If you thought Thursday was going to bring the calm investors were hoping for after Wednesday's brief respite, think again.

By the closing bell, the Nasdaq had surrendered 2.4% and the Dow was down a full percent and both losses traced back to the same anxious root: a Middle East conflict that refuses to de-escalate, compounded by a technology story that rattled the entire semiconductor complex.

There was nowhere to hide if your portfolio leaned into tech.

The Rundown

- Markets got hammered: Nasdaq ▼, Dow ▼, S&P ▼ driven by Middle East tensions and a tech selloff.

- Iran rejects peace talks. Trump warns "no way back" if too late. Brent crude surges 5.5% to $107.80/barrel. Strait of Hormuz reopening looks remote. OECD warns of stagflation risk.

- Google's AI memory breakthrough triggers chip selloff. New compression tech could slash AI memory demand (3+ years out). Memory chipmakers crushed.

- Helium supply crisis brewing. Qatar (33% of global supply) halted production due to conflict. South Korea imports 65% from Qatar. Even if conflict ends quickly, restart takes weeks, normalization takes months.

- Jefferies kicks off earnings: Record revenue, but missed EPS. Preview of bank earnings: strong top lines, credit/geopolitical costs hitting profits.

- Snap ▼ on EU child safety investigation under Digital Services Act. Heavy minor user base makes it vulnerable.

- Macro: Jobless claims ▲. 10-year Treasury yield ▲. EUR/USD steady.

Iran Rejects Peace, Markets Pay the Price

Earlier this week, speculation about a potential Iran–US deal had briefly calmed nerves, pulling the Brent crude price below $100 per barrel. By Thursday, that optimism had completely evaporated. Tehran formally rejected American overtures, and President Trump responded on Truth Social with a pointed warning: "Iran must think very seriously about this before it's too late, because if it's too late, there's no way back."

The prospect of a swift reopening of the Strait of Hormuz now looks remote. Brent crude surged 5.5% to $107.8 per barrel, its highest level in months.

The OECD chimed in with a warning that shouldn't be taken lightly: if energy prices continue to rise due to prolonged conflict, both inflation and economic growth will suffer simultaneously, a stagflationary scenario that central banks are poorly equipped to handle.

The euro/dollar pair held at 1.1524 as traders weighed those risks.

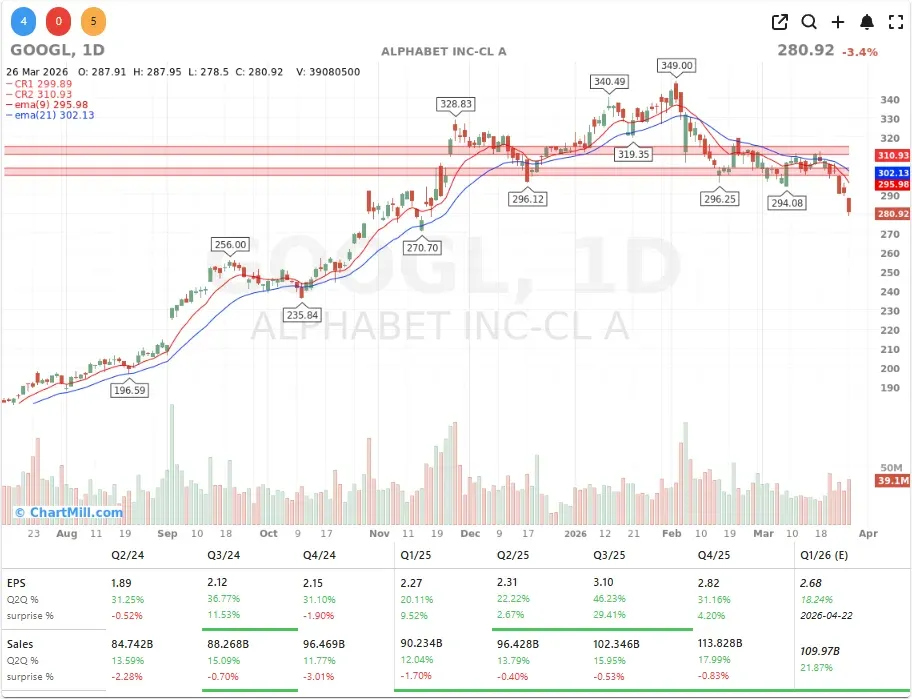

Google's Algorithm Shakes the Memory Chip Market

Even without the geopolitical backdrop, Thursday would have been a rough day for memory chipmakers.

