In a market that often swings between speculative growth stories and deeply discounted value traps, the GARP (Growth at a Reasonable Price) strategy offers a middle path that has a strong historical pedigree. This approach, famously championed by Peter Lynch in his book One Up on Wall Street, seeks out companies that are growing their earnings at a sustainable pace while trading at fair valuations. Lynch’s method avoids the extreme volatility of high-flying growth stocks and the stagnation of deep-value plays. Instead, it focuses on a disciplined set of fundamental criteria: steady earnings growth (not too fast, not too slow), low debt, strong profitability, and a reasonable price relative to that growth. These are the hallmarks of a portfolio built for long-term compounding.

PulteGroup Inc (NYSE:PHM) emerges as a strong candidate from a recent screen based on this very strategy. As one of the largest homebuilders in the United States, operating under well-known brands like Centex, Del Webb, and Pulte Homes, the company meets the Lynch criteria in several key areas. Its business—building and financing homes for first-time, move-up, and active-adult buyers—is the kind of understandable, tangible industry Lynch favored, as it relies on fundamental demand rather than fleeting hype.

Meeting the Lynch Criteria

The Peter Lynch screen is not just about checking boxes; each filter serves a purpose in identifying a sustainable, growing business. Here’s how PHM stacks up against the core requirements of the strategy:

- Earnings Growth (EPS 5Y): 18.05% – Lynch specifically demanded earnings growth that was strong but not unsustainable. He set a range of 15% to 30% to avoid "hot stocks" that often flame out. PHM’s 5-year average EPS growth sits comfortably within this "sweet spot," indicating a company that has been expanding its profitability at a healthy, repeatable pace.

- PEG Ratio: 0.66 – This is the cornerstone of the GARP philosophy. The PEG ratio (Price/Earnings to Growth) measures valuation relative to growth. A PEG below 1.0 is Lynch’s threshold for a bargain. At 0.66, PHM’s current earnings multiple of roughly 11.8x is very cheap when compared to its past growth rate, suggesting the market is not fully pricing in its earnings potential.

- Debt/Equity: 0.18 – Lynch was famously wary of high leverage, preferring a debt-to-equity ratio below 0.6. A low debt load protects the company during economic downturns (such as a housing slowdown) and provides financial flexibility. PHM’s ratio of 0.18 is not only well below this threshold but also signals a very conservative financial structure.

- Current Ratio: 5.08 – This measure of short-term liquidity (current assets divided by current liabilities) needs to be above 1.0 according to Lynch, ensuring the company can meet its obligations. PHM’s ratio of 5.08 is exceptionally strong, providing a wide margin of safety.

- Return on Equity (ROE): 15.77% – A ROE above 15% is Lynch’s benchmark for a company that is generating healthy returns on shareholder capital. PHM’s 15.77% confirms that its growth is not being achieved at the expense of profitability, but rather through efficient capital allocation.

