For investors looking to balance the search for high-growth companies with some fiscal care, the "Growth at a Reasonable Price" (GARP) method presents a viable middle path. This method tries to find companies with solid and lasting growth paths, but whose shares are not priced at extreme levels. It avoids the pure trend following of high-growth stocks and the value pitfalls that can trouble inexpensive companies with poor futures. By applying a systematic filter to search for strong growth, fair valuation, and acceptable basic financial condition and earnings, investors can create a list of companies that possess both the capacity for increase and a share price that is not overly optimistic.

One company appearing from an "Affordable Growth" filter is Advanced Micro Devices Inc (NASDAQ:AMD), an important participant in the semiconductor sector. The filter, which looks for stocks with a growth rating above 7, valuation above 5, and acceptable ratings in earnings and financial condition, indicates AMD has a profile that deserves more study for investors focused on GARP.

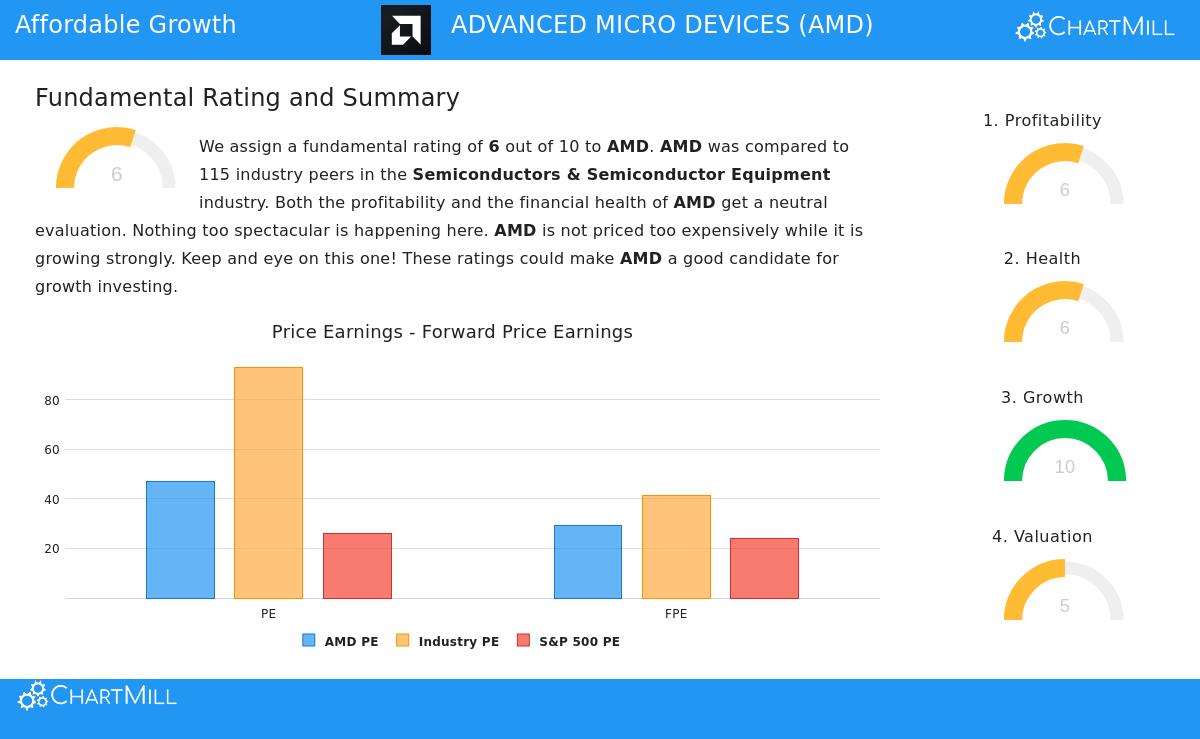

A Notable Growth Profile

The most striking part of AMD's basic report is its outstanding growth rating, which receives a top score of 10. This rating is based on strong past results and even more positive future estimates. The company has shown it can meaningfully grow its revenue and profit, a key element for any growth-focused investment.

- Past Performance: In the last year, AMD's revenue increased by 34.34%, while earnings per share (EPS) rose by 25.60%. The longer-term averages are also solid, with revenue growing close to 29% each year.

- Future Estimates: Analyst projections indicate a speeding up of this pattern. EPS is forecast to increase at an average yearly rate above 42% in the next few years, with revenue anticipated to rise nearly 32% yearly. This expected growth is central to the GARP method, as it looks for companies where future growth can support current share prices.

Valuation Considered

With a valuation rating of 5, AMD is at the line of what the filter considers "not overpriced." This average score shows a detailed situation that is important for the affordable growth idea. On its own, common measures like the Price-to-Earnings (P/E) ratio of 47 seem high, particularly next to the wider S&P 500. However, valuation is comparative, especially for a fast-growth company in a specific field.

- Sector Comparison: Next to similar companies in the Semiconductors & Semiconductor Equipment sector, AMD's valuation seems more acceptable. Its P/E ratio is lower than about 64% of the sector, and its forward P/E ratio of 29.20 is lower than around 65% of rivals.

- Growth Adjustment: The review points out AMD's low PEG ratio, which modifies the P/E ratio for projected earnings growth. This measure implies the stock's price may be fair when its excellent growth expectations are considered. The report directly states that "a higher valuation could be acceptable as AMD's earnings are predicted to grow by 47.97% in the coming years."

Supporting Basics: Condition and Earnings

For a GARP method, solid growth at a fair price must be backed by a stable base. This is where the filter's needs for acceptable earnings and financial condition (both rated a 6 for AMD) are relevant. They help confirm the company can pay for its growth and handle economic changes.

- Financial Condition: AMD's balance sheet is firm. It has a very good Altman-Z score of 14.79, showing very low failure risk and doing better than over 80% of its sector. The company carries very little debt, with a good Debt-to-Equity ratio of 0.04 and a solid Debt-to-Free-Cash-Flow ratio, meaning it can comfortably handle its debts. Its current and quick ratios also indicate sufficient cash to meet near-term requirements.

- Earnings: While not outstanding, AMD's earnings are adequate. Its Return on Equity (6.88%) and Profit Margin (12.51%) are higher than most of its sector peers. It is worth noting that some margins have decreased lately, which is an area to watch, but the company continues to be reliably profitable with positive earnings and cash flow.

Final Points and Next Steps

Advanced Micro Devices offers an example of the compromises and checks of the Growth at a Reasonable Price method. Its growth story is strong and well-backed by both recent performance and future projections. While its valuation is not low on its own, it seems acceptable compared to its high-growth sector and when considering that growth through measures like the PEG ratio. This matches the filter's aim of locating stocks that are "not overpriced." Also, its sufficient ratings in financial condition and earnings provide a basic verification, lowering the chance that the growth potential relies on weak finances.

For investors wanting to examine other companies that match this "Affordable Growth" profile, a ready-made filter is accessible to see more options: View the Affordable Growth Stock Screen.

A more complete look at AMD's basic measures, including the full review across growth, valuation, condition, earnings, and dividend groups, is available in its Fundamental Analysis Report.

Disclaimer: This article is for information only and is not financial advice, a suggestion, or an offer to buy or sell any security. Investors should perform their own study and think about their personal financial situation and risk comfort before making any investment choices.