The investment philosophy created by Peter Lynch focuses on finding companies with good growth potential that are available at fair prices, a method frequently described as Growth at a Reasonable Price (GARP). This method steers clear of the far ends of speculative high-growth stocks and deep-value turnarounds, concentrating instead on financially sound businesses with steady development. The process applies particular fundamental filters to identify companies that are increasing earnings reliably, are profitable, keep a strong financial position, and are not priced too high by the market. ADOBE INC (NASDAQ:ADBE) resulted from a screen constructed on these ideas, offering a persuasive case for investors with a long-term view.

Alignment with Lynch-Style Criteria

Adobe matches the main quantitative filters of the Lynch strategy, which are intended to find good growth companies without paying a high price. The given data indicates the company satisfies or goes beyond the particular limits established by the screen.

- Steady Earnings Growth: A fundamental part of Lynch's strategy is a record of solid, but not extremely rapid, earnings growth. Adobe's EPS has increased at an average yearly pace of 18.7% over the last five years. This number easily meets the screen's lowest requirement of 15% and stays under the 30% maximum Lynch used to steer clear of unstable growth paths.

- Fair Valuation via PEG Ratio: To make sure investors are not paying too much for growth, Lynch preferred stocks with a Price/Earnings to Growth (PEG) ratio of 1 or lower. Adobe's PEG ratio, calculated from its past five-year growth, is 0.86. This shows the stock is fairly valued compared to its historical earnings increase, a key element in the GARP method.

- High Profitability (ROE): Lynch looked for companies that effectively produce profits from shareholder equity. Adobe's Return on Equity of 59.1% greatly exceeds the screen's 15% minimum, putting it in the highest group of its software industry competitors and indicating outstanding operational effectiveness.

- Financial Condition Metrics: The strategy favors companies with controlled debt and enough immediate liquidity. Adobe's Debt-to-Equity ratio of 0.53 is under the screen's highest limit of 0.6, showing a balanced capital structure. Also, its Current Ratio of 1.02 satisfies the condition of being at least 1, indicating a sufficient capacity to meet short-term liabilities.

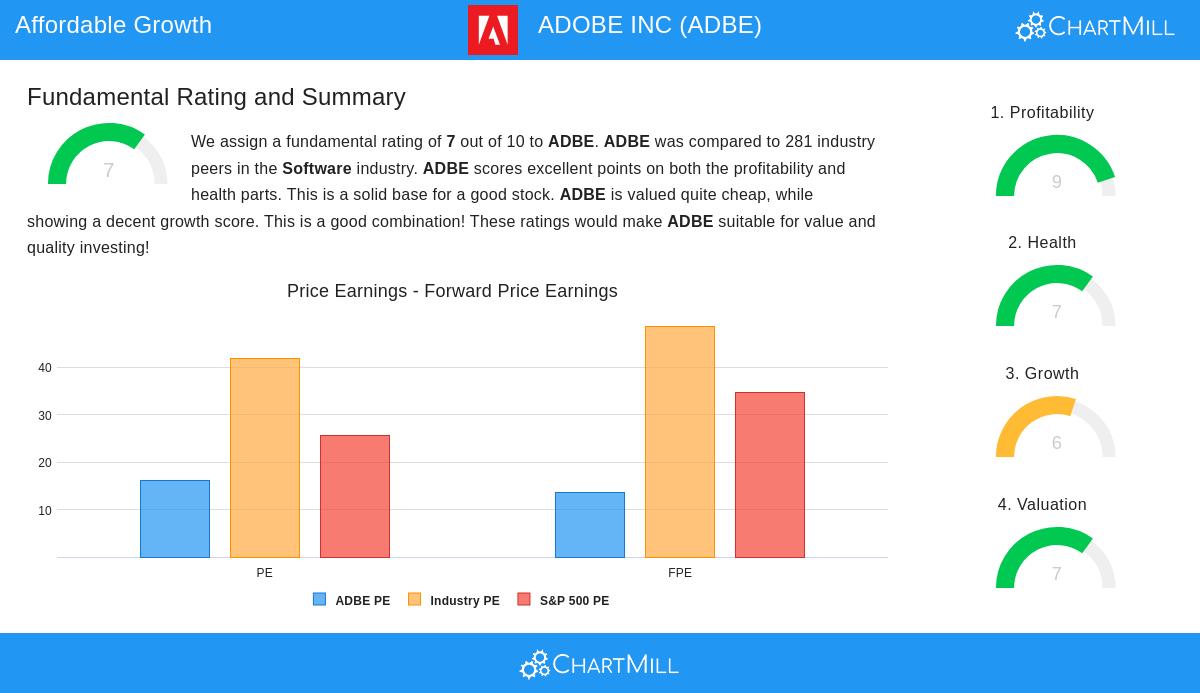

Fundamental Condition Summary

A wider examination of Adobe's fundamental report supports the results from the Lynch-based screen. The company gets a good total fundamental rating of 7 out of 10. Its profitability is a notable characteristic, scoring a 9, fueled by sector-leading margins and returns on assets and invested capital. The health score of 7 shows a company that is generating value, since its return on invested capital is higher than its cost of capital. While its liquidity ratios are moderate, its very good solvency, shown by a high Altman-Z score and a low debt-to-free-cash-flow ratio, reduces worries. From a valuation standpoint, Adobe seems fairly priced relative to both the wider S&P 500 and its own sector, with multiple metrics indicating it could be priced below its true value considering its quality and growth characteristics. You can examine the detailed fundamental analysis here.

Outlook for the Long Term

For investors following a long-term GARP strategy, Adobe stands as a representative candidate. The company functions in the necessary and growing digital experience and content creation sectors, supplying vital software tools. Its shift to a cloud-based subscription system has produced a consistent and repeating revenue source. The mix of lasting competitive strengths, reliable earnings growth, and a fair valuation offers a firm base for possible long-term price gains. While future growth rates are predicted to slow from their past levels, they remain solid, fitting with Lynch's liking for maintainable, instead of rapid, growth.

The screen that found Adobe is grounded in a structured, proven strategy. For investors looking to perform their own analysis, a list of other companies presently meeting comparable filters is available by exploring the Peter Lynch Strategy stock screener.

Disclaimer: This article is for informational purposes only and does not constitute financial advice, a recommendation, or an offer or solicitation to buy or sell any securities. The opinions expressed are based on current market conditions and data, which are subject to change. All investment decisions should be based on your own research, financial situation, and risk tolerance.