High-Level Fundamental Health

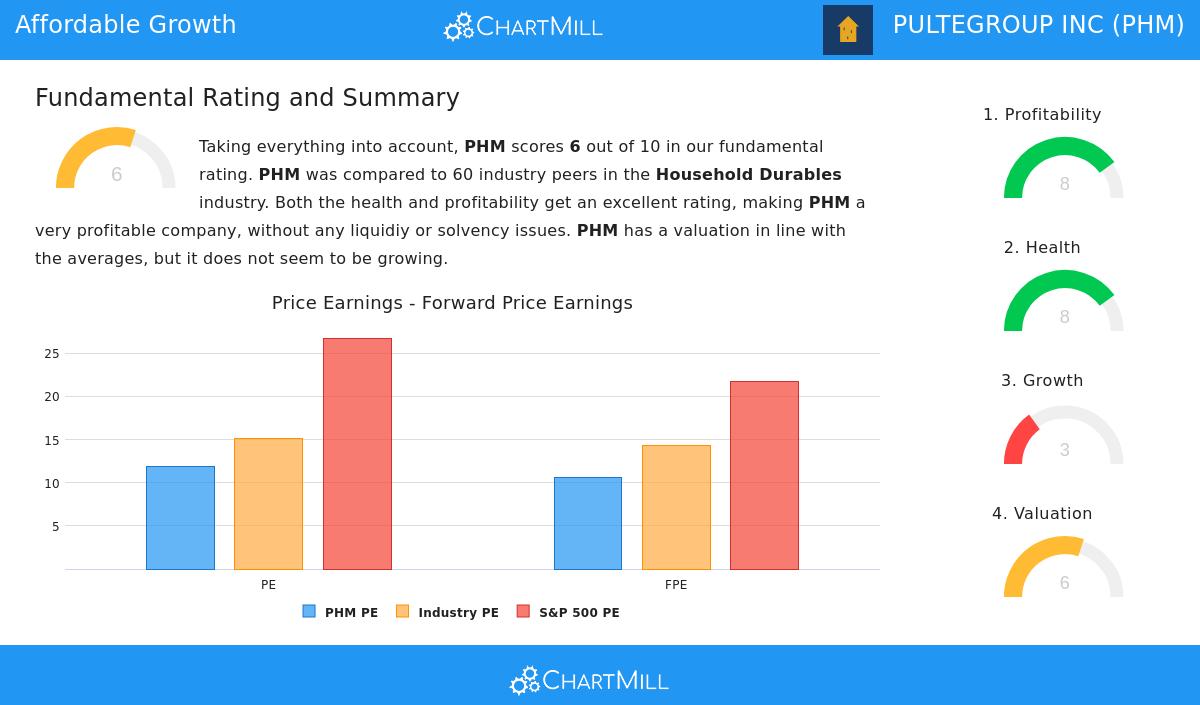

Beyond the specific Lynch filters, the overall fundamental report for PHM paints a picture of a solidly run business, albeit one currently facing a cyclical slowdown. The company earns a fundamental rating of 6 out of 10 from its peer group in the Household Durables industry. This rating is supported by top-tier scores in profitability and health, which are the strongest pillars of the analysis.

Specifically, PHM ranks in the top 10-15% of its industry for key metrics like Return on Assets (11.23%), Return on Invested Capital (13.45%), and Profit Margin (12.14%). Health metrics are similarly impressive, with an Altman-Z score of 5.63 (indicating virtually no bankruptcy risk) and a low Debt to Free Cash Flow ratio of 1.28. The company is also buying back shares, reducing its outstanding share count over the last five years.

However, the report does note a weaker growth score. While the 5-year history is strong, recent earnings growth has decelerated (a 26.77% decline year-over-year), and revenue has slipped slightly. This is typical for a cyclical homebuilder in a higher interest rate environment. The GARP strategy, as Lynch intended, is a long-term hold that weathers these cycles, and the company’s strong balance sheet and low valuation provide a cushion against the current headwinds. For a full breakdown of the financial metrics, you can view the complete fundamental analysis report.

Analyst Views and Market Context

While analyst coverage varies, the current valuation of PHM is attractive against the broader market backdrop. The S&P 500 is currently trading at over 26x trailing earnings and 21x forward earnings. In contrast, PHM trades at a P/E of 11.83 and a forward P/E of just 10.58. This significant discount offers a margin of safety that is rare in today’s market. Furthermore, the current long-term and short-term trends for the S&P 500 are positive, providing a supportive environment for equities that possess the defensive characteristics of a well-capitalized homebuilder.

For investors seeking a time-tested framework for identifying similar opportunities—companies trading at a discount to their sustainable growth, with strong financial health—you can run the screen yourself. The Peter Lynch strategy is designed to find these pockets of value across the market. Discover which other stocks meet this rigorous criteria by exploring the full list of results in our Peter Lynch Strategy screen.

Disclaimer: This article is for informational purposes only and does not constitute investment advice. Past performance is not indicative of future results. Always conduct your own due diligence before making any investment decisions.