For investors looking for chances in the market, a disciplined method often gives the best outcomes. One such approach is value investing, a plan that involves finding companies trading for less than their real worth. The central idea is to purchase these undervalued securities and keep them until the market fixes the price difference. A key part of this work is finding stocks that are not only low-priced, but also fundamentally good, companies with strong financial condition, steady earnings, and the possibility for expansion. This mix of a low price and good basic business can offer a "margin of safety," a cushion against mistakes in assessment or unexpected market declines.

A recent filter for "acceptable value" stocks, which looks for companies with strong valuation grades along with acceptable marks for earnings, condition, and expansion, has pointed to TOLL BROTHERS INC (NYSE:TOL) as a possible choice. As a top builder of luxury homes, Toll Brothers works in a cyclical field, making a complete basic study key to tell a real value chance from a possible value trap.

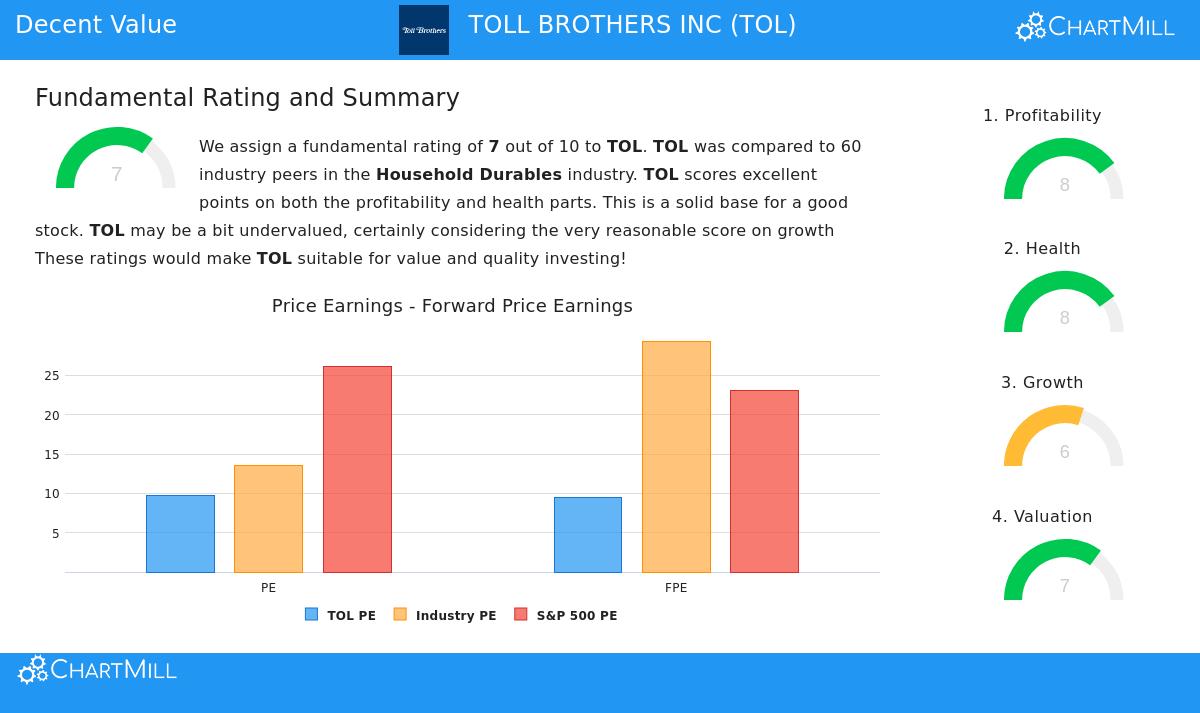

Valuation: An Attractive Entry Point

The most direct draw for a value investor is a stock's price compared to its earnings and cash flow. Toll Brothers shows a valuation picture that looks meaningfully lower, not only within its own industry but also compared to the wider market.

- Price-to-Earnings (P/E): TOL trades at a P/E ratio of 9.70. This is clearly lower than the industry average of about 13.58 and less than half the S&P 500's current average of 26.17.

