The investment philosophy of legendary fund manager Peter Lynch, as detailed in his book One Up on Wall Street, focuses on finding well-run, growing companies that are trading at reasonable prices. Often called a Growth at a Reasonable Price (GARP) strategy, Lynch’s method steers clear of speculative stocks in favor of businesses with steady, clear growth, good financial health, and appealing valuations. The aim is to create a varied, long-term portfolio by locating companies that are profitable, not carrying too much debt, and whose stock price has not yet caught up to their future prospects.

A recent screen using Lynch’s main criteria has identified PulteGroup Inc (NYSE:PHM) as a candidate for more study. As one of the nation's largest homebuilders, PulteGroup works through a group of brands including Pulte Homes, Centex, and Del Webb, serving different customer groups across the United States.

Meeting the Lynch Criteria

The screen uses specific quantitative filters taken from Lynch’s ideas. Here is how PulteGroup measures up to these important benchmarks:

- Sustainable Earnings Growth: Lynch wanted companies with a good but not extreme growth path. The screen looks for a 5-year average annual EPS growth between 15% and 30%. PulteGroup’s EPS has grown at an average rate of 18.05% over this time, fitting within Lynch's target range, pointing to a history of steady, sustainable increase.

- Reasonable Valuation (PEG Ratio): Maybe the central part of the Lynch method is the Price/Earnings to Growth (PEG) ratio, which tries to find stocks where the price matches the growth rate. A PEG ratio of 1 or less is seen as good. PulteGroup’s PEG ratio, based on its past 5-year growth, is 0.57, showing the market may be pricing it below its historical growth.

- Strong Financial Health (Debt & Liquidity): Lynch stressed investing in companies with sound balance sheets. The strategy looks for a Debt-to-Equity ratio below 0.6, favoring even lower numbers. PulteGroup does very well here, with a D/E ratio of 0.17, showing a careful capital structure built mainly on equity. Also, its Current Ratio of 6.82 is much higher than the screen's need of 1, showing very good short-term cash availability and a solid ability to pay its bills.

- High Profitability (Return on Equity): To make sure shareholder money is used well, Lynch looked for a high Return on Equity (ROE). The screen requires an ROE above 15%. PulteGroup’s ROE of 17.09% meets this level, indicating effective management and good profitability.

Fundamental Health Check

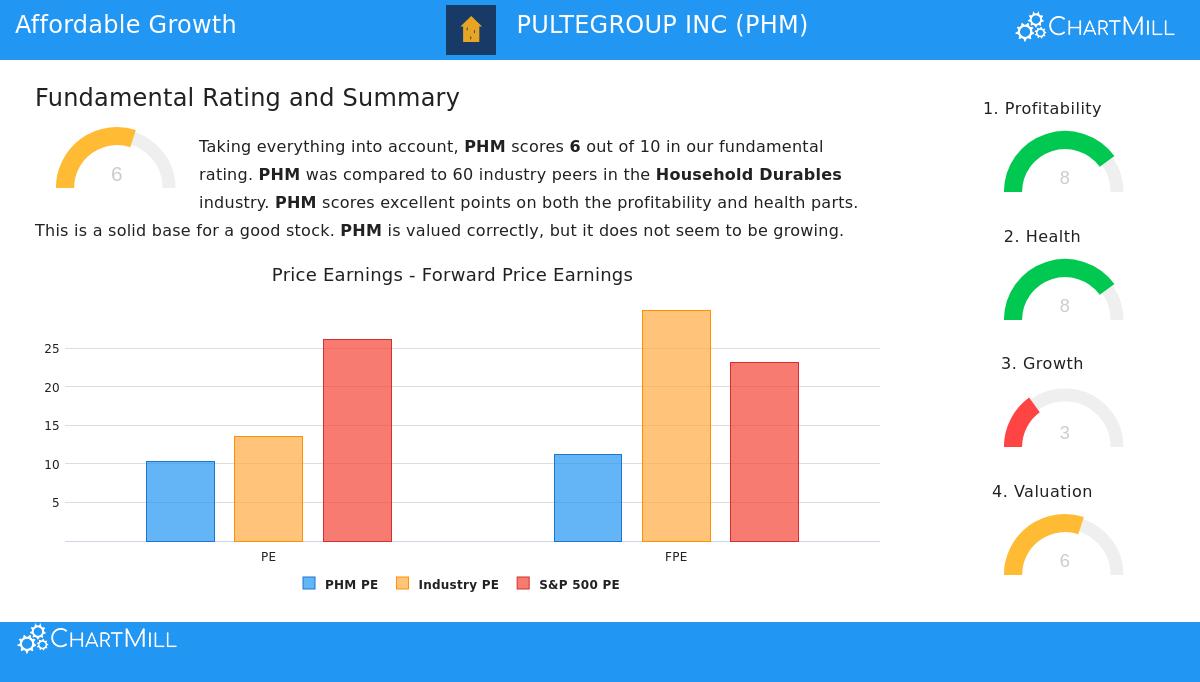

A wider view of PulteGroup’s fundamental profile, as shown in its detailed analysis report, supports the results from the Lynch screen. The company gets an overall fundamental rating of 6 out of 10, with special note in two important areas:

- Profitability & Efficiency: The company gets a high profitability score (8/10). Its profit margin of 12.82% and operating margin of 17.27% are in the best part of the household durables industry. Measures like Return on Invested Capital (ROIC) are also much better than industry averages, confirming the effective use of capital.

- Financial Health: The balance sheet is a clear positive, getting a health score of 8/10. Besides the low debt, the company’s Altman-Z score shows no bankruptcy risk, and it has been buying back its shares—a trait Lynch liked.

The main warning in the report focuses on growth. While the company has a good 5-year history, recent yearly EPS and revenue have gone down, and future growth forecasts are not high. This matches the up-and-down nature of the homebuilding industry and shows why the Lynch screen’s valuation check (the low PEG ratio) is important; it suggests the current stock price may already include a period of slower growth.

Is PHM a Lynch-Style Investment?

For an investor following Peter Lynch’s philosophy, PulteGroup offers an interesting example. It works in a clear business—homebuilding—that is important to the economy. It meets the quantitative checks for sustainable historical growth, fair valuation compared to that growth, and very good financial strength. The low PEG and Debt/Equity ratios especially fit with Lynch's attention to safety and value.

However, following Lynch’s way, the screen is only a first step for more non-number based study. An investor would need to evaluate the company’s competitive place in the housing market, the long-term view for housing demand, and its specific brand plans. The industry cycle pressures on current growth are a main point to learn about and watch.

Interested in finding other companies that pass the Peter Lynch investment screen? You can see the current list and change the criteria to your own choices by going to the Peter Lynch Strategy Screener.

Disclaimer: This article is for informational purposes only and does not constitute financial advice, a recommendation, or an offer to buy or sell any securities. Investing involves risk, including the potential loss of principal. You should conduct your own research and consult with a qualified financial advisor before making any investment decisions.