Thursday’s tape was a classic sector rotation day: defense and old-economy names carried the Dow higher while semis dragged the Nasdaq. Meanwhile, Washington’s geopolitics-and-spending firehose kept energy and defense traders busy and everyone else stared at Friday’s jobs report like it’s a season finale.

The index vibe: “Rotation, not capitulation”

The Dow’s proxy DIA finished higher, while the tech-heavy Nasdaq proxy QQQ slipped, basically the market saying, “Thanks for the AI rally, I’m going to walk it off.”

The selling pressure was most visible in semis and mega-cap tech, where even a small pullback feels dramatic because… well… the run-up has been anything but small. Reuters flagged broad tech weakness weighing on the S&P/Nasdaq session.

Macro pulse: productivity up, claims steady, trade gap… weirdly tiny

On the data front, the U.S. economy did its usual trick: refuse to look tidy.

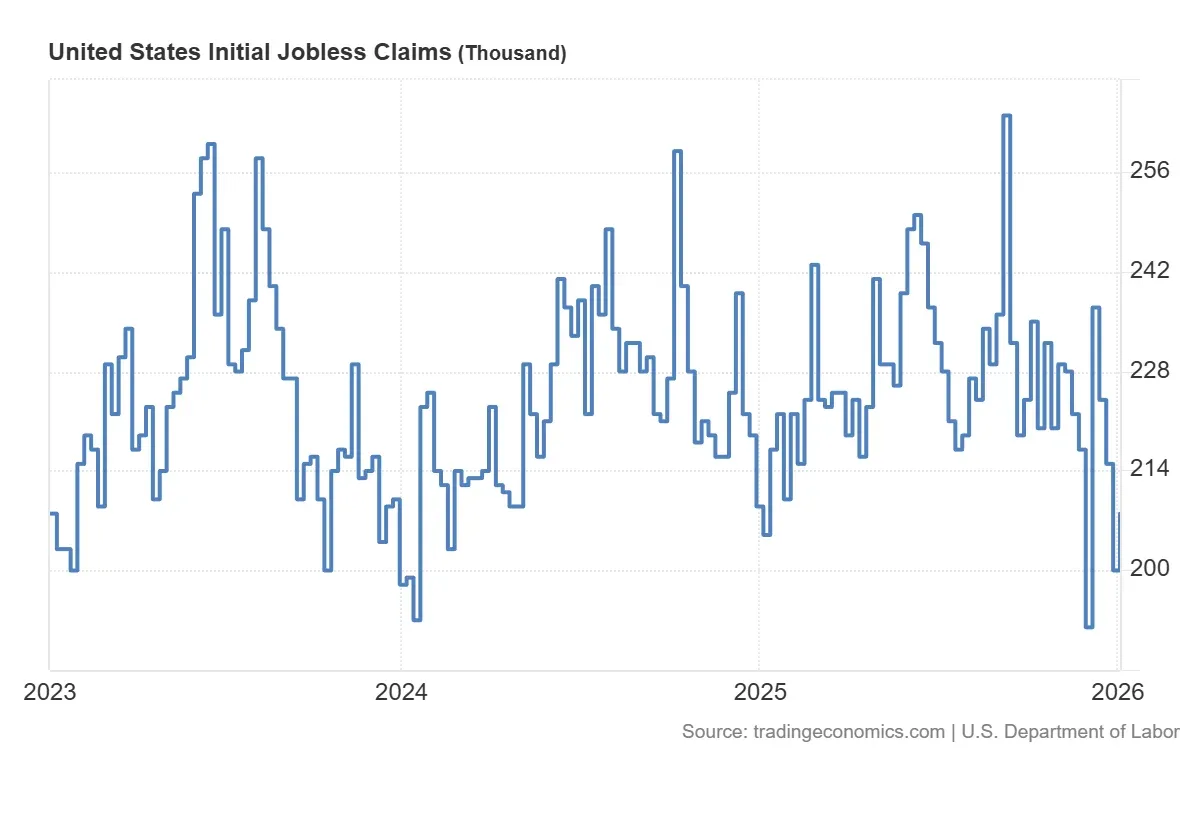

- Jobless claims ticked up by 8,000 to 208,000, still low enough to keep “recession” chatter mostly confined to people who get paid per hot take.

