For investors looking to assemble a portfolio of lasting, high-performing businesses, the quality investing approach provides a structured system. This method centers on finding companies with durable competitive strengths, reliable profitability, sound financial condition, and the capacity to produce high returns on capital. The "Caviar Cruise" stock screen puts this thinking into practice by selecting for firms with a record of revenue and profit increase, outstanding returns on invested capital, reasonable debt, and trustworthy earnings. The aim is not to locate temporary discounts, but to discover businesses suitable for long-term holding.

A recent use of this screen has identified Aon PLC-Class A (NYSE:AON), a worldwide leader in professional services offering risk, health, and wealth solutions. The company’s profile indicates several traits that match the quality investing standards, making it a notable option for more study by investors using this method.

Performance and Profitability Metrics

The Caviar Cruise screen selects companies that display not only increase, but profitable and efficient increase. Aon’s past performance shows it meets and passes several of these important limits.

- Revenue and EBIT Growth: The screen demands a minimum 5% compound annual growth rate (CAGR) for both revenue and EBIT (earnings before interest and taxes) over five years. Aon’s EBIT growth of 11.11% greatly exceeds this mark, pointing to solid expansion in its core operational profitability. While its five-year revenue CAGR of 4.77% is just under the 5% filter, it shows consistent top-line expansion in an established industry.

- Profitability Expansion: A central idea of quality investing is gaining efficiency and pricing power, shown by EBIT growth exceeding revenue growth. Aon’s higher EBIT CAGR compared to its revenue growth confirms that more of each extra dollar of sales becomes operating profit, a signal of operational leverage and a firming business model.

- Outstanding Returns on Capital: Maybe the most important filter for quality is a high Return on Invested Capital (ROIC), which calculates how well a company produces profits from its capital base. The screen searches for an ROIC (excluding cash, goodwill, and intangibles) over 15%. Aon’s number of 114.84% is very high, putting it in the leading group of its industry. This shows that Aon’s business model—built on intellectual capital and client relationships—needs fairly little capital to create significant earnings, a characteristic of a quality franchise.

Financial Health and Earnings Quality

Quality investors look for companies with stable balance sheets and earnings supported by actual cash flow, ensuring endurance through economic cycles.

- Debt Management: The screen uses a Debt-to-Free Cash Flow (FCF) ratio below 5 to measure how fast a company could in theory pay off its obligations using its cash generation. Aon’s ratio of 4.74 falls within this acceptable band, implying its debt level is reasonable compared to the significant cash flow its operations create.

- Trustworthy Earnings: The Profit Quality metric, which compares free cash flow to net income, is set at a minimum 75% over five years. A number above 100% implies the company is turning all its accounting profits into cash—and more. Aon’s five-year average of 119.42% is much higher than the requirement, indicating that its reported profits are not only real but are also creating extra cash. This cash can be used to reinvest in the business, pay down debt, or return capital to shareholders, all without pressuring finances.

Fundamental Analysis Overview

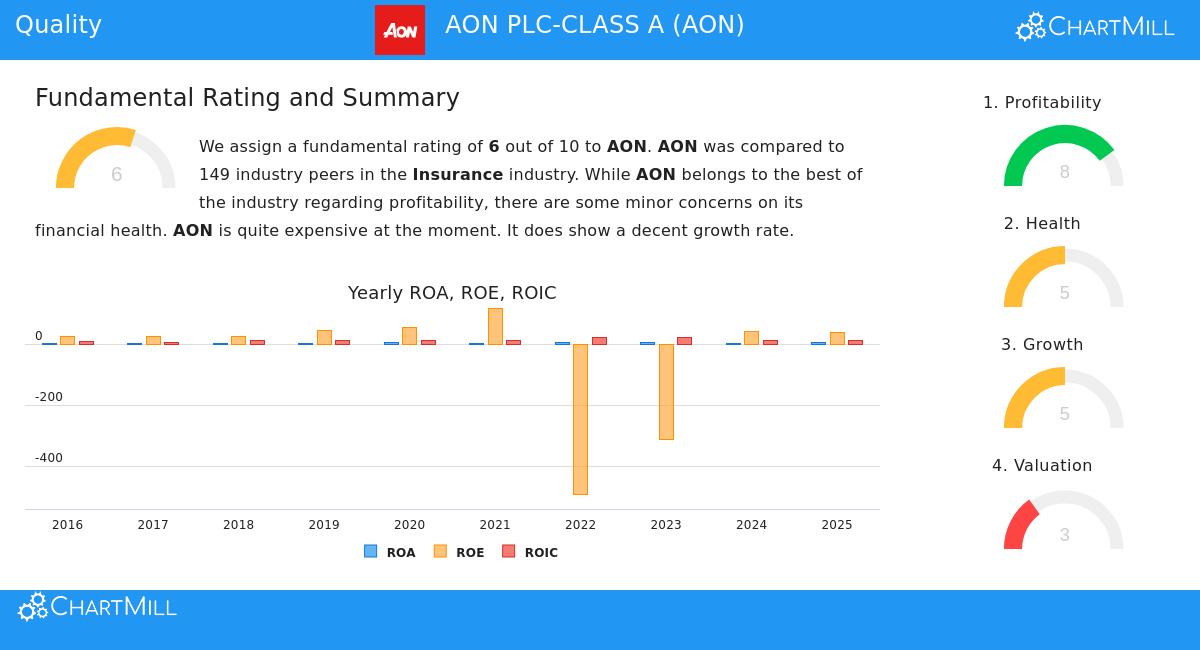

An examination of Aon’s detailed fundamental report gives a wider context that backs the screen’s results. The report gives Aon an overall rating of 6 out of 10, highlighting a varied but somewhat positive view.

- Strengths: Aon is strong in Profitability, scoring an 8/10. It has industry-leading margins and returns on equity and assets. Its Growth score of 5/10 is supported by a solid historical record in both revenue and EPS expansion.

- Considerations: The main area of note is Financial Health, which scores a 5/10. While the company creates strong cash flow and has been lowering its share count, it holds a higher amount of debt compared to equity than many industry peers. This is partly balanced by its significant cash generation, as seen in the Debt/FCF ratio. Valuation is scored at 3/10, with metrics implying the stock trades at a higher price than its industry average, though not necessarily compared to the wider market. For quality investors, a fair premium for a better business is often acceptable, but it stays a key point for personal evaluation.

Is Aon a Quality Investment Candidate?

According to the Caviar Cruise standards, Aon makes a solid argument for quality investors. The company shows the necessary features the method looks for: outstanding returns on its invested capital, a history of profitable increase that exceeds sales expansion, strong translation of profits into cash, and a reasonable debt profile relative to its cash flow. These numerical factors point to a business with a lasting competitive strength in the global professional services market.

However, the screen is a beginning, not a conclusion. The fundamental analysis notes that Aon’s leverage is higher than average, which needs understanding, and its valuation is not low. Quality investing also involves subjective assessments about a company’s competitive barrier, leadership, and long-term industry directions—factors that demand more investigation beyond the figures.

Interested in examining other companies that pass the Caviar Cruise quality screen? You can locate the complete, current list of qualifying stocks by going to the Caviar Cruise stock screener.

Disclaimer: This article is for informational purposes only and does not constitute financial advice, a recommendation, or an offer to buy or sell any security. Investing involves risk, including the potential loss of principal. You should conduct your own research and consult with a qualified financial advisor before making any investment decisions.