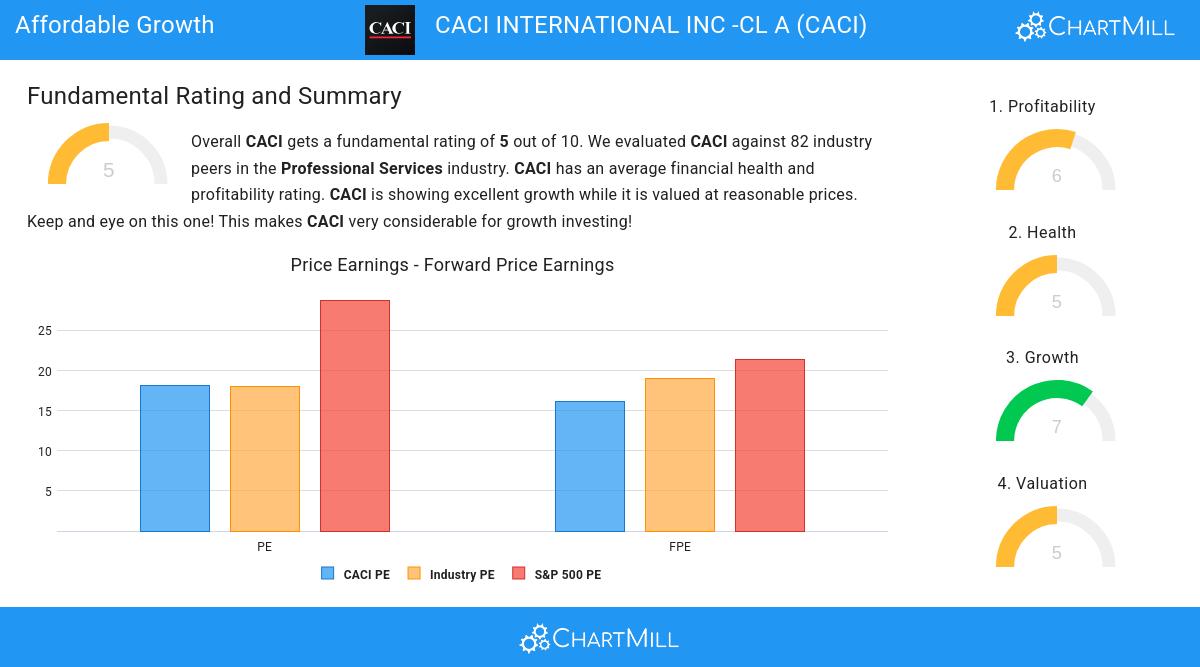

How do we evaluate the Valuation for CACI?

ChartMill provides a Valuation Rating to every stock, ranging from 0 to 10. This rating assesses various valuation aspects, comparing price to earnings and cash flows, while considering factors like profitability and growth. CACI boasts a 5 out of 10:

- CACI's Price/Earnings ratio indicates a valuation a bit cheaper than the S&P500 average which is at 28.78.

- Based on the Price/Forward Earnings ratio, CACI is valued a bit cheaper than 63.41% of the companies in the same industry.

- Compared to an average S&P500 Price/Forward Earnings ratio of 21.32, CACI is valued a bit cheaper.

- Compared to the rest of the industry, the Price/Free Cash Flow ratio of CACI indicates a somewhat cheap valuation: CACI is cheaper than 65.85% of the companies listed in the same industry.

- The low PEG Ratio(NY), which compensates the Price/Earnings for growth, indicates a rather cheap valuation of the company.

- CACI has a very decent profitability rating, which may justify a higher PE ratio.

- CACI's earnings are expected to grow with 12.78% in the coming years. This may justify a more expensive valuation.

Evaluating Health: CACI

A critical element of ChartMill's stock evaluation is the Health Rating, which spans from 0 to 10. This rating considers multiple health factors, including liquidity and solvency, both in absolute terms and relative to industry peers. CACI has received a 5 out of 10:

- An Altman-Z score of 3.36 indicates that CACI is not in any danger for bankruptcy at the moment.

- With a decent Altman-Z score value of 3.36, CACI is doing good in the industry, outperforming 65.85% of the companies in the same industry.

Looking at the Profitability

ChartMill assigns a proprietary Profitability Rating to each stock. The score is computed by evaluating various profitability ratios and margins and ranges from 0 to 10. CACI was assigned a score of 6 for profitability:

- The Return On Assets of CACI (5.56%) is better than 62.20% of its industry peers.

- The Return On Equity of CACI (12.87%) is better than 60.98% of its industry peers.

- The 3 year average ROIC (7.92%) for CACI is below the current ROIC(8.02%), indicating increased profibility in the last year.

- CACI has a better Profit Margin (5.70%) than 65.85% of its industry peers.

- CACI's Operating Margin of 9.19% is fine compared to the rest of the industry. CACI outperforms 73.17% of its industry peers.

- CACI's Operating Margin has improved in the last couple of years.

Our Affordable Growth screener lists more Affordable Growth stocks and is updated daily.

Check the latest full fundamental report of CACI for a complete fundamental analysis.

Disclaimer

This article should in no way be interpreted as advice. The article is based on the observed metrics at the time of writing, but you should always make your own analysis and trade or invest at your own responsibility.