-

The more interesting headline: Q3 productivity jumped at a 4.9% annualized pace, while unit labor costs fell 1.9%, a combination that screams “efficiency gains” and whispers “AI is spreading into the real economy.”

-

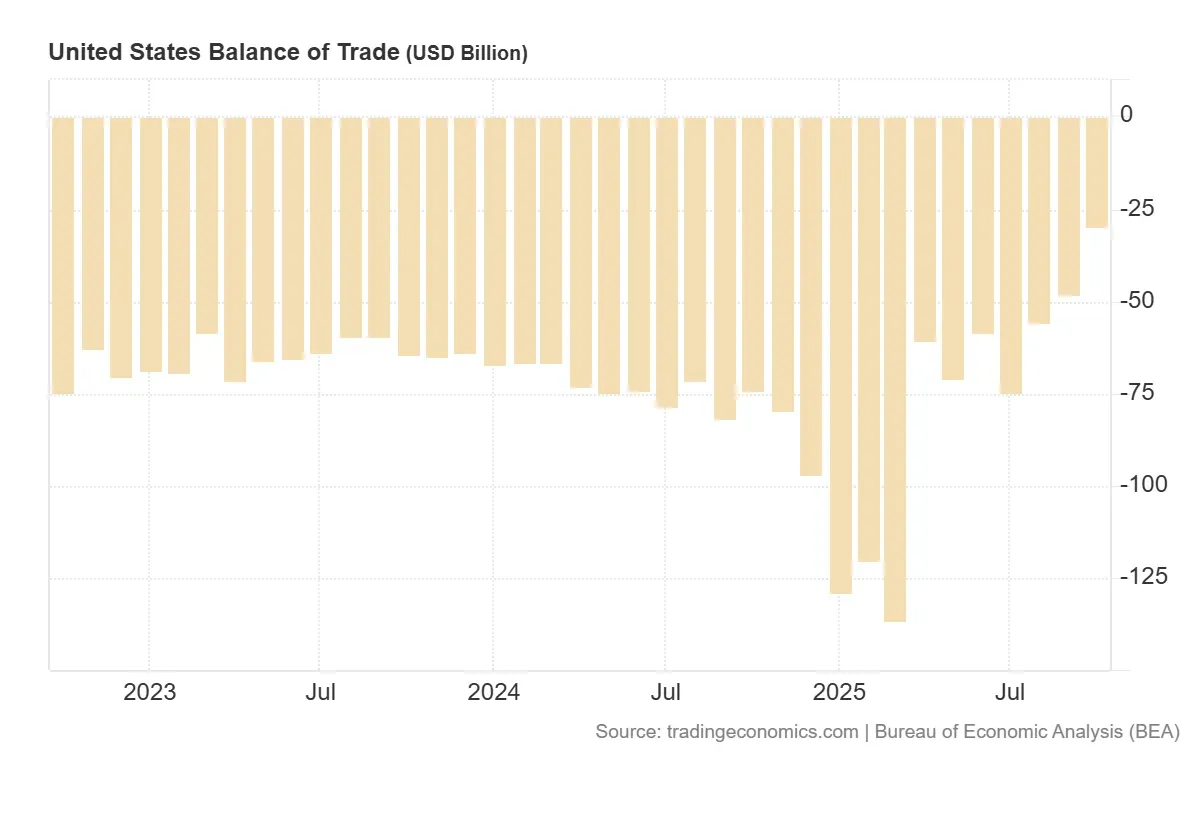

And then there’s trade: October’s U.S. trade deficit narrowed sharply to $29.4B, the lowest since 2009, thanks to rising exports and falling imports. It’s a meaningful number, but it also comes with the fine print that trade flows have been distorted by policy and timing effects.