Google's (GOOGL | ▼3.44%) research team unveiled a new compression technique for large language models, one that could dramatically reduce the amount of memory those AI workloads actually consume.

Now, most analysts are saying the practical impact is three years away at minimum. But that hasn't stopped investors from locking in gains on a cohort of stocks that had risen sharply on the back of AI-driven memory demand.

SanDisk (SNDK | ▼11.02%), Micron Technology (MU | ▼6.97%), and Western Digital (WDC | ▼7.70%) all fell more than 5%, as profit-taking accelerated. The S&P 500 Semiconductors subindex lost 4.1% on the day.

"There is a rotation underway where investors are selling winners," noted Hardika Singh, strategist at Fundstrat Global Advisors.

"Everyone has agreed that we are all too heavily invested in tech." That's a fair observation, and one I'd agree with, the concentration risk in mega-cap tech had been building for months.

Helium: The Invisible Supply Chain Risk

There's another layer to the chip story that hasn't gotten nearly enough attention: helium.

Semiconductor fabrication relies on helium as a coolant and purging gas, and there is currently no viable substitute. Qatar, which in 2025 accounted for roughly one-third of global helium production, has halted output as a result of the conflict.

South Korea - home to Samsung and SK Hynix - imports 65% of its helium from Qatar. TSMC has so far said it expects no major disruption, and large chip companies generally hold multi-month reserves.

But here's the catch: even a rapid de-escalation won't immediately fix the problem. Sector experts estimate it would take weeks to restart Qatar's production and months before logistics normalize.

If the conflict drags on, helium could become a genuine pinch point for the entire semiconductor supply chain and that's a risk I don't think the market has fully priced in yet.

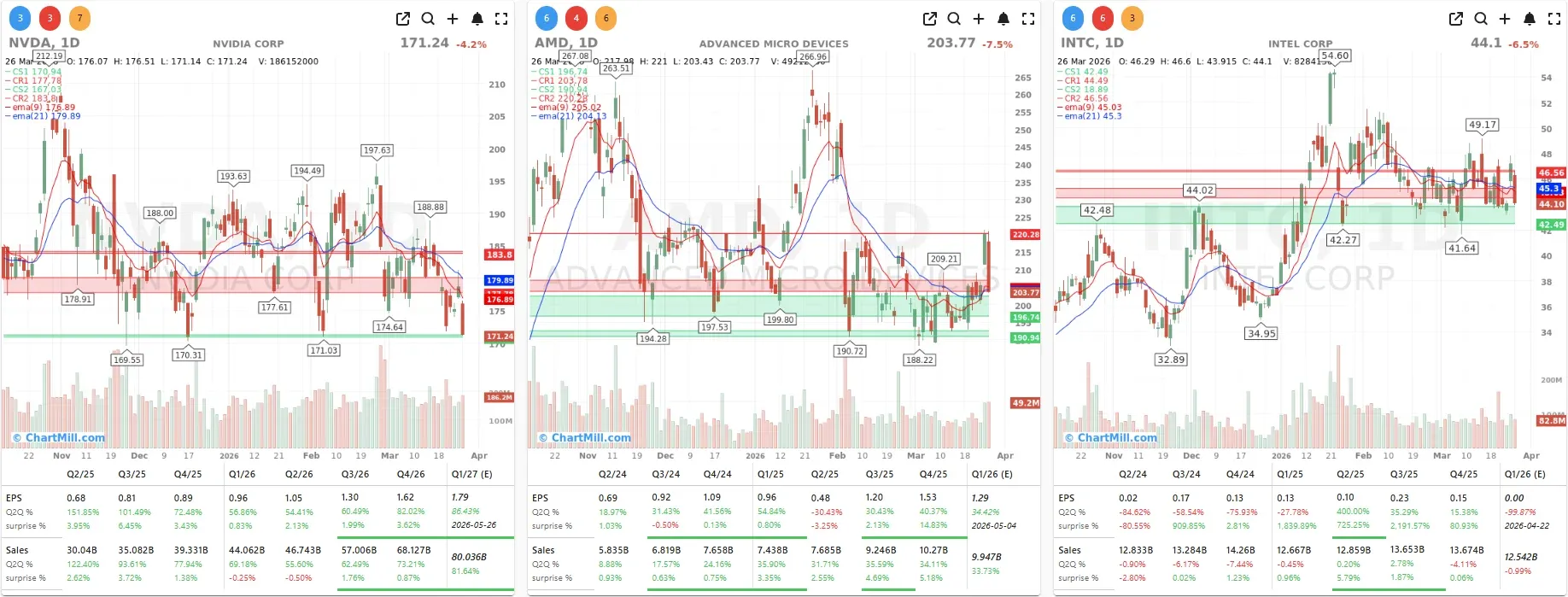

Broader Chip Selloff: NVDA, AMD, INTC Under Pressure

The damage wasn't limited to memory names.

