BRISTOL-MYERS SQUIBB CO (NYSE:BMY) stands out as an undervalued stock with solid fundamentals, making it a potential candidate for value investors. The company’s strong profitability, reasonable financial health, and attractive valuation metrics suggest it may be trading below its intrinsic value.

Key Strengths

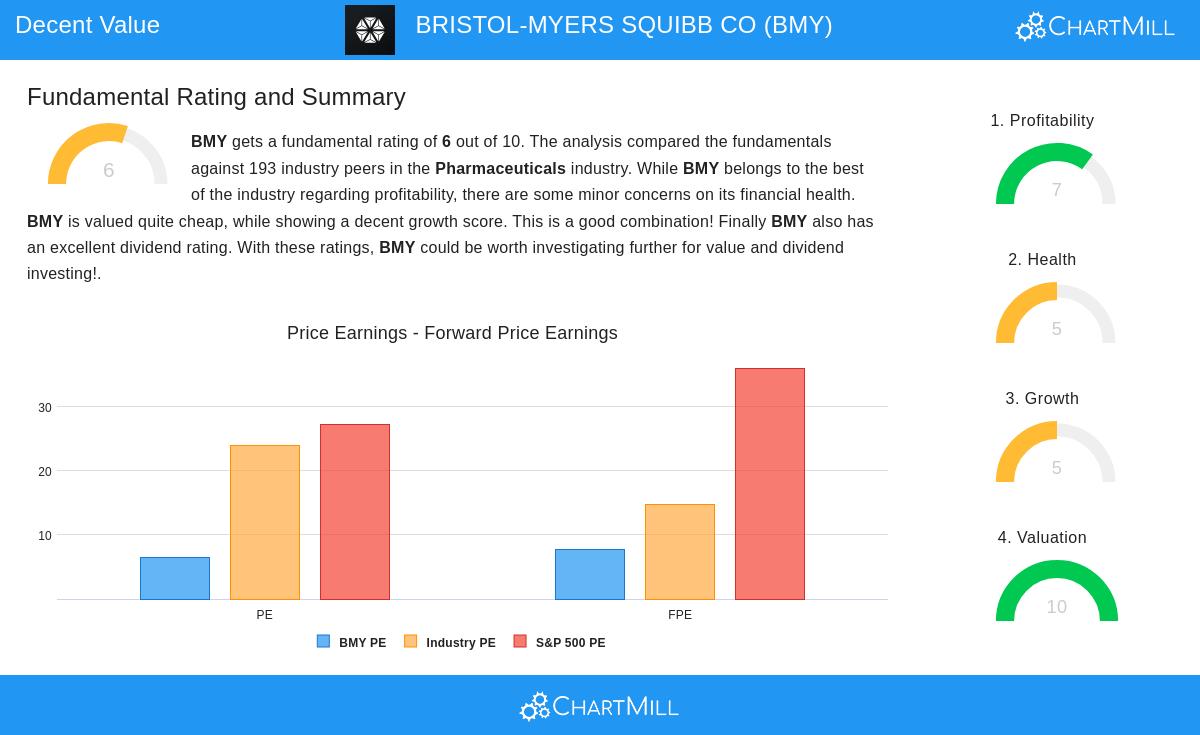

- Valuation (Score: 10/10) – BMY appears significantly undervalued with a P/E ratio of 6.43, well below both the industry average (23.90) and the S&P 500 (27.29). Its forward P/E of 7.67 also suggests a discount compared to broader market valuations.

- Profitability (Score: 7/10) – The company maintains strong margins, including an operating margin of 27.11%, outperforming 92.75% of its pharmaceutical peers. Return on equity (31.16%) and return on invested capital (14.88%) are also well above industry averages.

- Dividend (Score: 7/10) – BMY offers a high dividend yield of 5.11%, making it appealing for income-focused investors. While the payout ratio is high (90.59%), earnings growth supports sustainability.

- Financial Health (Score: 5/10) – Debt levels are elevated, but manageable, with a Debt/FCF ratio of 3.80, indicating it could repay debt in under four years using free cash flow. Liquidity metrics are adequate, though slightly below industry standards.

- Growth (Score: 5/10) – While past EPS growth has been volatile, future EPS is expected to grow at 36.74% annually. Revenue growth has been steady, though near-term projections show a slight decline.

Why It Fits a Value Strategy

BMY’s low valuation, combined with strong profitability and a high dividend yield, aligns with value investing principles. The stock trades at a discount despite solid fundamentals, presenting a potential opportunity if market sentiment improves.

For a deeper analysis, review the full fundamental report on BMY.

Our Decent Value Stocks screener lists more stocks with similar characteristics and is updated daily.

Disclaimer

This is not investment advice. The observations here are based on available data at the time of writing. Always conduct your own research before making investment decisions.