The real story: chips sold off, defense caught a bid

Semis: profit-taking is a feature, not a bug

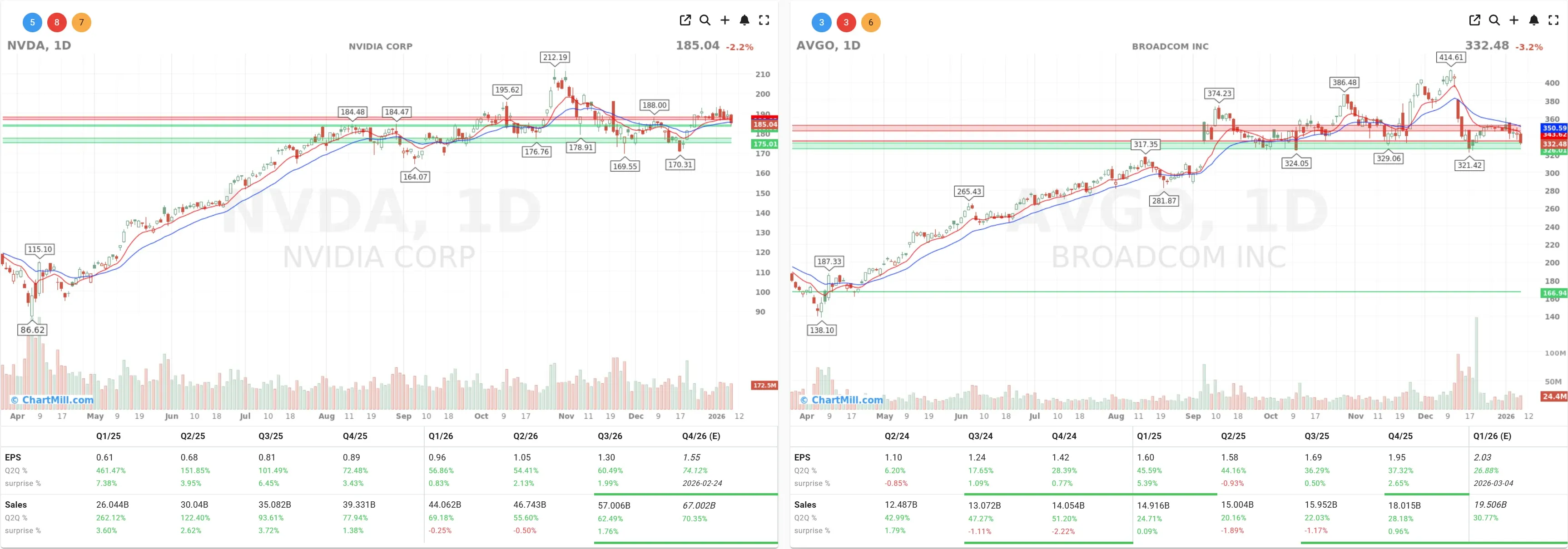

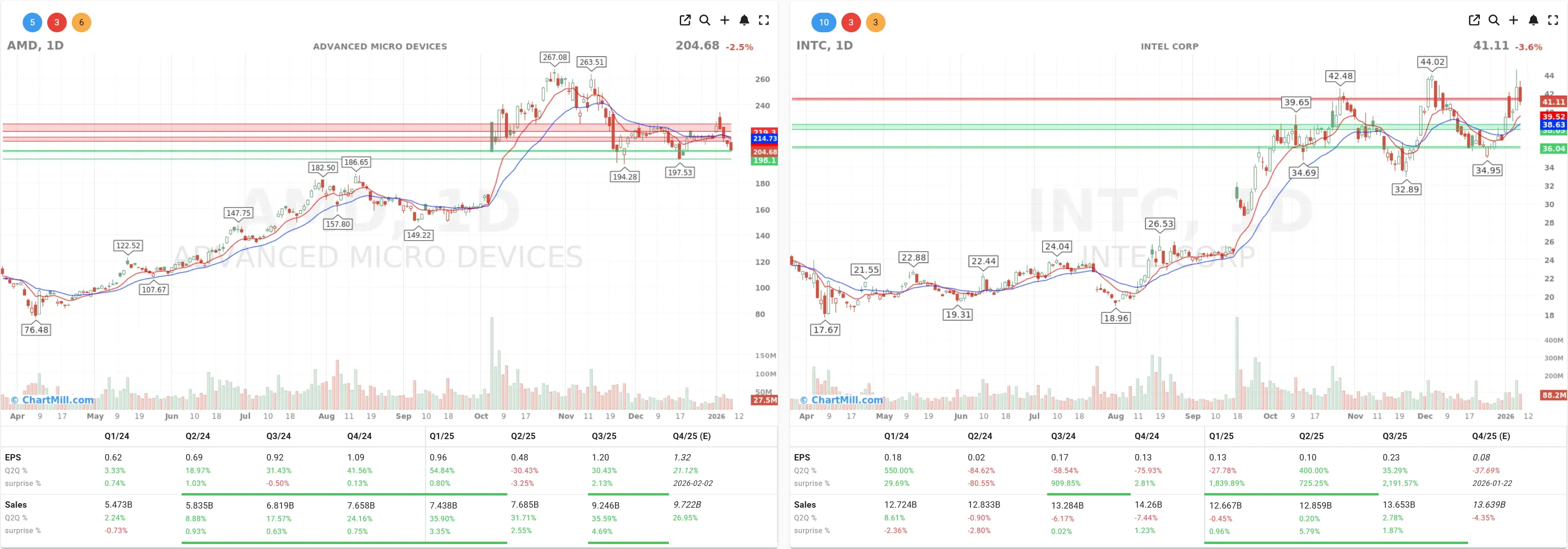

The semiconductor complex was the anchor. Nvidia (NVDA | -2.15%), Broadcom (AVGO | -3.21%), AMD (AMD | -2.54%) and Intel (INTC | -3.57%) all traded heavy.

This wasn’t “the AI story is dead.” It was more like the market exhaling, especially after the latest reminder that private AI funding is still operating in a different solar system: Anthropic (private) is reportedly