- Forward P/E: Looking forward, the company's forward P/E ratio of 9.45 implies the valuation stays attractive based on future earnings forecasts, grading lower-priced than over 80% of its industry group.

- Price-to-Free-Cash-Flow: The stock is also valued low based on its free cash flow production, an important measure for judging the actual cash earnings available to the business.

This lower valuation is the basic filter that spots TOL as a possible value stock. For an investor, it implies the market may be pricing the company's earnings ability too low.

Financial Health: A Strong Base

A low-priced stock is only a good investment if the company is financially secure. A strong balance sheet gives the toughness to endure economic cycles and avoid the problems of too much debt. Toll Brothers gets a good condition grade, with several key positives:

- Solvency: The company keeps a careful debt-to-equity ratio of 0.32, showing it is not too dependent on debt funding. More notably, its debt-to-free-cash-flow ratio is a very small 1.87, meaning it could in theory pay off all its debt in under two years using its current cash flow, a mark of high financial soundness.

- Liquidity: With a current ratio of 3.88, Toll Brothers has enough short-term assets to meet its short-term debts, doing better than 70% of its industry. While its quick ratio is smaller, the overall solvency and earnings setting suggests the company handles its working capital well for its business plan.

- Altman-Z-Score: A score of 4.09 shows a small near-term chance of financial trouble, giving more confidence of the company's steadiness.

This financial strength is important for a value investor. It means the company is not likely to be a "value trap," a seemingly low-priced stock that is actually low-priced for a basic reason like approaching failure or heavy debt.

Profitability: Quality at a Lower Price

Value investing is not only about buying troubled companies at a low price; it is often about buying good companies when they are briefly unpopular. Toll Brothers shows very good earnings, which backs the argument for its real worth.

- Return Measures: The company has a strong Return on Invested Capital (ROIC) of 11.76%, doing better than 85% of its industry. This shows management is using capital well to create profits. Its Return on Equity (ROE) of 16.41% is also good.

- Widening Margins: Both operating margin (15.52%) and profit margin (12.26%) rank in the top group of the homebuilding industry. Importantly, these margins have been getting better in recent years, a sign of working efficiency and pricing ability.

Strong and rising earnings is a key point of difference. It suggests the company's low valuation is not a sign of poor operations but possibly wider market feeling towards the housing sector.

Growth: The Driver for Future Worth

While pure value stocks sometimes miss growth, the best choice mixes value with a maintainable growth path. This can help speed up the market's re-pricing of the stock. Toll Brothers shows a reasonable growth picture:

- Past Growth: Over the past several years, the company has reached a notable annual EPS growth rate of over 31% and sales growth of over 9%.

- Future Forecasts: Analysts predict continued growth, with expected annual EPS growth near 12% and sales growth around 8% in the coming years. This forward-looking steadiness in sales growth matches its past performance.

For a value investor, this growth part is key. It provides a way for the company to grow into its valuation and later get a higher market price as earnings rise, instead of depending only on a shift in market feeling.

Conclusion

The bringing together of these points, a very low valuation, a very strong balance sheet, very good and improving earnings, and a steady growth view, makes TOLL BROTHERS INC an attractive example for value-focused study. It shows the hunt for a good business that may be missed by the wider market. The company's basic report, available here, explains these measures more.

Naturally, investing in a cyclical homebuilder holds built-in risks linked to interest rates and economic condition. However, for an investor using a value plan with a margin of safety, TOL's current basic picture shows a notable chance where the figures suggest the market price may not completely show the basic business quality.

This study of Toll Brothers came from a specific basic filter. Investors curious in finding other companies that fit similar standards of good valuation, earnings, condition, and growth can look at the Decent Value Stocks screen for more possible ideas.

Disclaimer: This article is for information only and does not make up financial guidance, a suggestion, or an offer to buy or sell any securities. Investors should do their own study and talk with a qualified financial advisor before making any investment choices.