Nvidia (NVDA | ▼4.16%) and Alphabet (GOOGL | ▼3.44%) each fell more than 3%, while AMD (AMD | ▼7.49%) and Intel (INTC | ▼6.53%) both approached 7% declines.

In an environment where sentiment is already fragile, the combination of the helium risk story and the Google memory-compression news gave traders a narrative excuse to reduce their semiconductor exposure across the board.

What concerns me here is that this isn't purely technical selling, there are genuine fundamental questions emerging around the AI memory trade. The thesis was straightforward: AI requires exponentially more memory, and chip companies with exposure to that theme would benefit for years.

That thesis hasn't collapsed, but it has developed some cracks, and investors are right to reassess position sizing.

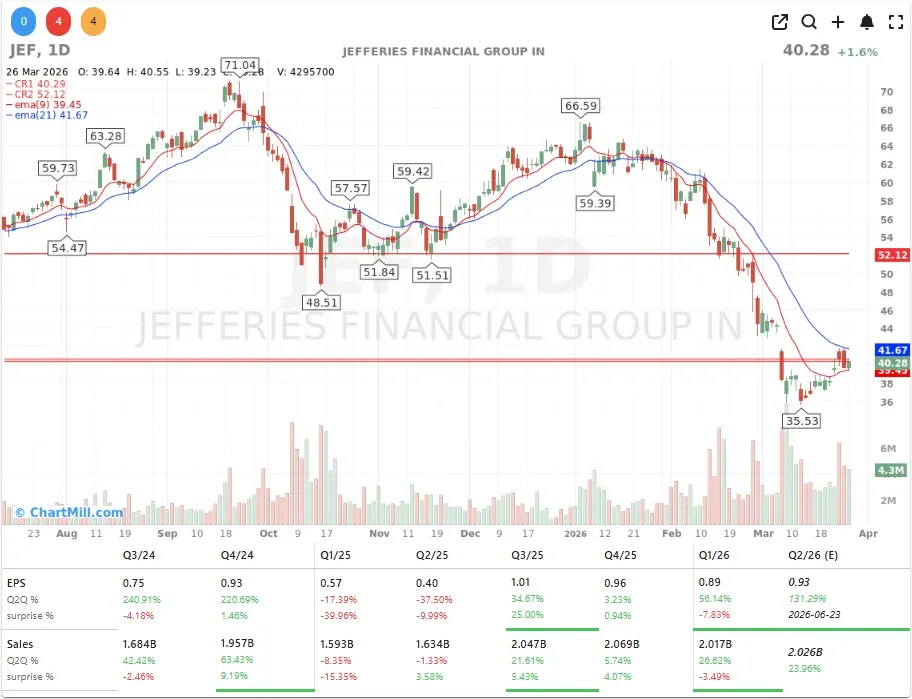

Jefferies Opens Q1 Season — Record Revenue, Missed Profit

Jefferies (JEF | ▲1.61%) became the first major US investment bank to report Q1 results for its fiscal year ending February 28.

The headline looked promising - record quarterly revenues - but the bottom line disappointed. EPS came in at $0.70, well below the $0.87 consensus estimate, as $17 million in losses tied to the bankruptcies of Market Financial Solutions and First Brands dented profitability.

The underlying business was solid: wealth management revenues grew 15% to $220.3 million, and investment banking surged 28% to $1.8 billion.

But as Morgan Stanley analyst Ryan Kenny noted, "The stock needed a clear beat to relieve the pressure from macro-driven market sentiment and credit/legal risks."

FICC (fixed income, currencies and commodities) trading was described as weak even after adjusting for the MFS losses.

For those watching the broader bank reporting season, Jefferies is a useful bellwether. Investment banking activity was clearly strong in Q1, but credit risks and volatile trading conditions are real headwinds.