eyeing a $10B raise at a $350B valuation. That kind of headline doesn’t hurt AI enthusiasm, it just nudges public-market traders to lock in some winnings.

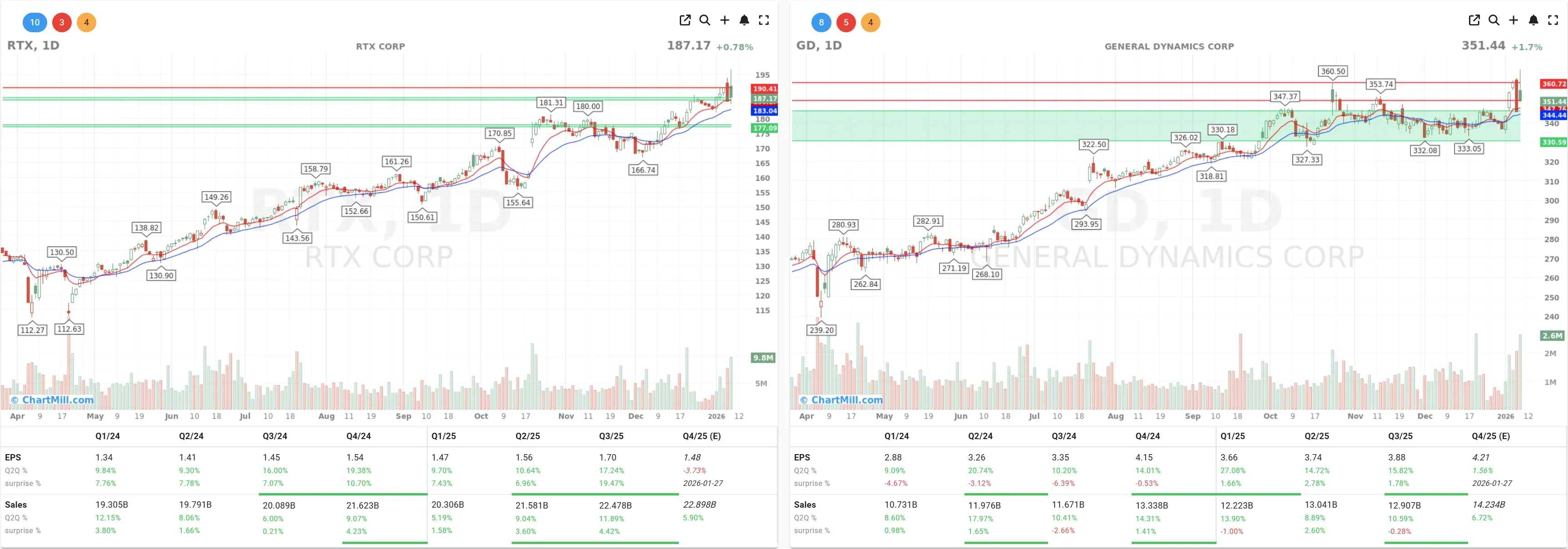

Defense: Washington turns the volume knob to 11

Defense stocks snapped back sharply after President Trump pushed for a $1.5T U.S. military budget in 2027, a dramatic jump versus the $901B approved for 2026, and a shift in tone after earlier talk about restricting payouts/buybacks in the sector. Markets heard the bigger number louder than the scolding.

