A basic analysis method for finding growth stocks at good prices involves looking for companies that show solid expansion potential without high valuations. This strategy, often called Growth At Reasonable Price (GARP) investing, mixes the search for companies with increasing revenue and earnings with the practice of paying fair prices. The method usually looks at stocks using several basic measures, focusing on those with strong growth paths, good profitability, sound financial states, and valuations that do not completely reflect future possibilities.

AMPHENOL CORP-CL A (NYSE:APH) appears as a noteworthy candidate under this system, getting an overall basic rating of 7 out of 10 from ChartMill's detailed analysis tool. The company's role as a designer and maker of electronic connectors and interconnect systems places it favorably inside technology infrastructure markets, serving various areas such as industrial, automotive, aerospace, and communications.

Growth Path

The company shows notable expansion numbers that are central to its investment case:

- Earnings Per Share grew 66.86% over the last year with a five-year average yearly growth rate of 15.11%

- Revenue increased 47.37% in the most recent year and holds a 13.10% compound yearly growth rate over five years

- Future estimates point to continued progress with EPS expected to grow 18.70% each year and revenue forecast to rise 14.42% per year

- The growth pattern shows EPS growth rates getting better from past to expected future periods

These growth features are especially significant for affordable growth investing because they show the company is gaining market position and growing efficiently, providing the basic expansion that leads to long-term shareholder returns without depending only on valuation changes.

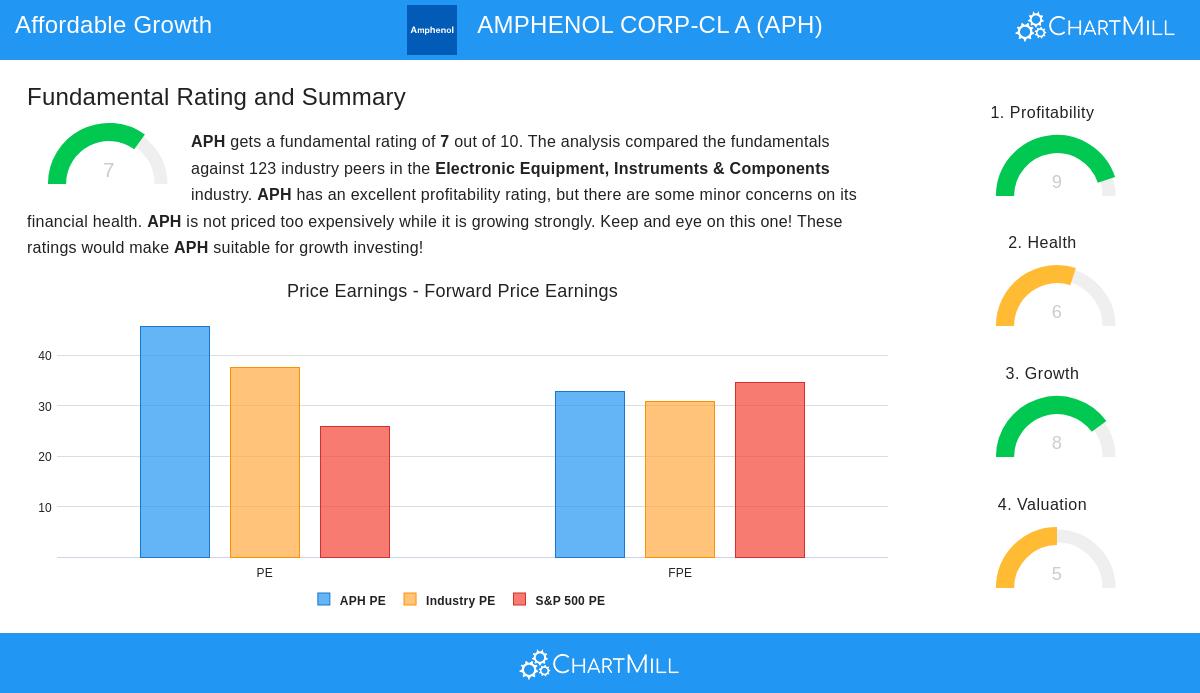

Valuation Check

While some standard valuation measures seem high, surrounding factors back the fair valuation idea:

- The P/E ratio of 45.80 is more than the S&P 500 average of 25.89 but matches industry standards

- Forward P/E of 32.90 looks good compared to both industry averages and wider market multiples

- The Price/Free Cash Flow ratio is at an appealing level, positioned better than 61.79% of industry companies

- Most importantly, the PEG ratio, which changes the P/E for growth, suggests an appealing valuation compared to earnings expansion outlook

For growth-at-reasonable-price methods, valuation cannot be viewed separately from growth rates. The company's higher earnings multiple seems more acceptable when looked at next to its strong expansion path and excellent profitability profile.

Profitability Quality

The company's operational skill gives a good base for its growth narrative:

- Return on Invested Capital of 19.87% is much better than 93.50% of industry rivals

- Operating margin of 25.01% is in the top group of the electronic components field

- Profit margin of 18.22% beats 95.94% of industry companies with steady improvement in recent years

- All main profitability measures, including ROA, ROE, and ROIC, show industry-leading performance

High profitability is vital for affordable growth investing because it points to lasting competitive strengths and supplies the money to support continued expansion without high debt or share dilution.

Financial State Points

The company keeps acceptable financial steadiness with some points to watch:

- Altman-Z score of 8.87 shows very low bankruptcy danger and is better than 86.99% of industry companies

- Debt-to-free-cash-flow ratio of 2.27 shows a workable debt situation

- Current and quick ratios show enough cash for operational requirements

- The primary issue relates to a rising share count over recent periods, although debt amounts stay acceptable

Financial state forms the third part of the affordable growth base, making sure companies can handle economic changes and keep putting money into growth projects without money troubles.

Investment Points

AMPHENOL CORP-CL A presents a noteworthy case for investors looking for growth at fair prices. The company mixes fast recent growth with steady historical expansion and positive future estimates. While the pure P/E multiple seems high, the valuation looks more fair when set against growth rates, future earnings potential, and excellent profitability. The financial state profile, while not ideal, gives enough steadiness to support continued operations and strategic plans.

For investors wanting to find similar chances, other affordable growth options can be found using the set screening method that found this stock. The screen picks companies showing solid growth features together with fair valuations and good basic foundations.

Disclaimer: This analysis uses basic data and ratings given by ChartMill and shows a neutral check of the company's financial numbers. It is not investment guidance or a suggestion to purchase, sell, or keep any security. Investors should do their own research and think about their personal money situation before making investment choices.