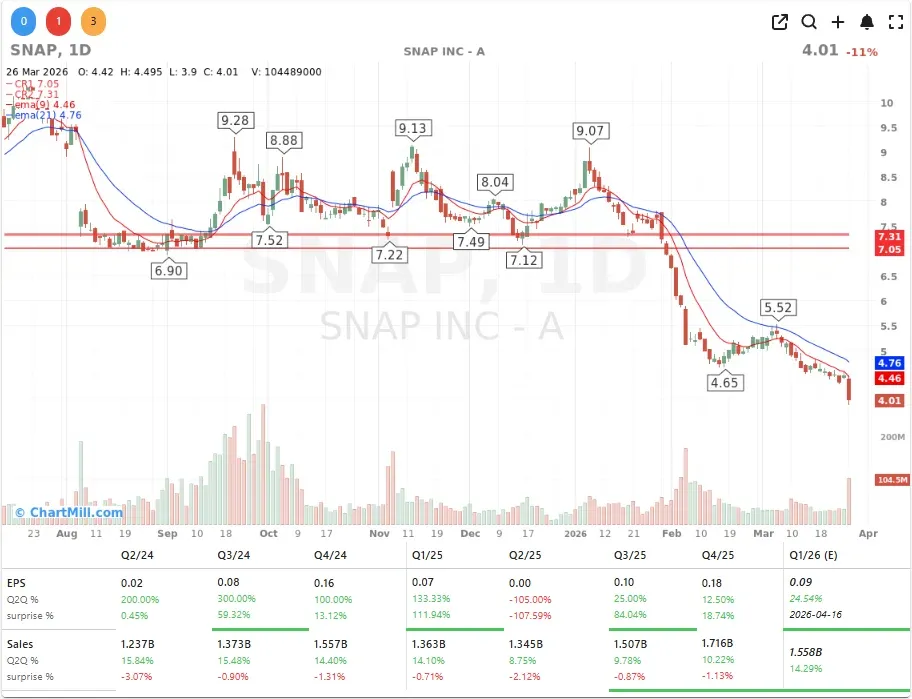

Snap Falls 11% as EU Opens Child Safety Investigation

Snap (SNAP | ▼10.69%) suffered the steepest single-day drop among major platform stocks after the European Commission officially launched a formal investigation into Snapchat, along with several adult content websites, to assess whether they're doing enough to protect minors.

The probe falls under the Digital Services Act, which carries the potential for significant fines and operational restrictions.

A near-11% move on a regulatory announcement is a strong signal that investors were already nervous about Snap's regulatory exposure. With an active user base heavily skewed toward younger demographics, Snap is particularly vulnerable to child safety scrutiny.

I'd watch closely for any preliminary findings, as these investigations can drag on and keep a cloud hanging over the stock.

Macro Check: Jobless Claims, Yields & FX

-

Weekly initial jobless claims rose modestly to 210,000, up 5,000 from the prior week. Not a worrying number in isolation, but worth monitoring given the OECD's stagflation warning and the potential for energy prices to erode consumer spending.

-

The EUR/USD pair held steady at 1.1524, euro strength reflecting some capital rotation away from US assets amid geopolitical uncertainty.

-

The 10-year Treasury yield's 9 basis point climb to 4.42%, driven partly by the tepid bond auction and partly by the energy shock, is something I think deserves attention. If yields continue to grind higher while risk assets sell off, the Fed will face an increasingly awkward policy environment.

My Take: Volatility Is the New Baseline

Thursday was a day that put risk management front and center. Memory chips face a genuine dual headwind: near-term profit-taking driven by the Google compression story, and a medium-term supply chain risk from the helium situation.

Neither is resolved, and both bear watching. Meanwhile, oil's resurgence above $107 is forcing portfolio managers to rethink their inflation assumptions just as the earnings season heats up.

Until there's meaningful clarity on Iran, I expect volatility to remain elevated. Keep a close eye on Fed speakers next week and any signals from the energy market.

On the earnings front, the Jefferies beat-but-miss pattern may be a preview of what's to come from larger banks: strong top lines, but credit and geopolitical costs eating into the bottom line.

Stay selective, stay disciplined, and don't let short-term noise distract you from your longer-term thesis.

ChartMill Market Desk - Kristoff

This daily update is prepared by ChartMill for informational purposes only and does not constitute investment advice. Always do your own due diligence before making investment decisions.