The beneficiaries were exactly who you’d expect:

Lockheed Martin (LMT | +4.34%)

Northrop Grumman (NOC | +2.39%)

General Dynamics (GD | +1.68%)

RTX (RTX | +0.78%)

Company snapshots that mattered

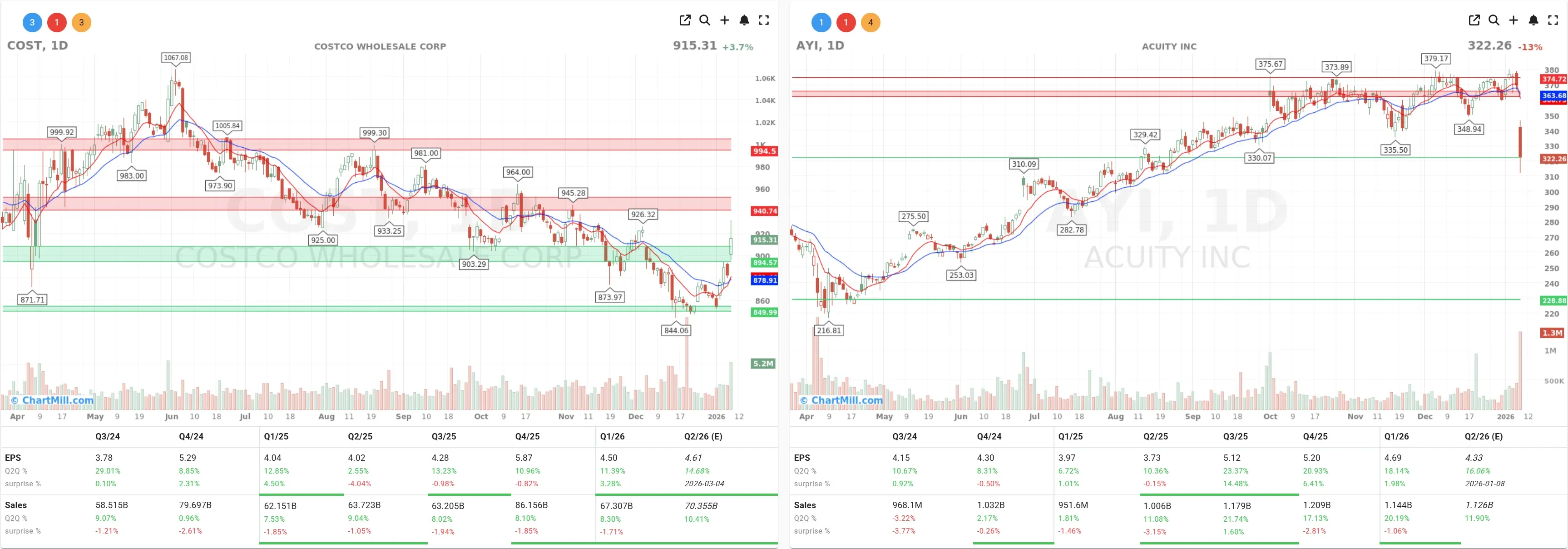

Costco reminded everyone the consumer isn’t dead

Costco (COST | +3.71%) put up strong December momentum - comparable sales up 7% - and the stock responded like a warehouse door on Black Friday: it swung open fast.

Acuity: good numbers, bad reaction

Acuity (AYI | -12.85%) sank hard after earnings despite reporting solid growth metrics. The takeaway: when expectations are high, “meeting estimates” can still feel like showing up late to your own birthday.

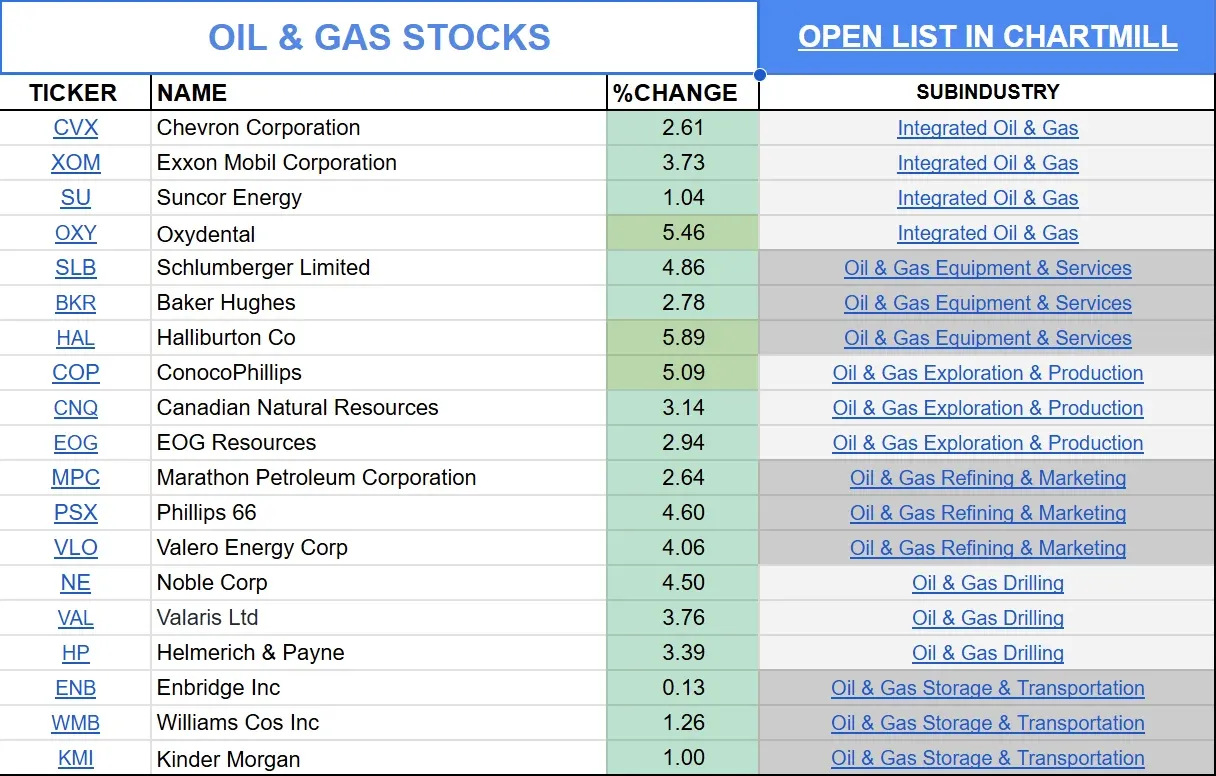

Geopolitics + energy: Venezuela and Greenland are not just “noise” anymore

Oil moved higher as headlines swirled around a reported U.S. plan to gain influence over Venezuela’s state oil company PDVSA, with Trump aiming to push crude toward $50/barrel. Whether that’s realistic is a separate argument (and a long one), but traders reacted to the direction of travel: more policy risk, more price sensitivity.

Add the Greenland thread - Trump’s renewed push to bring Greenland under U.S. control has become loud enough to generate real diplomatic churn - and you get a market that’s trying hard to focus on data, while geopolitics keeps poking it in the ribs.

My “so what” for investors heading into Friday

Thursday looked less like distribution and more like a rotation day with nerves showing: tech cooled, cyclicals and defense caught bids, and macro data provided enough “soft landing” fuel to keep the debate alive.

The next catalyst is straightforward: Friday, January 9’s U.S. jobs report. If payrolls come in hot, rates-sensitive tech could feel more gravity. If it cools meaningfully, the market may try to reheat the AI trade, because apparently we all forgot how to be bored.

Kristoff - ChartMill

Next to read: Rotation Day: Small Caps Push Higher While Breadth Firms Up